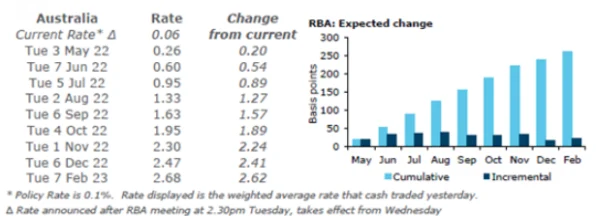

Mwahaha. There’s no sensible caution on interest rate forecasts at the ANZ like there is at CBA. ANZ has gone all-in on a massive ten rate hike cycle with a terminal rate above 3%:

Eventually we see the cash rate reaching into the 3s.

Given the strong inflation print, and reports from the RBA’s business liaison program that ‘wages growth had continued to pick up in the March quarter’, we don’t think they need to wait for more data on wages to conclude that the current inflation will be sustained.

Those twelve rate hikes will sink Sydney and Melbourne property prices by 20-25% is my (and the RBA’s) best guess.

That’s enough to crush the VIC and NSW consumption economies so I can only assume that ANZ also sees some gigantic boom elsewhere in the Aussie economy. Either in exports or public and private investment.

Advertisement

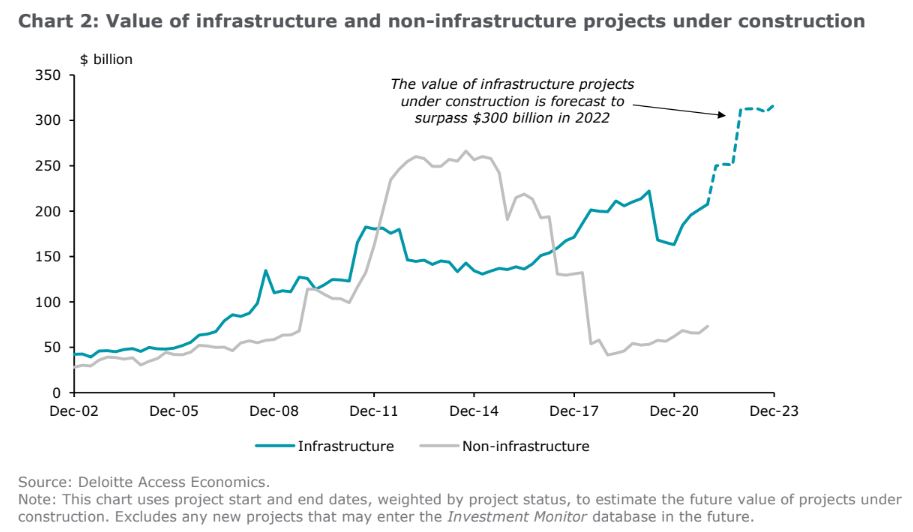

There is a strong fiscal tailwind of infrastructure projects to help:

But that is all for this year. Next year it’ll add nothing to growth as the spending plateaus.

Advertisement

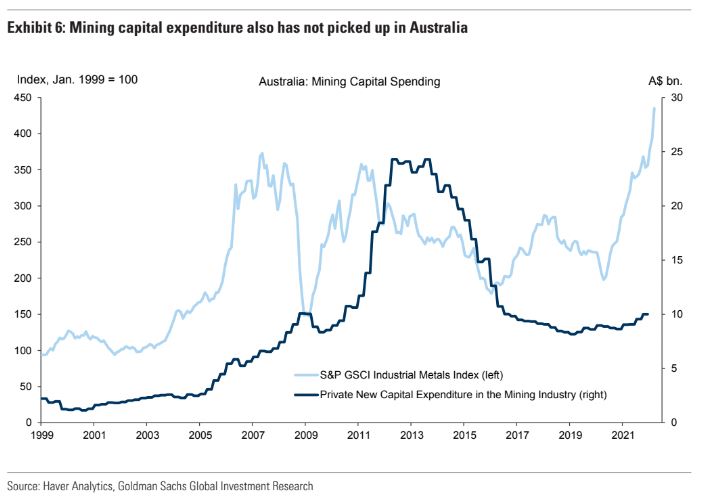

Perhaps it’s another hundred-year mining boom that ANZ is counting on. Prices are signaling the need for it:

The problem is that iron ore is still in a glut. Coal is uninvestable owing to climate change. And gas has largely exhausted the good projects.

Advertisement

Therefore, by definition, there will be no repeat of the post-GFC investment boom because these are Australia’s major three commodities by a country mile.

Westpac is less hawkish than ANZ on interest rates, seeing a total of seven hikes and a peak rate of 2% but it still forecasting a -14% dump in prices house prices:

The more compressed and earlier interest rate tightening cycle also means the rapid run-up in Australian dwelling prices over the last eighteen months is almost certainly over.

Momentum has already slowed in markets where affordability is most stretched, prices have stalled in Sydney and Melbourne.

Buyer sentiment, turnover and auction activity are also pointing to a clear slowdown that should accelerate as official rates rise and the prospect of ongoing increases through the remainder of 2022 confronts buyers and sellers.

Previously we had expected markets to retain some price momentum in the first half of 2022, tipping into correction mode in the final quarter. That momentum has faded already, and the tipping point is closer. Accordingly, we now expect:

• 2022 – prices nationally to finish down 2% – meaning a 4% decline from the current peak (and compared to +2.5% previously).

• 2023 – a further 8% fall in prices, slightly larger than our previous forecast of –7%, as the tightening cycle continues to impact.

• 2024 – a further 1% decline in prices as weakness carries into the first half of the year, only partially offset by a weak recovery in the second half as prices essentially stabilise (compared to –5% previously).

Note that the peak to trough decline is still around minus 14% in nominal terms. We have only lifted the terminal rate by 0.25% from 1.75% to 2.0%.

By the end of 2024 the mix of lower prices and higher incomes will have more than offset the effect of higher rates, restoring affordability to more normal levels for most markets. The initial recovery is likely to remain subdued as rate cuts – an important catalyst for housing upturns – are not expected. The cash rate is forecast to hold at 2% throughout 2024.

Advertisement

My own view is that both will be wrong; that prices will fall faster than most expect and a global recession overtake the Australian economy before the RBA gets very far.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.