I’ve been slow to move on the strength of the Aussie economy this year for two reasons.

First, the China property accident led me to think that national income would be challenged later in the year. That might have been the case prior to the Ukraine war but the opposite has happened since.

Second, the bowel-shakingly swift economic cycle had me thinking that a global shock might hit us before the local economy gathered pace after the Morricession through the OMICRON new year.

Neither of those things has happened and, although both are still in prospect, the Australian economy has since moved distinctly towards an episode of hotting up.

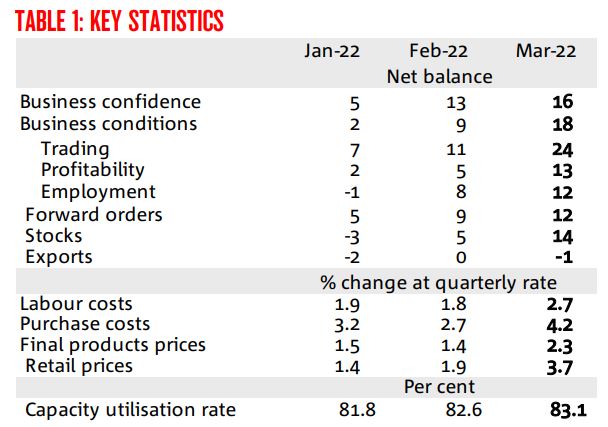

Yesterday’s NAB survey was red hot with most contemporaneous measures booming:

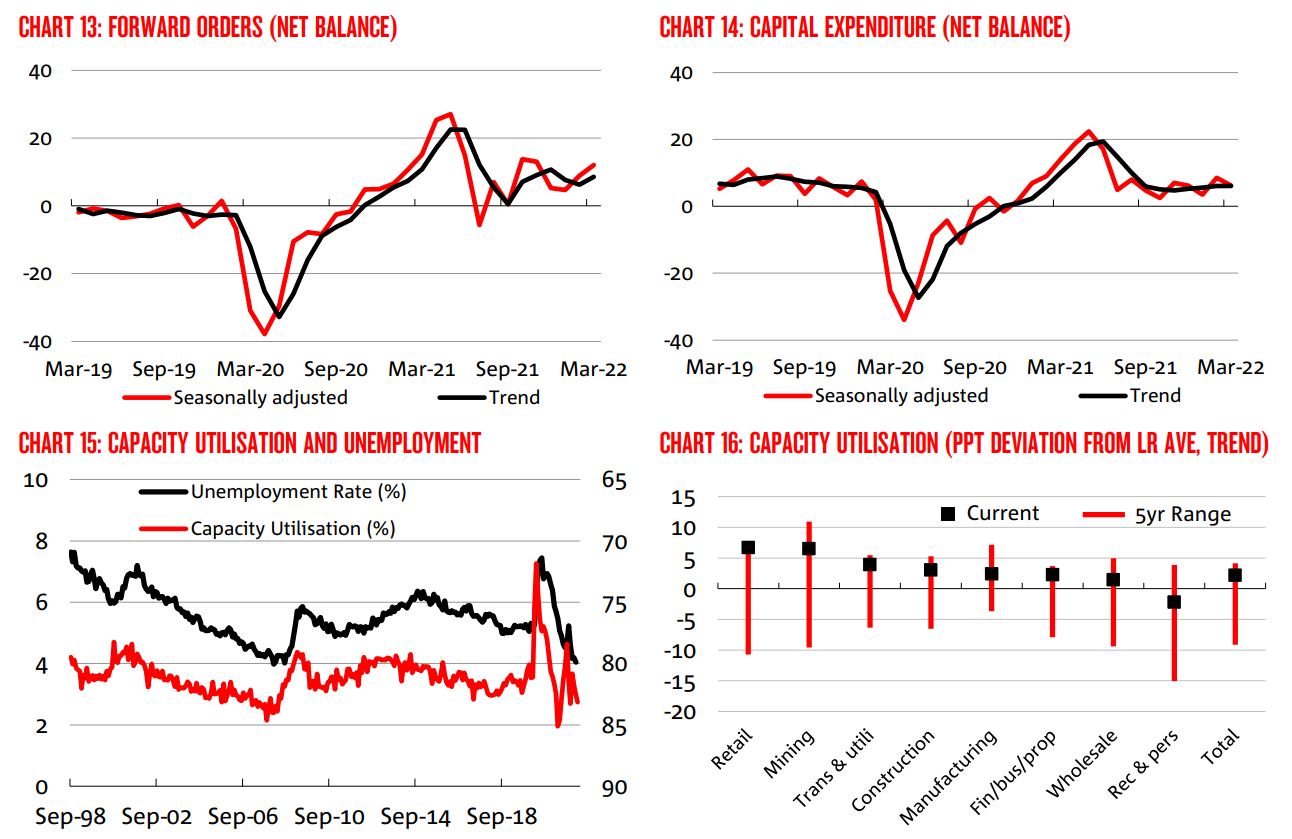

Forward-looking indicators were also good and capacity utilisation rising nicely:

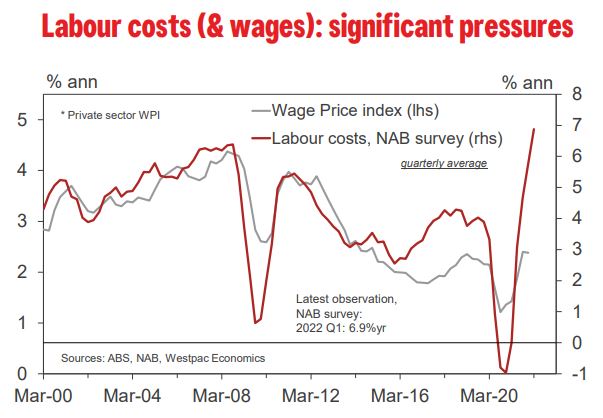

And, wait for it, this little beauty:

The uninitiated will look at these charts, most notably the last, and conclude that the RBA is far behind the curve. But there are some large caveats:

- The NAB survey is NOT as accurate as it once was. In particular, it has struggled to balance east versus west two-speed economies. Over several cycles now, it has exaggerated the strength and weakness of the net economy.

- Offical measures are still lagging the survey about the cost blowoff materially.

- Aussie households are very browbeaten by trickledown economics and hopeless at asking for wage rises.

- Immigration is returning.

- Australia is appallingly monopsonistic meaning wage rises are still difficult to get (though also that corporations might game price rises).

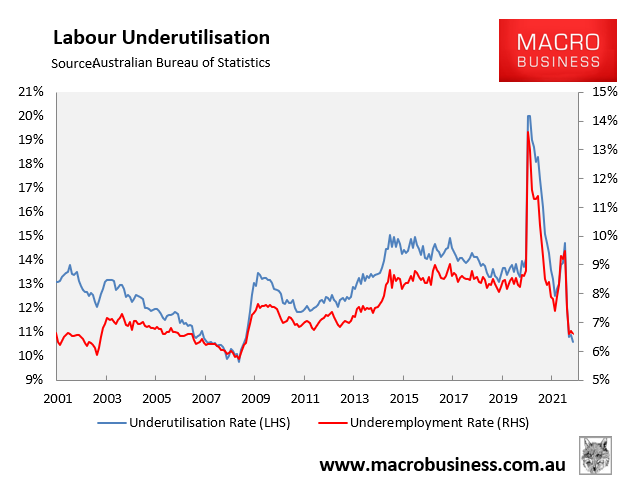

- There is still slack in the labour market, especially underemployment which has the best correlation with wages growth:

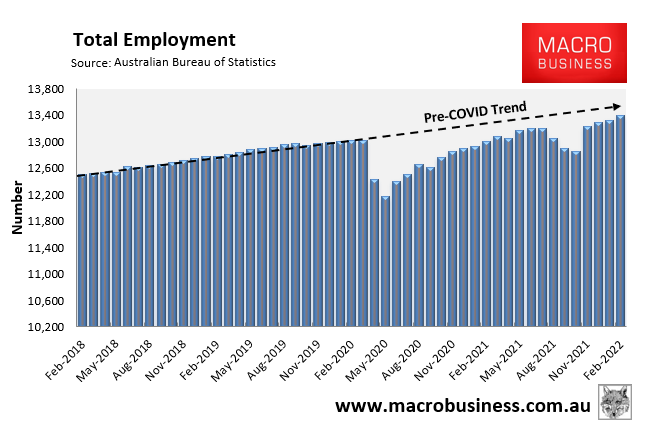

And we are way off trend jobs in aggregate meaning we can squeeze out some more participation with strong wages:

- There is still heaps of embedded rate rises in the fixed-rate mortgage roll-off and that’s going to hit house prices.

- This commodities boom is NOT going to be investment and employment intensive given LNG harms the economy, iron ore is in glut and coal cooked by ESG..

- And, the two global shocks are still rolling down the pipe.

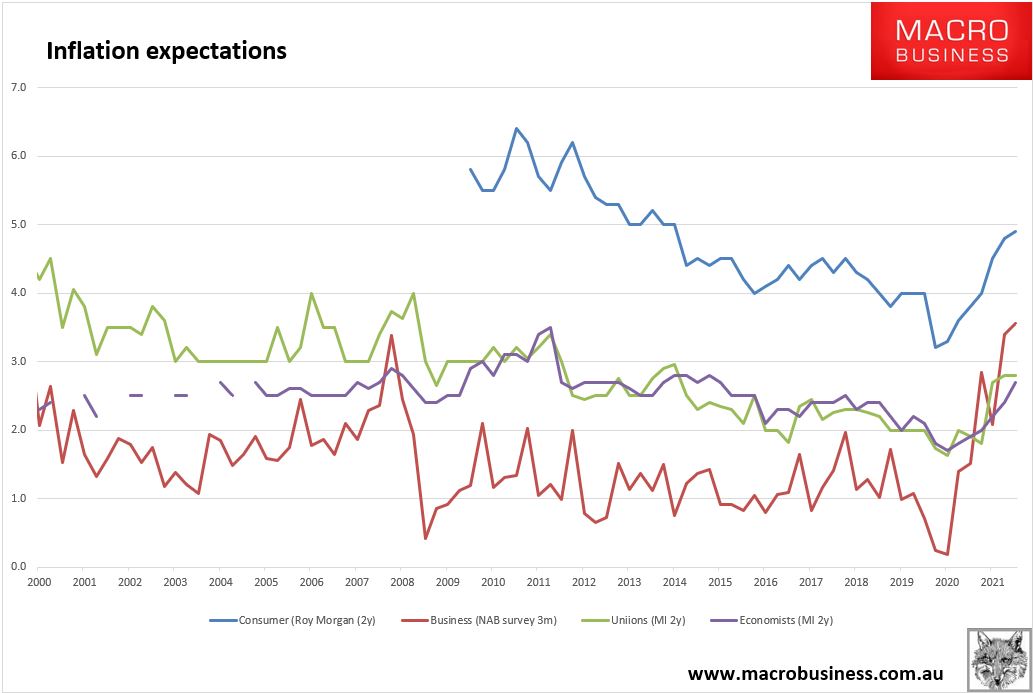

Finally, inflation expectations are still anchored. Note that NAB business inflation expectations are only for three months and are highly volatile. Longer-term expectations have barely gotten above the last defltionary decade:

If we let the economy run hot instead of listening to panic inflation panic merchants, we can deliver a powerful labour market into the forthcoming global downturn, which is more likely than not going to deliver a tidal wave of delation over 2023.

Australia could ride out the coming storm rather like it did in 2000, which is one reason why it had its twenty-year recession-free run.

If the RBA panics instead, we will join the world in an epic bust like it and we did in 2008.