Alan Kohler has labelled Australia’s housing market a “disaster” that has “fundamentally transformed society” for the worse after prices rose 960% since 1980.

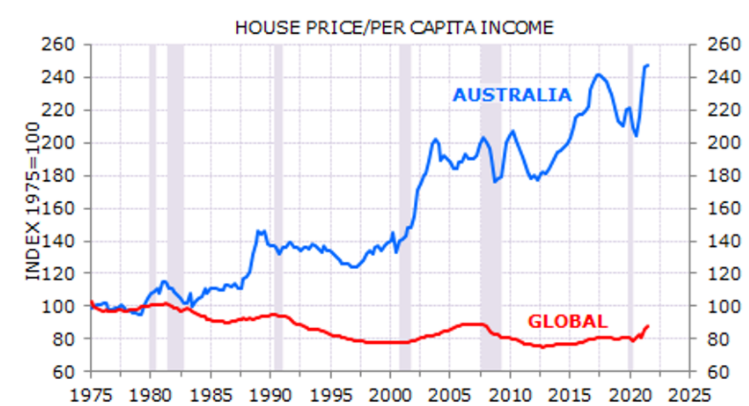

Kohler sites data from economist Gerard Minack, which shows that while affordability in Australia has badly deteriorated, houses have actually become cheaper globally relative to income:

Sources: Bank for International Settlements; Minack Advisers.

This extreme house price growth, alongside Australia’s ballooning household debt load (ranked second highest in the world), means that “as far as the Australian economy is concerned, house prices are everything”.

Kohler also blames the nation’s broken housing system for increasing inequality, while noting that Australia’s high household wealth is largely meaningless because shelter is a basic need that we cannot simply cash-out:

Rising house prices do not create wealth, they redistribute it… It means the level of household wealth is both meaningless and destructive…

Sell your house and you have to buy another one, or your children do…

It’s destructive because of the inequality that results: With so much wealth concentrated in the home, it stays with those who already own a house and within families. For someone with little or no family housing equity behind them, it’s virtually impossible to break out of the cycle and build new wealth.

The growth in the value of land has fundamentally changed society, in two ways: First, generations of young Australians are being impoverished by the cost of shelter…

Education and hard work no longer determine how wealthy you are; now it comes down to where you live, and what sort of house you inherit.

It means Australia is no longer an egalitarian meritocracy: Material success is a function of geography and class, not accomplishment.

Kohler even gives yours truly a compliment for calling out the “housing affordability” crocodile tears pouring from the Coalition’s latest faux housing inquiry:

One of the pithiest comments came from the submission of Leith van Onselen of the newsletter MacroBusiness, who wrote, among other things: “Let’s get real and admit that this inquiry is a waste of time and taxpayer’s money”. And so it was…

What the standing committee’s report should have said is that the level of house prices and debt in Australia is a blunder, perhaps the biggest policy mistake in 50 years.

If Labor wins the election there will have to be another inquiry, but at least the same submissions can all be re-used.

Bravo Alan Kohler. I’ve been challenging Australia’s housing system since the inception of MacroBusiness, and have watched it go from bad to worse. It’s great to see that I am not alone in calling out the endless housing affordability bunkum.

I’ll see you at the next faux affordability inquiry. And then the one after that!