Financial comparison site Mozo has updated its average fixed mortgage rate data to end-March 2022.

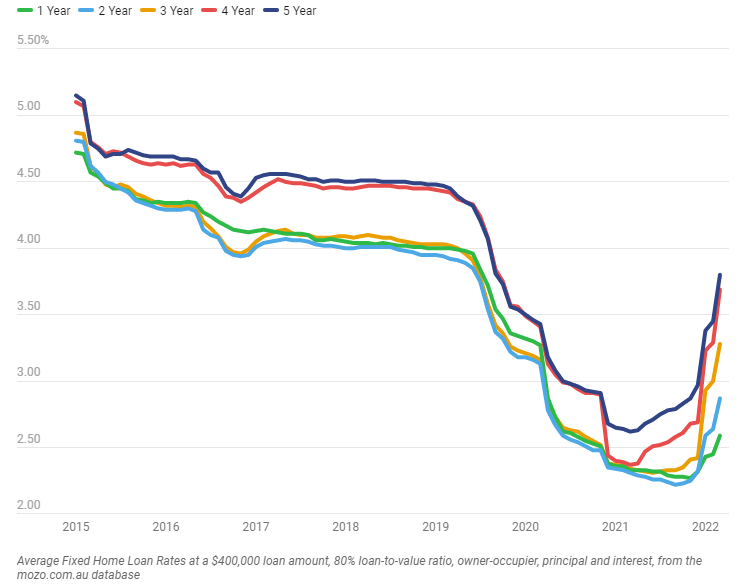

As shown in the next chart, fixed mortgage rates have risen sharply across all terms, with the largest increases happening across the longest duration mortgages:

Australian fixed mortgage rates have soared across all loan terms.

According to Mozo:

- The average one-year fixed mortgage rate has risen from a low of 2.27% in November 2021 to 2.59% as at March 2022.

- The average two-year fixed mortgage rate has risen from a low of 2.22% in September 2021 to 2.87% as at March 2022.

- The average three-year fixed mortgage rate has risen from a low of 2.32% in May 2021 to 3.28% as at March 2022.

- The average four-year fixed mortgage rate has risen from a low of 2.37% in March 2021 to 3.69% as at March 2022.

- The average five-year fixed mortgage rate has risen from a low of 2.62% in November 2021 to 3.80% as at March 2022.

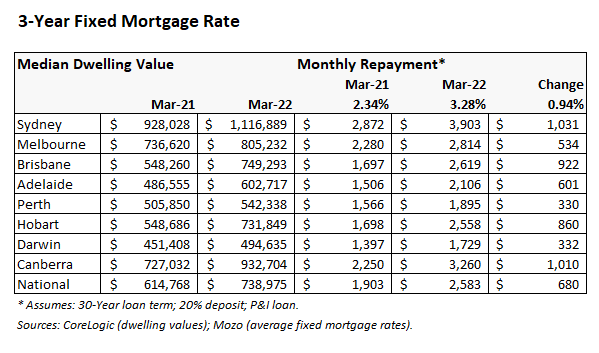

Over the past year, Australian dwelling values have soared in value. Thus, the combination of higher dwelling values combined with the sharp lift in fixed mortgage rates means the median home buyer using a fixed rate mortgage is paying far more in monthly mortgage repayments now than they would have had they purchased a year earlier.

To illustrate, the below table shows the change in monthly mortgage repayments for a purchaser of a median priced dwelling using a three-year fixed rate mortgage between March 2021 and March 2022. Both scenarios assume the buyer used a 20% deposit and a 30-year principal and interest loan term.

At the national level, the typical new fixed rate borrower is paying $680 more per month in repayments than the median buyer did a year earlier.

The situation is worst in Sydney, where the median buyers using a three-year fixed rate mortgage would be paying an extra $1,031 per month in mortgage repayments.

As noted last week, the futures market is now tipping that the Reserve Bank of Australia (RBA) will lift the cash rate from its current low of 0.1% to 3.0% by August 2023.

If rates were to rise in line with the market’s forecast, then mortgage borrowers – whether choosing fixed or variable rates – would experience a very large increase in monthly mortgage repayments.

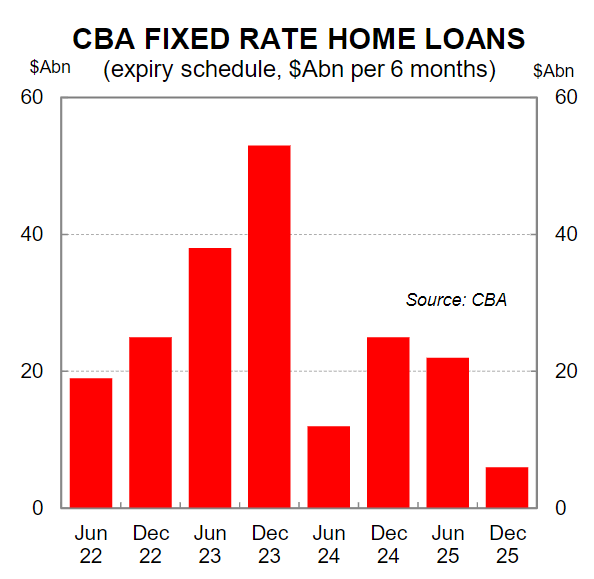

The interest rate shock would be particularly harsh for the many fixed rate borrowers that originated their mortgages in 2021 at rates below 2.5%. Indeed, the CBA estimates there are $500 billion of fixed mortgages due to expire by the end of 2023:

$500 billion worth of fixed rate mortgages are due to expire by end-2023.

These borrowers would face at least a doubling in mortgage rates, which would place many in severe mortgage stress.

If economists and the market is correct and interest rates do soar, then it is going to be a Nightmare on Mortgage Street.