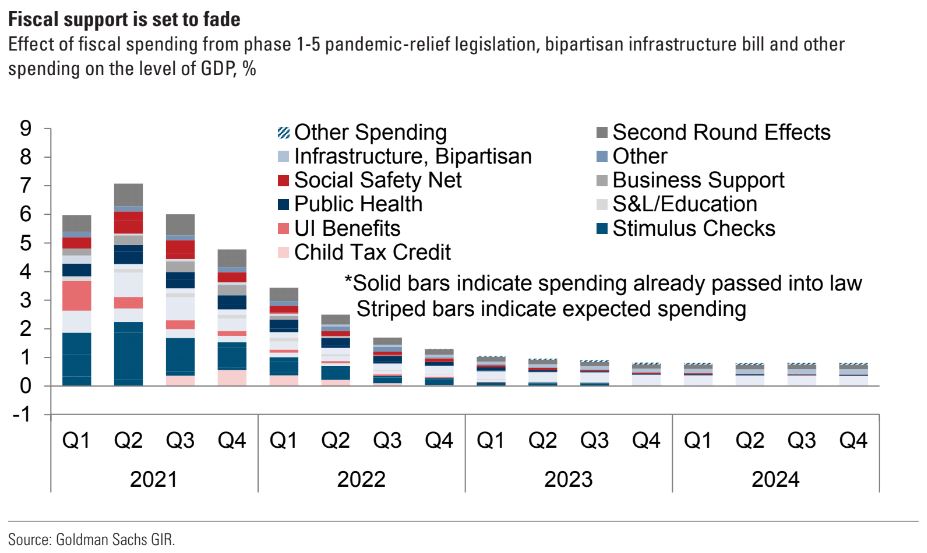

While inflation reached its fastest yearly pace in March since the early 1980s, we believe headline and core CPI should gradually subside throughout most of the rest of the year, and reach 5.7% and 4.5%, respectively, by YE22. That said, we believe that easing current strong wage growth and tightness in the labor market, where conditions are the most overheated in postwar history based on the 5.3mn gap between total available jobs and workers, will require growth to soften to a modestly below-trend pace—enough to persuade firms to shelve some of their expansion plans, but not so much as to trigger sharp cuts in current output and employment. We expect a substantial drag from fiscal policy will do a significant part of the work, as shown in our chart of the week, though estimating its size is hard because of the interaction with pent-up savings and reopening of the service sector. But the needed growth slowdown also calls for a significant tightening of financial conditions, in our view, which may well require Fed hikes beyond our current modal forecast for a 3-3.25% terminal rate. We think this leaves a narrower path for the Fed to deliver a soft landing, though we still don’t see a recession as the base case and retain our expectation for further US curve flattening despite recent steepening. While the Dollar has historically strengthened going into US recessions, especially against EM currencies, we find that its performance has been more mixed during the actual months of recession and broadly weaker around the trough. For now, we remain structurally bearish on the dollar, but our conviction on its near-term direction is fairly low.

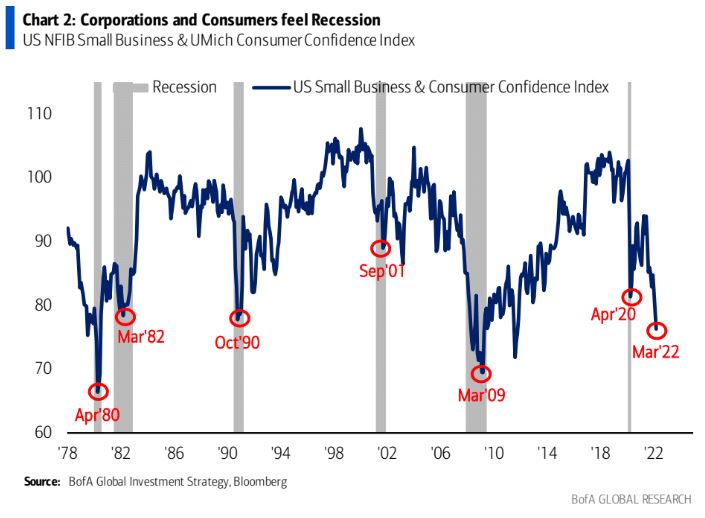

What are the odds of the steepest rise in inflation and interest rates since WWII resulting in a soft landing? Nobody knows. But BofA has a better idea of how long the odds than does Goldman:

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.