Westpac with the note.

—

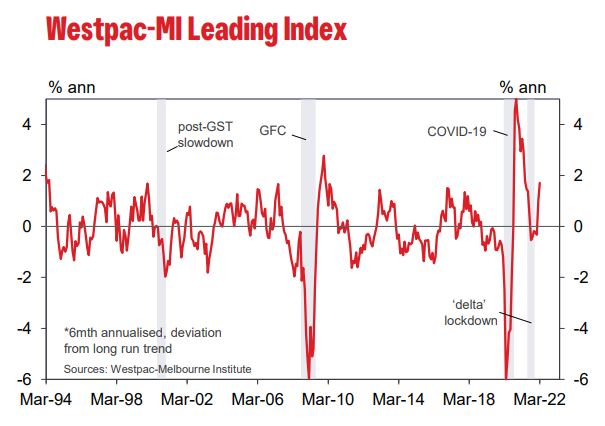

This is the fastest growth rate of the Index since May 2021. The growth rate in the Index had been slowing through the first half of 2021 from the explosive recovery in October 2020 (peak monthly growth rate in November 2020 of 4.96%) as the economy emerged from the initial Covid related lockdowns in 2020.

With the Delta lockdowns in NSW and Victoria leading to a contraction in growth in the September quarter last year and a rebound in the December quarter it is very welcome to see these encouraging signals from the Leading Index in the early months of 2022 that growth prospects for the next 3 to 9 months are encouraging.

They are consistent with Westpac’s upbeat view of the growth momentum in the economy for most of 2022. We expect growth in 2022 of around 5.5% with more than 70% of that growth being concentrated in the June and September quarters.

That will be driven by the rapid recovery in spending associated with the significant easing of pandemic restrictions. Households are expected to boost spending through further reductions in the savings rate including some drawing down some of their excess savings that have been built up through 2020 and 2021.

As we move through 2022 rising interest rates and a contraction in real wages will begin to bite and spending will slow.

Growth prospects for 2023 and 2024, which are beyond the scope of the Leading Index, are much more subdued than we expect in 2022.

There has been a strong recovery in the Leading Index over the last six months. The growth rate in the Index has lifted from -0.33% in October to 1.71% in March. Positive contributors have been sourced both domestically (particularly in the labour market) and internationally.

The contributors to that lift in the growth rate are: hours worked (0.93 ppt’s); a steepening of the yield curve (0.38 ppt’s); commodity prices (0.33 ppt’s); US industrial production (0.24 ppt’s); dwelling approvals (0.20 ppt’s); and unemployment expectations (0.02 ppt’s).

Modest drags on the Index from the S&P/ASX 200 (–0.04 ppt’s) and the Expectations component of the Westpac Melbourne Institute Index of Consumer Sentiment (–0.01 ppt’s).

In the last month the increase in the growth rate from 1.02% to 1.71% was largely driven by improvements from offshore – S&P/ASX 200 (0.18 ppt’s); US industrial production (0.21 ppt’s) and commodities (0.22 ppt’s). Domestically we saw a bounce back in dwelling approvals (0.26 ppt’s) although some momentary slowing the labour market components of the Index took the edge off the month – hours worked (–0.14 ppt’s) and unemployment expectations ( -0.14 ppt’s). However, hours worked continues to be a very important contributor to the recovery in the Index (contributing 0.43 ppt’s to the growth rate).

The Reserve Bank Board next meets on May 3. Following the April Board meeting the Governor explicitly deleted reference to the Board being patient with its approach to policy. He also noted that “Over coming months important additional evidence will be available to the Board on both inflation and the evolution of labour costs.” That suggests to us that the Board will hold rates steady at the May meeting but be prepared to move at the next meeting on June 7.

Further evidence that the beginning of the rate hike cycle is close came in the Minutes to the April meeting where global inflation and the actions of other central banks, including the United States, were given much more emphasis than in past reports.

Westpac expects a lift of 15 basis points in the cash rate on June 7, with 25 basis point increases at most subsequent meetings in 2022 reaching 1.25% at the end of the year.

In 2023 we expect three further increases of 25 basis points with the cash rate peaking at 2% in June.