We’ll get the inflation number today and it’ll blow out. The central bank should look straight through it. Why?

Because there is a mounting deflationary shock globally as Europe is rocked by a war and energy shock. China is rocked by a property and COVID shock. And the US is rocked by an inflation and interest rate shock.

A global recession is on the way and it will automatically deflate prices, probably sending them deeply negative in 2023 in a rerun of what happened in the post-Spanish Fly great deflation of 1920/21. Equity markets are beginning to price this, and it is coming faster than anybody realises.

If this is the case, then there is no commodities investment boom coming to Australia. There is already enough embedded tightening in the fixed interest rate reset to sink house prices 10%. And the RBA should rather be worried about the unwind of pandemic distortions as supply-side strains collapse into excess.

Australia is lagging this global cycle by a quarter or two so we have the good fortune of not having to repeat others’ mistakes.

Below find UBS on how this playing out in the US even before we see Fed hikes which are coming fast to crash the lot.

—

For several months, media reports have been breathlessly(and repeatedly) reporting that the latest developed economy consumer price inflation data is the highest in decades. As the trend in the year on year rate of inflation has been rising, stories can be recycled month after month, because inflation has always proved to be higher. Economists, however, see inflation as falling over the second half of this year – the peaks in consumer price inflation will take place at different times in different economies, but the trend of falling inflation is a high conviction call. There are three reasons for economists to be confident.

(Some) Prices are already falling

The inflation story last year was simple. In developed economies there was an extraordinary surge in demand for goods – in the US, demand for durable goods surged in away not seen since the ending of wartime rationing in 1946. Consumers had fiscally supported incomes when lockdowns prevented spending – and as restrictions lifted they rushed to spend. Supply also surged, but as the supply surge could not keep up with the demand surge there was an imbalance. The result was a mix of shortages, and price inflation.

Economists knew that the pandemic savings could not last and thus the demand surge could not last, which was why the inflation was labeled transitory. And, indeed, the demand surge has not lasted (fading first in the US, and later elsewhere). The related inflation has proved to be transitory. The supply-demand imbalance has shrunk, and in some areas markets may even have to consider excess supply at some point. The result is that inflation rates for products affected by the supply demand imbalance are starting to fall as demand slows. For some products, inflation is turninginto outright deflation.

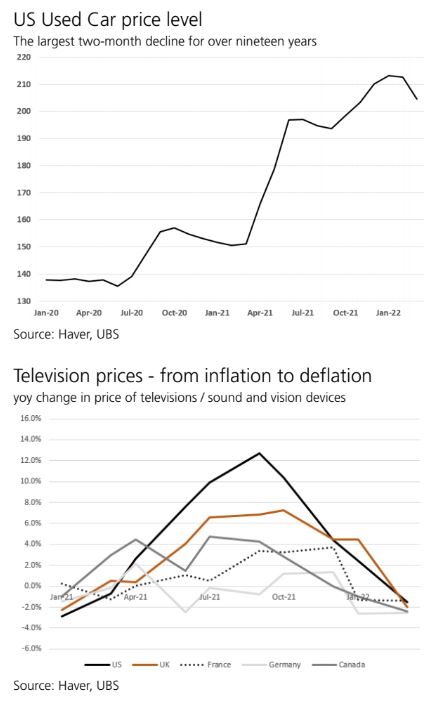

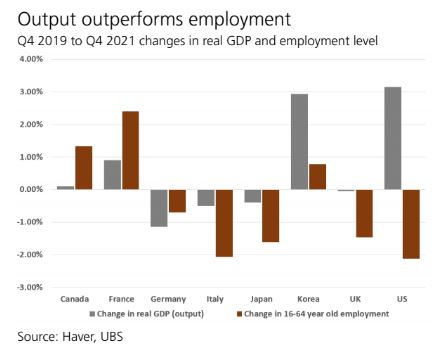

Lower inflation and outright deflation in developed economies can be seen in exactly the areas where demand soared and then fell. Used cars and televisions saw unusual increases in prices last year, and now prices are tumbling.

Inflation can also be self-destructive – higher prices reduce demand, leading to lower prices. US households have been paying higher prices for fuel recently, meaning that they have less money to spend on other items. Lower income households in particular have had to cut back on other spending, and this slowdown in demand is relevant for non-fuel prices. Thus, in March prices in US fast food restaurants had their biggest monthly drop in twenty years (although prices are still higher than a year ago).

Base effects start comparing normal to normal

It is always worth remembering that inflation is all about the change in prices – and so a year on year inflation rate tells us something about price pressures today, but also about price pressures a year ago.

During the first quarter of 2022, the year on year inflation rate was comparing a normal economy (more or less) with the lockdown economy of first quarter 2021. Inevitably moving from “lockdown” to “normal” will involve a large price change. As we move through the second quarter, the comparison will change. First we will be comparing normal in 2022 with reopening in 2021. Later, we will be comparing normal in 2022 with normal in 2021. By the time the comparison is “normal” to “normal” the price change should be quite muted.

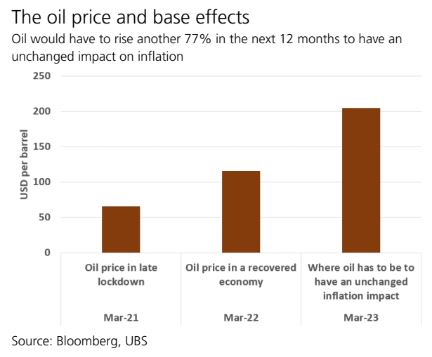

Prices normally go up – falling prices are relatively unusual. If prices go up more quickly, inflation rates (the change in prices) will rise. If prices go up more slowly, inflation rates will slow. Thus higher oil prices this year are likely to lower the rate of inflation. In the year to March 2022 crude oil prices rose 77%, driving up headline inflation. As long as oil price srise less than 77% over the next 12 months (meaning a Brent crude oil price level below USD205), oil will contribute less to the future rate of headline inflation.

Wage costs are not spiraling

Labour costs are the largest component of an inflation basket. In developed economies the processing, packaging, distribution and advertising of everything we buy uses enormous amounts of labour. If labour costs are rising at a faster and faster pace, it will be difficult for inflation to fall.

Wages are not the same as labour costs. If people are working harder, they can be paid more without causing inflation. And that is what is happening.

Across many developed economies, economic output (GDP)is near or above the pre-pandemic level. But employment is below pre-pandemic levels. In other words, fewer people are working harder to produce more stuff. Paying fewer people higher wages if they are doing more does not raise wage costs.

It is also important to distinguish between one off corrections in wage costs, and a continuous increase in wages. For instance, the increase in demand for goods(rather than services) and the rising share of online retail increased demand for delivery drivers. When there is a shock increase in demand for labour, wages will rise until enough people are attracted to the jobs. This is one reason why wages for delivery drivers rose. However, once wages are high enough to attract sufficient workers, there is no need for wages to keep rising at the same pace – a one off shock increase in demand is met with a one of shock increase in wage costs, and then more normal behaviour.

Inflation to fall

The pandemic was an extraordinary economic shock, as was the scale of the policy response. It has produced extraordinary inflation in consequence. Indeed, given the pent-up demand created by pandemic-related limits on spending and exceptional income support, one of the biggest surprises is perhaps that inflation has been as modest as it has.

As the world moves further and further away from the pandemic, it moves further and further away from the extraordinary economic consequences. Demand is normalising, and companies that had pricing power when demand was unimaginably high are finding that they do not have the same pricing power now demand is low. We have been looking at past prices as much as current prices- with the year on year comparisons forcing us to look back to lockdowns. In the coming quarter we will finally leave lockdowns behind us as the backward looking comparisons will come to an end. And finally, there is no evidence of the second round effects of inflation emerging – a wage cost / price spiral (which would be a very troubling signal for inflation) is notably absent.

Economists are rightly confident in the view that inflation is going to fall.

What is less certain is how low inflation will go.