BofA with the monthly fundie survey. Note the extreme commodities long into extreme global recession risk. Everybody is positioned for stagflation but if we get the growth shock instead then they’ll all be forced to puke commodity positions. This hoarding is where the shortages are coming from not fundamentals.

—

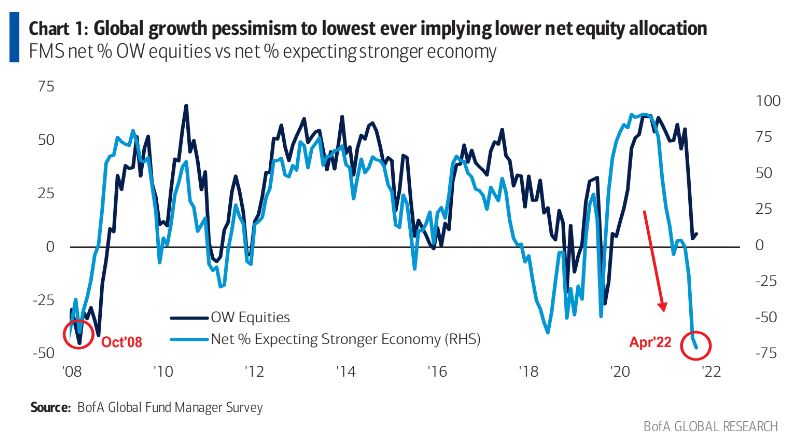

FMS bottom line: April FMS is bearish as fear of fast & furious Fed sends global growth optimism to all-time low, keeps Wall St stability risks high; though not as bearish as war-shocked March FMS, sentiment is poor (BofA Bull & Bear Indicator back down to 2.0 “buy signal”); we remain in “sell-the-rally” camp as Profit-Policy set-up means Jan/Feb sell-off was appetizer not main course of’22 (Chart 1).