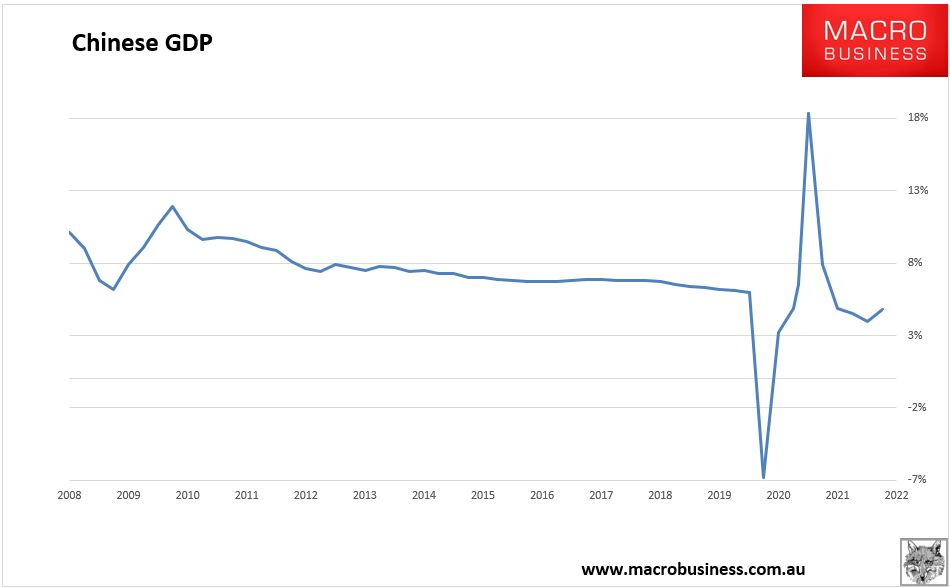

As expected, Chinese data is holding up OK on the usual CCP data massaging, but under the bonnet, the economy has crash-landed.

Growth for the March quarter came in at 1.3% and YoY at 4.8%. Both were far ahead of expectations:

The March activity data tells the truth. Industrial output was 5% YoY, fixed asset investment was 9.3% but retail sales dropped 3.5%. All dropped sharply from February,

Advertisement