DXY is telling you all you need to know about where markets are headed. Its huge ascending triangle has broken out on the monthly chart. I see no reason why it won’t challenge the millennium high in due course:

AUD was scorched though did better on the crosses:

Oil still has the polar opposite chart descending triangle. Any break of the $98 is the end game:

Advertisement

Metals rebounded for the day. Good luck with that:

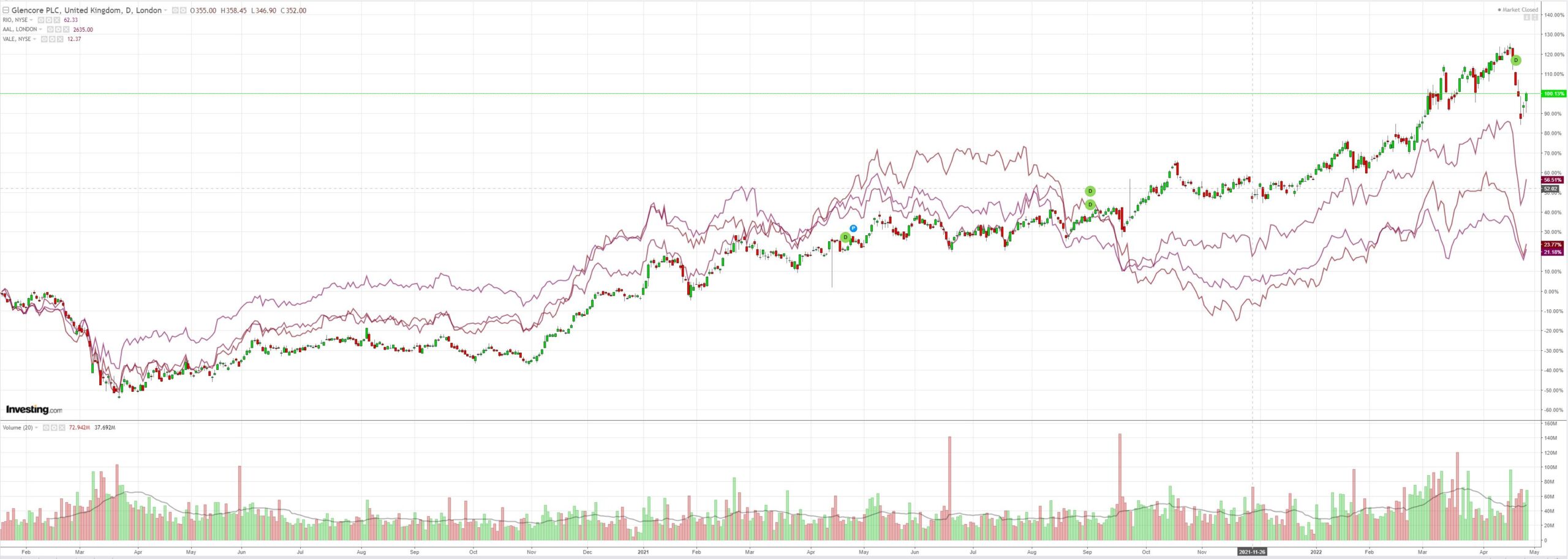

Ditto miners:

Advertisement

EM stocks are trash:

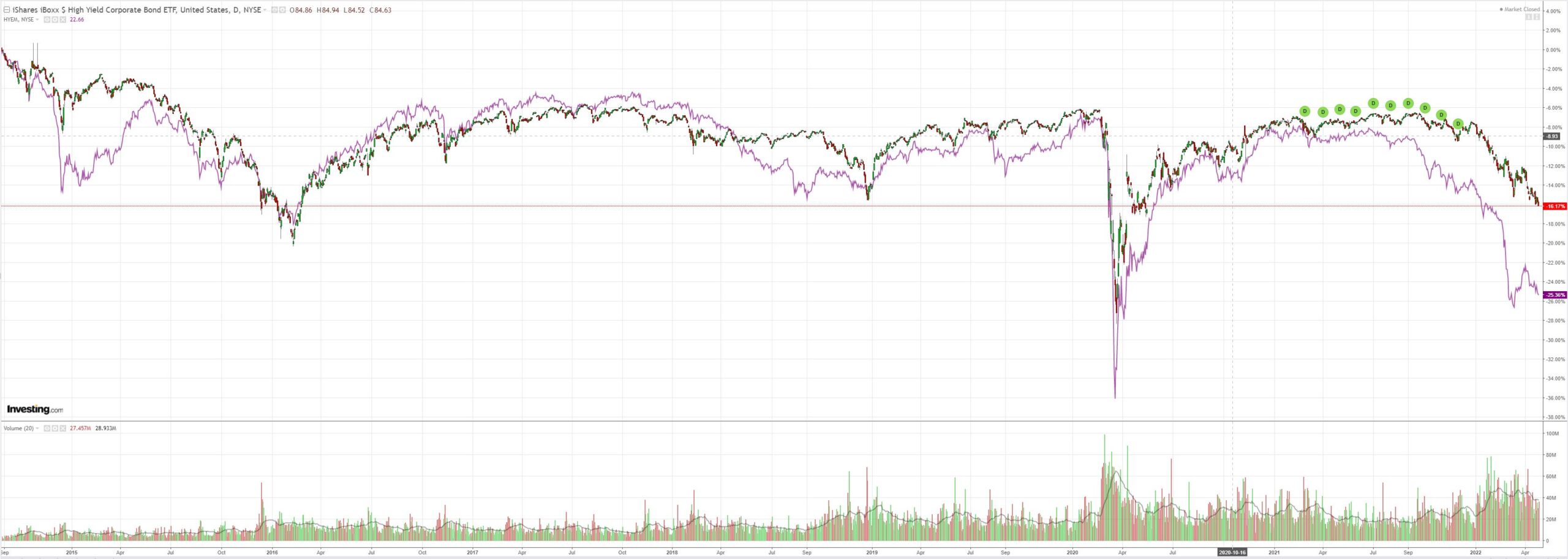

Junk is trashier trash:

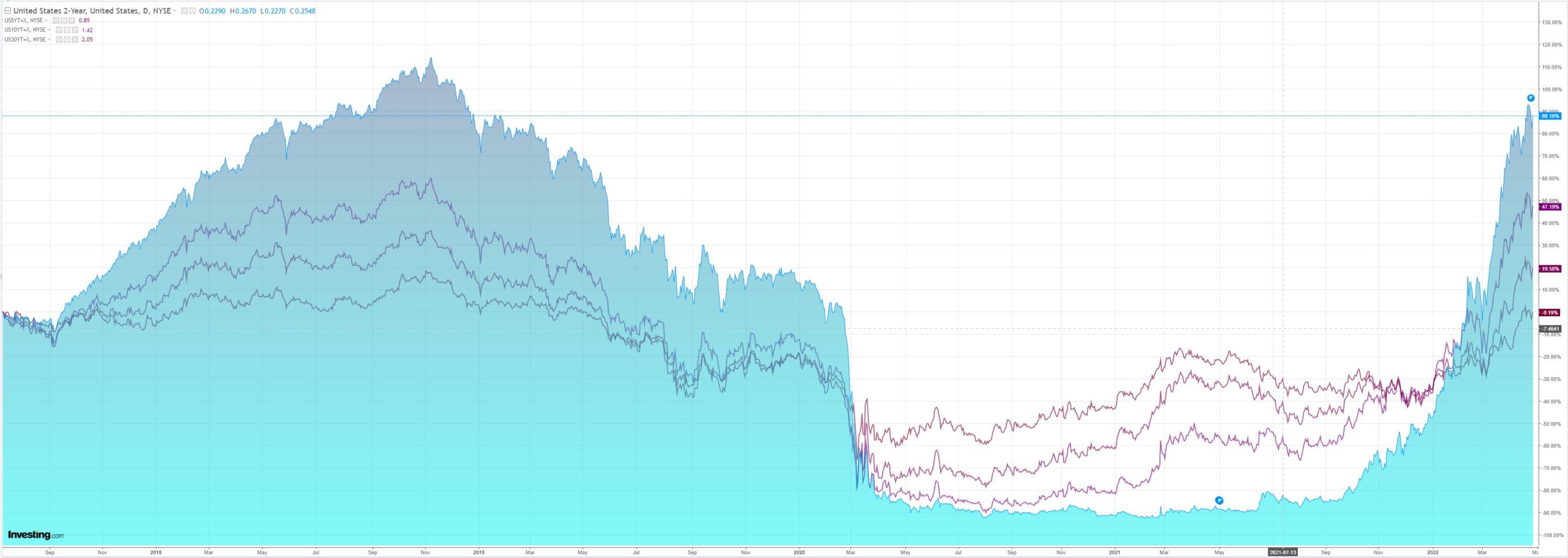

Yields managed to gain:

Advertisement

Stonks too but, like oil, they have the exact reverse pattern of DXY:

Westpac has the wrap:

Advertisement

Event Wrap

US pending home sales in March fell 1.2%m/m (est. -1.0%m/m). NAR Chief Economist Yun referenced a normalising (read “slowdown”) of market conditions as mortgage rates rise. The trade balance for March saw the deficit widen to -USD125.3bn (est. -USD105bn, prior -USD106.3bn), with a surge in imports of over 10%m/m.

German GfK consumer confidence fell to -26.5 (est. -16.5, prior -15.7), France’s at 88 (est. 92, prior 90). UK CBI retail sales index in April fell to 3 (prior 20, est. 11), with sales volumes slumping to -35 (est. 5, prior +9).

Event Outlook

Aust: A slightly lower AUD and higher energy prices in Q1 are set to lift import prices (Westpac f/c: 3.2%) while the surge in commodity prices should significantly boost export prices (Westpac f/c: 11.0%).

NZ: The oil price surge is expected to flow through to the March trade deficit (Westpac f/c: -$200mn). Omicron disruptions have recently weighed on the employment indicators and ANZ business confidence, but each should firm as those issues fade. Notes from RBNZ Dep. Gov. Hawkesby’s speech on macroprudential tools will be released at 9am.

Japan: Supply issues should continue to hamper industrial production in March (market f/c: 0.5%).

Eur/UK: Soaring energy and commodity prices are expected to continue weighing on European economic confidence (market f/c: 108.0) and consumer confidence. Meanwhile, the UK’s Nationwide house prices is expected to post a relatively more moderate gain as rising mortgage rates begin to cool demand (market f/c: 0.8%).

US: The trade deficit and supply-chain issues are anticipated to stunt the annualised pace of GDP growth in Q1 (Westpac f/c: 1.5%; market f/c: 1.1%). Meanwhile, initial jobless claims are set to remain near record lows (market f/c: 180k) and the April Kansas City Fed index should continue to reflect a strong manufacturing outlook (market f/c: 35).

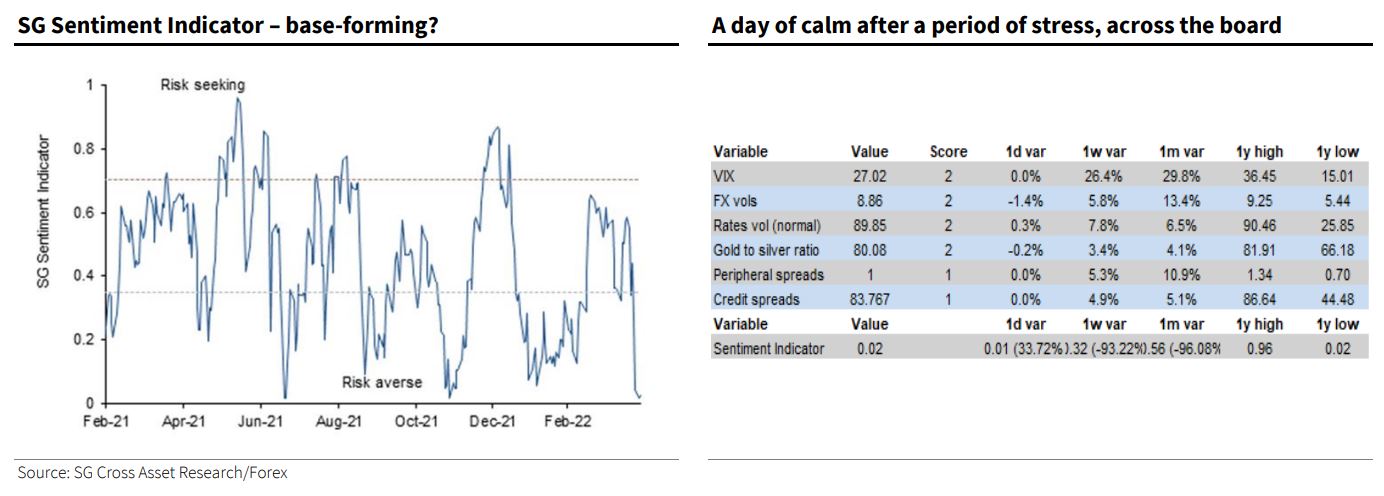

Societe Generale the analysis:

Pressure was building into the weekend, but yesterday morning’s stormy markets may have helped clear the air. The SG Sentiment indicator (see the chart below), almost fell to zero yesterday, a level last seen in March 2020. All the components of the index were showing signs of stress, with volatility (FX, rates and equity) at elevated levels. The Chinese authorities seem to be trying to instil some stability into USD/CNY, bond yields have steadied for now and equity indices too, are finding a toehold.

All of which is lovely, but will it last? I doubt it. The war in Ukraine seems more likely to drag on than end soon, and as well as the human suffering that implies, further tension between Russia and the west seems inevitable. Energy flows can be interrupted at any point, too. Were it not for the war, I’d be keen on buying this euro dip, but as it is, there is more downside and positioning provides no support. The fact that the rates market prices in an implausible 75bp of rate hikes this year, doesn’t add to negative pressure on the currency (if the ECB raised rates to above zero this year, I’d be bullish of the euro, regardless of whether it was priced in) but the economic threat from the conflict is simply too great to buy dips yet.

If we want to buy a beaten-up currency for a short-term trade, we’re more inclined to look at the yen. Olivier has recommended options trades that benefit from a correction, and if Chinese authorities try to stabilise the yuan (because they don’t like disorderly market moves), while US long-term investors are tempted to buy longer-dated Treasuries, we could see a move closer to 120, even if that were only a temporary stop on the way to a peak above 130.

A period of calm in USD/CNY would also be a sign for us to buy AUD and NZD. Both are vulnerable to protracted Chinese economic weakness, but a lot of that is priced in and monetary policy normalisation is more important, while the boost from an eventual reacceleration of Chinese growth can’t be forgotten. However long it takes for current Covid policies to work, they are still temporary, rather than permanent.

Things are certainly stretched. But the Chinese problems are as enduring as the European to my mind. Easier to fix, sure, but Xi is not for turning. The Fed is still coming.

I’m a seller of all rallies in the AUD, EM, and commodity complex.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.