I have no sympathy for the RBA. Once again it has proven to be a terrible forecaster. This time around it lured homebuyers in with promises of cheap fixed-mortgage rates for four years and instead, it is going to double mortgage rates within two years.

Not only that, it has now reset its course for lifting variable rates so that those rolling off their fixed-rate loans will have nowhere to hide.

$500bn in mortgages is about to be hit by the most radical interest rate shock in modern Australian history. Thanks for taking it in the team, kids.

These monetary sacrificial lambs are going to do two things.

First, they are going to sink house prices as mortgage distress roars higher at unprecedented speeds.

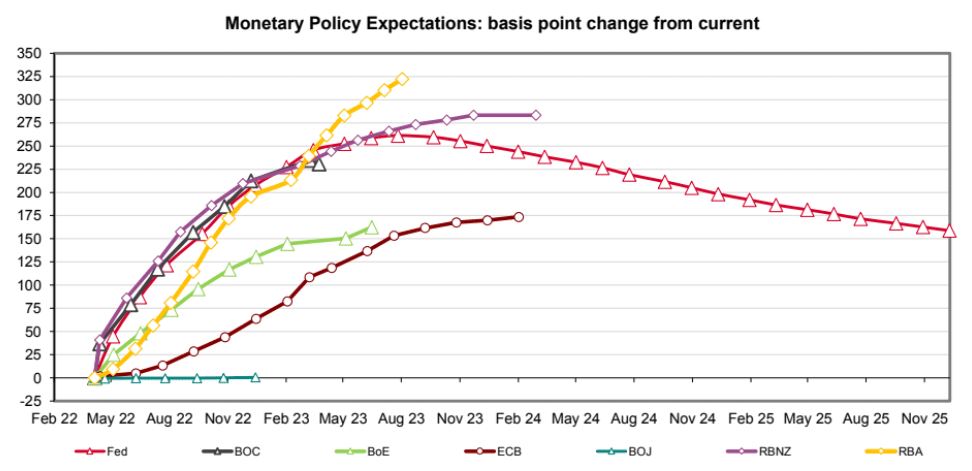

Second, they are going to stall consumption so that’ll prevent interest rates from going anywhere near where markets are forecasting. Now 13 hikes by mid-next year:

The mistake markets are making is in drawing a correlation between the Ukraine war-inspired terms of trade boom and higher interest rates, such as transpired in 2009-10. Higher commodity prices no longer translate to a stronger Australian economy:

- Higher LNG prices subtract from Australian activity owing to captured regulatory structure and taxation.

- Higher coal and iron ore prices will boost budgets but have no investment follow through owing to ECG and oversupply.

- There are some other benefits to softs and green commodities but they are too small to matter much.

- Public budgets will be helped but not passed on much. Stocks are falling with global bourses. Weak resources investment means limited wages pressures.

- There is also the ongoing effort to reboot immigration which will land on wages sooner or later.

That pretty much means the commodity boom is only skin deep so any monetary tightening on the services economy will have little offset in the mining economy, unlike 2009/10.

Worse, a global recession is already on deck as the US inventory supercycle clashes with the Fed, sending a trade shock into a China already on its knees fighting OMICRON and a property bust, plus Europe dying of the very commodity spikes benefitting Australia.

This all looks ominously similar to 2008 when the RBA hiked rates directly into a GFC that the drover’s dog could see coming. Some might argue that there’s no obvious candidate for a credit event this time but they are often hidden until they’re not and the accident may simply be in equities this time:

Blue: G5 Credit Impulse, leads by 12 months

Orange: SPX YoY earnings growth, lags by 12 monthsAfter the fastest credit creation ever recorded since the ’70s, we are now witnessing the sharpest credit impulse contraction.

Less credit.

Less animal spirits.

Lower earnings. pic.twitter.com/5DRiQcTD6t— Alf (@MacroAlf) April 5, 2022

2008 is calling the RBA hotline but nobody is picking up the phone.