Aussie house prices to crash 73% on 14 straight interest rate hikes

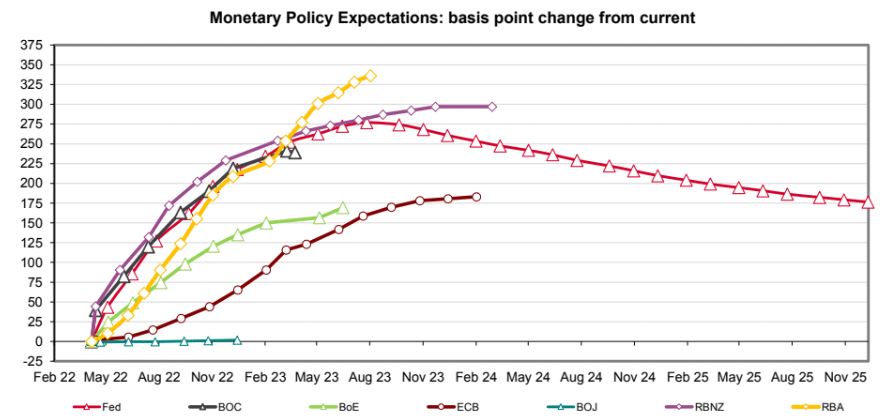

It’s a laugh a minute now for house price bears. Interest rate markets are now pricing nearly 14 straight interest rate hikes from the RBA by mid-2023:

The recent bottom for the fixed interest-rate mortgage boom, which comprised 90%+ of new issuance, was around 2%. If markets are right, these will be rolling off at an astonishing 7% flexible rate across 2023 and beyond.

Here are the income impacts of this on Aussie households:

Here’s what the RBA says about interest-rate sensitivity and house prices:

At a user cost of 6 per cent we estimate that a sustained percentage point drop in interest rates would, in the long run, boost housing prices by 17 per cent, holding rents and other components of the user cost equal. This semi-elasticity (the proportionate increase in housing prices for a given percentage point increase in interest rates) is larger than the time series estimates of Abelson et al (2005), perhaps because they control for many other variables affected by interest rates (e.g. share prices and income), so only capture part of the effect of interest rates. Our estimate is similar to Gitelman and Otto’s (2012, p 183) estimate of 20 per cent for Sydney housing prices using disaggregated census data, and Himmelberg, Mayer and Sinai’s (2005, p 78) estimated range of 19 to 33 per cent for the United States in a calibrated model.

A user cost (or rental yield) of 6 per cent is the approximate average over Gitelman and Otto’s sample. User cost models, such as Equation (4), imply that the semi-elasticity increases as the user cost declines. Effects on prices become extremely large as the denominator in Equation (4) approaches zero. With a current user cost of 3½ per cent (well below that observed in the studies above), a percentage point drop in the expected real mortgage rate would boost housing prices by 28 per cent in the long run.

In short, at low-interest rates, house prices volatility is dramatically amplified. Based on the RBA’s own model and a little poetic license, house prices will fall -28% for every 1% hike. This will not happen all at once so let’s give it three years to fully play out:

- Year one -28%.

- Year two -48%.

- Year three -73%.

Obviously, this exercise is more than a little bit rubbery. But it makes a solid if a theatrical point in the broadest sense.

If the RBA smokes the same mull of PCP, ketamine, and crack that interest rate markets do then by mid-2023 the Australian economy will be lying dead in the gutter.