The Council of Financial Regulators (CFR) – the coordinating body for Australia’s main financial regulatory agencies and comprises APRA, ASIC, RBA and Treasury – this week released its quarterly statement, which suggested that macro-prudential mortgage restrictions are still on the agenda with the focus likely to be on curbing highly leveraged mortgage lending:

A particular focus of the discussion was the increased share of loans with a high debt-to-income (DTI) ratio. Members discussed the actions being taken by banks to manage the risks within their portfolios, and will continue to assess the need for further macroprudential measures. It is important that lending standards are maintained and that borrowers have adequate buffers, especially in an environment in which housing loan interest rates are at historically low levels and are expected to rise over time in line with the economic recovery.

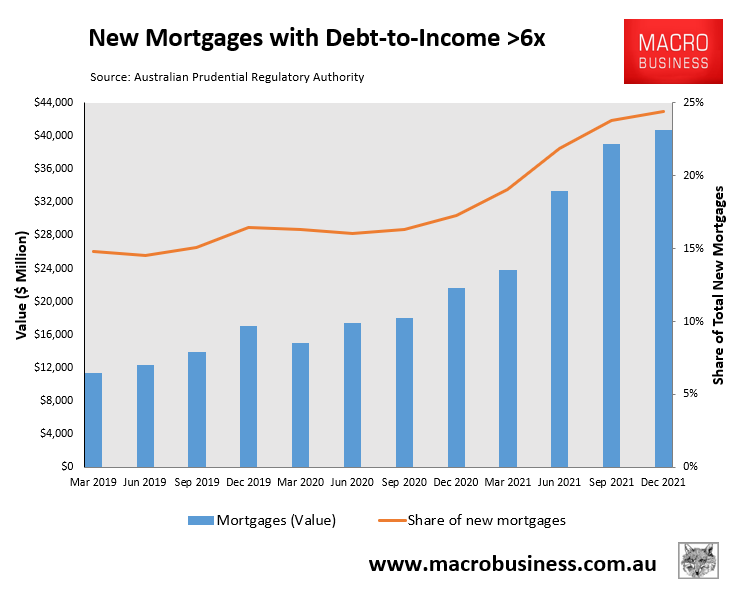

According to the latest APRA disclosures, the percentage of new mortgage lending at debt-to-income ratios of six or more also rose to a record high 24.4% in the December quarter, up from less than 15% in early 2019:

Highly leveraged mortgage lending is booming across Australia.

Since March 2019, $264 billion worth of mortgages have been originated across Australia with a DTI of 6 or above, suggesting there is a large pool of borrowers that are extremely sensitive to mortgage rate increases.

Thus, belatedly introducing macro-prudential mortgage curbs against high DTI borrowing would be akin to shutting the farm gate after the horse has already bolted. These rules should have already been in place to prevent the build-up of highly leveraged mortgages.

As usual, the CFR is acting reactively rather than proactively.