Westpac consumer sentiment falling away before any RBA action. Just imagine what it will do if we see the 14 straight rate hikes interest rate futures are forecasting!

—

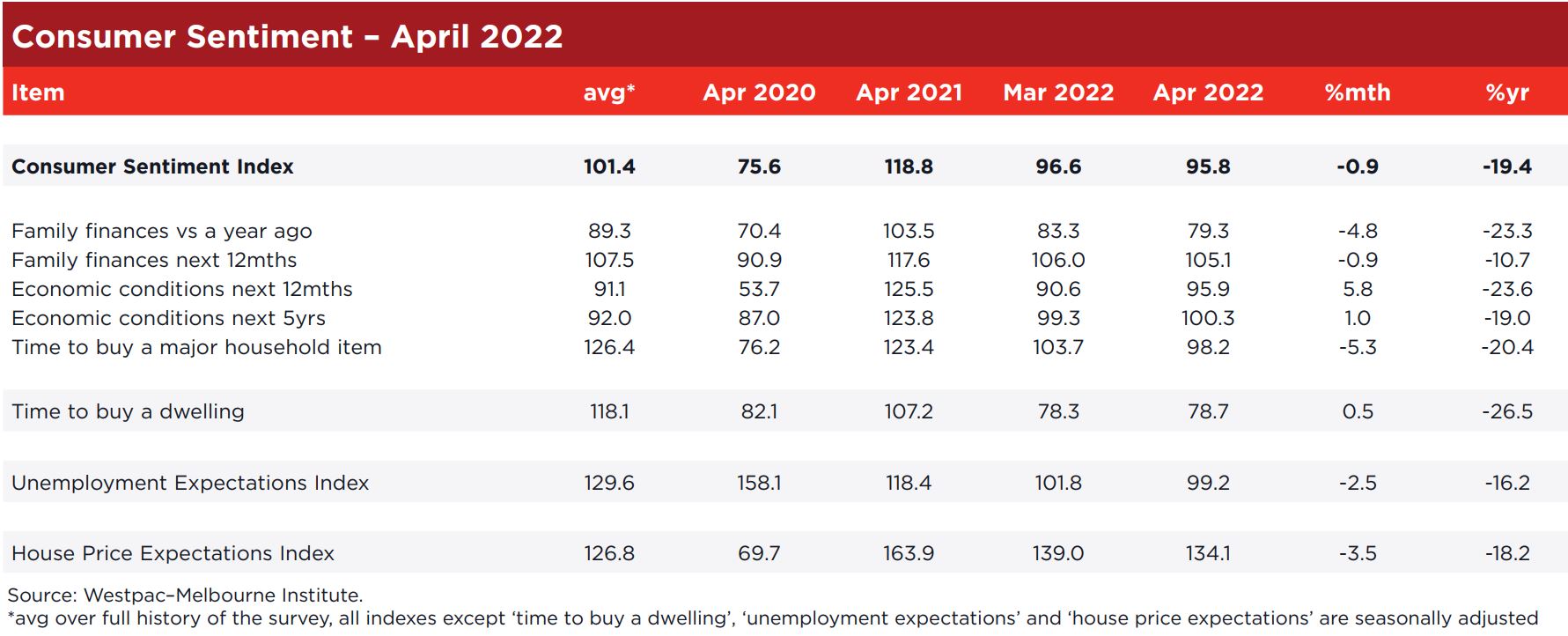

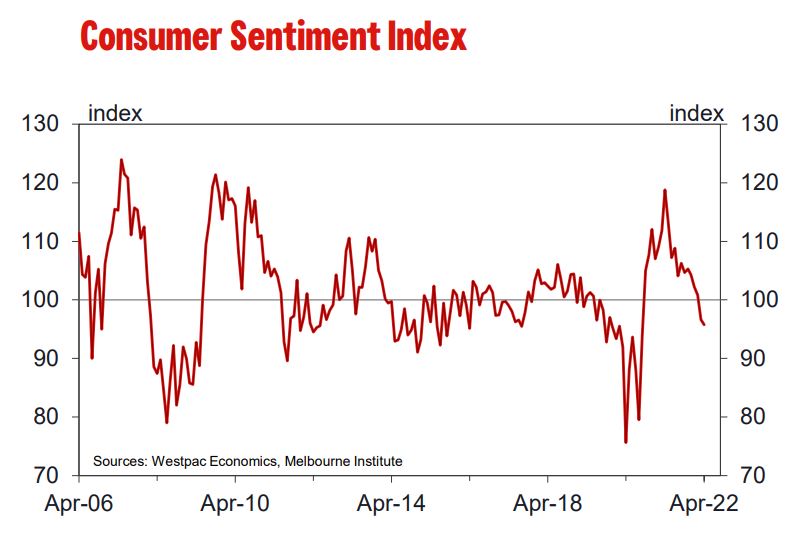

The Westpac-Melbourne Institute Index of Consumer Sentiment fell by 0.9% to 95.8 in April from 96.6 in March.

This modest decline follows the sharp 4.2% fall in March. At that time concerns around interest rates and inflation were starting to weigh on confidence. These were compounded by Russia’s invasion of Ukraine, an associated spike in petrol prices, and severe weather events.

Positive factors over the month that may have moderated the overall weakness included the Federal budget; further strength in the labour market; and a significant fall in petrol prices.

The April Index read is the lowest since September 2020, when COVID pandemic fears were dominating. Recall that prior to the pandemic the Australian economy was lacklustre, weighed down by persistently low wages growth and a cautious consumer. In fact, the average print for the Index in the six months before the pandemic was 95.3 – in line with the current level.

Last month’s detail pointed to geopolitics, floods, inflation, and interest rates as the key explanations for the sharp fall in the Index. There is further evidence that interest rates ; inflation and weather continued to unnerve consumers in the current survey.

Confidence amongst respondents with a mortgage fell by 9.2% in April amid concerns that the Reserve Bank will be raising the cash rate earlier than previously expected and at a faster pace.

Responses to a separate question on mortgage rate expectations show that 70% of consumers expect rates to rise in the next 12 months, up from 67% last month. However, there has been a notable lift in the proportion of consumers expecting rates to increase by more than 1ppt, from 30% in March to 36% in April.

Notably, the prospect of interest rate rises may have buoyed sentiment across some sub-groups that stand to benefit.

Confidence posted significant gains amongst those aged over 65 (+7%) and amongst freehold homeowners (+5.5%). These are segments without large mortgage debts that are also more likely to depend on interest incomes.

Further evidence of the impact of inflation on confidence came from the 5.3% fall in the ‘time to buy a major household item’ sub index. This index is now 22% below its long-term average and has fallen by 10.7% in the last six months. The weakening has been broadly based, across nearly all of the thirty-odd sub-groups we monitor (including age ; income ; and vocation).

This is a strong indication that the decline is being driven by a broad-based factor such as rising prices.

The geographic detail also showed more pronounced declines in areas affected by recent flooding with wet weather continuing through March and early April. Confidence indexes covering regional NSW and regional Queensland both recorded double-digit declines in the latest month.

The Federal Budget was announced by Treasurer Frydenberg in the week prior to the April survey. Since 2010 we have asked consumers about the expected impact of the Budget on their finances over the next 12 months. Apart from the two Budgets handed down during the pandemic – both of which provided generous policy support measures – the proportion of respondents reporting ‘worsen’ has always outnumbered those reporting ‘improve’ .

The latest Budget has seen a return to that pattern with the proportion expecting to be worse off again larger than the proportion expecting an improvement with a ‘net balance’ of –7.2%. That should be seen by the Government as a relatively satisfactory result given that it is in line with the response to the Budget in 2019 (–7.4%), better than the net balance of responses in 2018 (–9.1%) and 2016 (–9.8%), and far less negative than the response to the other Budgets in 2010 to 2017 which ranged between –17% (2010) and –56% (2014).

The sub-group detail suggests some of the ‘cost of living’ measures in the Budget were relatively well-received. Those in lower income groups reported better Budget assessments than in 2021 and most 18-24 year olds (a segment known to be particularly sensitive to high fuel costs) viewed the Budget as a positive.

The temporary halving in excise duty announced on Budget night has seen average pump prices fall 23c to $1.54/litre in early April, from $1.78/litre during the last survey.

The overall sentiment Index posted a strong gain amongst those on low incomes (+7.6%). The Budget likely played an important role in this response with one-off tax relief and cost of living payments for pensioners and beneficiaries providing targeted support for low and middle income households.

Budget reactions also had a clear impact on wider sentiment across different voter groups. Confidence amongst Coalition voters lifted by 7.6% while ALP supporters showed a fall of 5.5%.

The component detail showed that interest rate and inflation concerns weighed on assessments of finances although there was some improvement in expectations for the economy.

The ‘finances compared to a year ago’ sub-index showed the most significant weakening, down 4.8% in the month to 79.3, well below the long run average of 89 and the weakest read since the pandemic. Near term expectations for finances are more positive and more resilient. The ‘finances, next 12 months’ sub-index dipped only 0.9% and remained in ‘net positive’ territory at 105.1.

Consumer views on the economy improved, particularly for the near- term outlook. The ‘economy, next 12 months’ sub-index posted a solid 5.8% recovery to 95.9, albeit still down on its level in February. The ‘economy, next 5 years’ sub-index rose 1% to 100.3 but was also below its level two months ago.

The labour market remains a strong cornerstone for confidence. The Westpac–Melbourne Institute Unemployment Expectation Index improved 2.5% in April. The index read of 99.2 is the second lowest level since the mid-1990s (lower reads mean more consumers expect unemployment to fall rather than rise).

With the unemployment rate already at 4% and job vacancies holding near record levels, Australia’s labour market is clearly tight. Westpac recently lowered its forecast for the unemployment rate by year’s end to 3.2% – almost uncharted territory for Australia which has not seen unemployment rates materially below 4% in the best part of 50 years.

Conditions in the housing market were mixed in April. Buyer sentiment held steady at weak levels. Price expectations showed a further softening while remaining in positive territory overall.

The ‘time to buy a dwelling’ index nudged 0.5% higher but was coming off a 14-year low in the previous month and around 40% below its most recent peak in November 2020. High prices, rising fixed mortgage rates and the expectation of rises in variable mortgage rates continue to weigh on affordability and confidence in the housing sector.

The Westpac–Melbourne Institute House Price Expectations Index fell by 3.5% to 134.1. Most consumers still expect prices to rise over the next 12 months but the view is becoming less widespread. At the index peak of 163.9 a year ago, 70% of consumers expected prices to rise. Today that proportion has declined to a little over half (54.5%).

Notably, the balance has tipped a lot further in NSW and Victoria with state index reads in the low 120s and less than half of consumers in these states expecting prices to rise in the year ahead. Both state indexes recorded sizeable falls in April: NSW is down 9.5% and Victoria by 12.3%. That follows recent updates showing prices in Sydney and Melbourne have flat-lined since late last year.

The Reserve Bank Board next meets on May 3. Last week Westpac brought forward its forecast for the first rate increase in the cycle from August to June following the Governor’s Statement after the April Board meeting. The Board is no longer emphasising ‘patience’. In fact, the Governor emphasised that the Board will be reviewing the data releases “over coming months” – phrasing that points to a June lift off.

This guidance seems to rule out the prospect of a rate increase as early as the May Board meeting although markets are certainly discussing that prospect.

Once the tightening cycle begins, we expect a series of rate hikes in most months in 2022 with a pause in September by which time the emergency cuts from 2020 will have been reversed. Further increases can be expected in the first half of 2023 as wage pressures threaten the outlook for inflation. We expect the cash rate to peak around 2% in the cycle by June next year.