Chinese credit had a better month in March. Goldman:

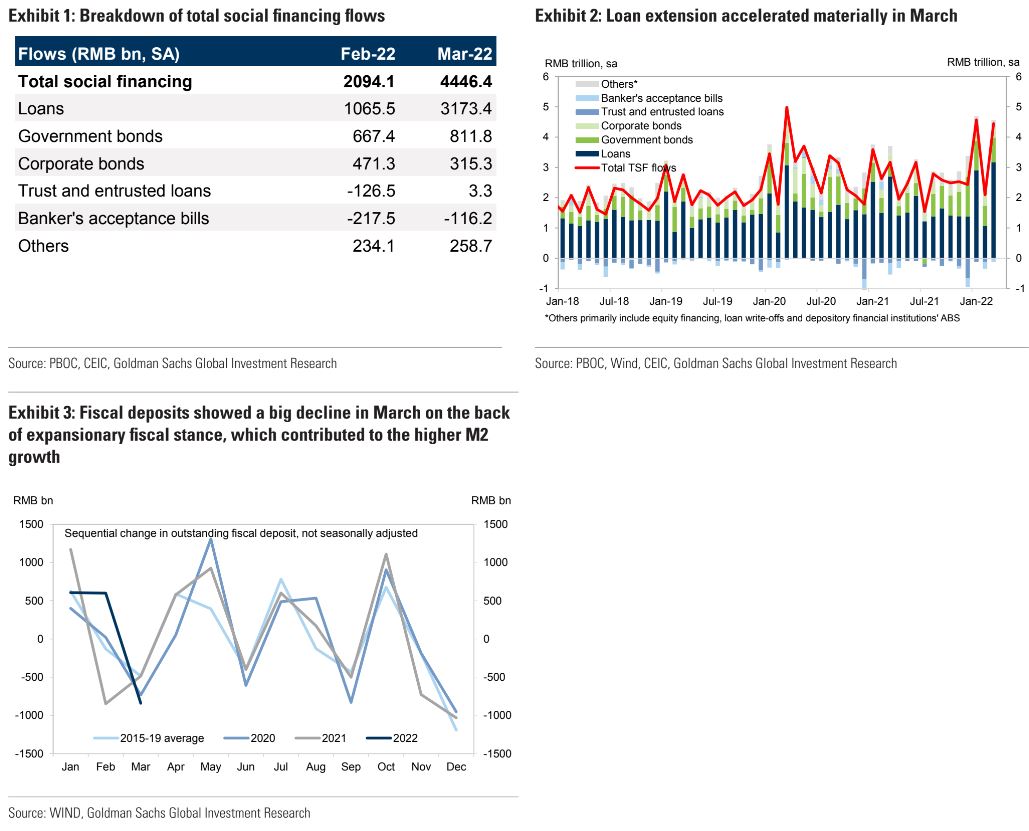

Bottom line: March total social financing, RMB loans and M2 growth accelerated materially and were all well above market expectations on the back of policy support. Composition of RMB loans suggests broad acceleration of loan growth across sectors (with the only exception being household short-term loans, which might reflect the drag from anti-pandemic measures because short-term household loans are typically consumption loans), however bill financing growth was still much faster than medium-to-long term loan growth, which continued to imply weak credit demand relative to credit supply.

Key numbers: New CNY loans: RMB 3130 bn in March (RMB loans to the real economy: RMB 3233 bn) vs. GSe: RMB 2800bn, consensus: RMB 2750bn. Outstanding CNY loan growth: 11.4% yoy in March (18.1% SA ann mom, estimated by GS); February: 11.4% yoy (13.2% SA ann mom). Total social financing (flow, reported): RMB 4650bn in March, vs. GSe: RMB 3500bn,

consensus: RMB 3550bn. TSF stock growth (after adding all government bonds) was 10.6% yoy in March, faster than the 10.2% in February. The implied month-on-month growth of TSF stock accelerated to 14.4% (seasonally adjusted annual rate) from 11.5% in February. M2: 9.7% yoy in March (+24.4% SA ann mom) vs. GSe: 9.0% yoy, Bloomberg consensus: 9.4% yoy. February: 9.2% yoy (+11.3% SA ann mom estimated by GS).

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.