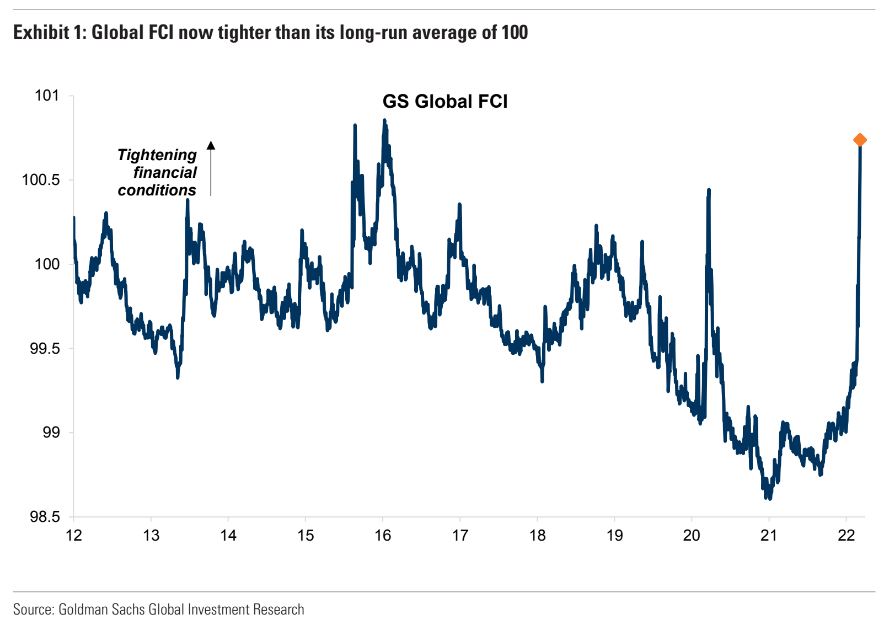

It may have to. As noted last week, global financial conditions are tightening at spectacular speed under pressure on all fronts from Ukraine sanctions, the Fed and q rising DXY:

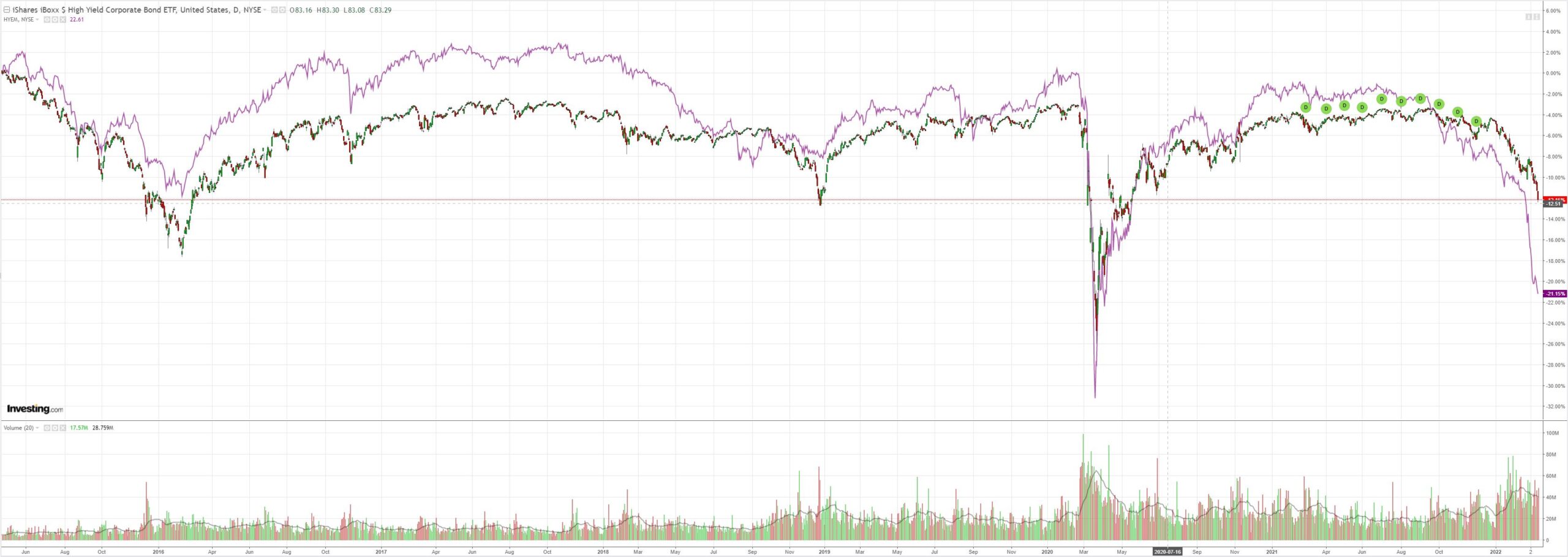

This is hammering peripheral global credit spreads and it’s working its way back to the centre as well::

Advertisement

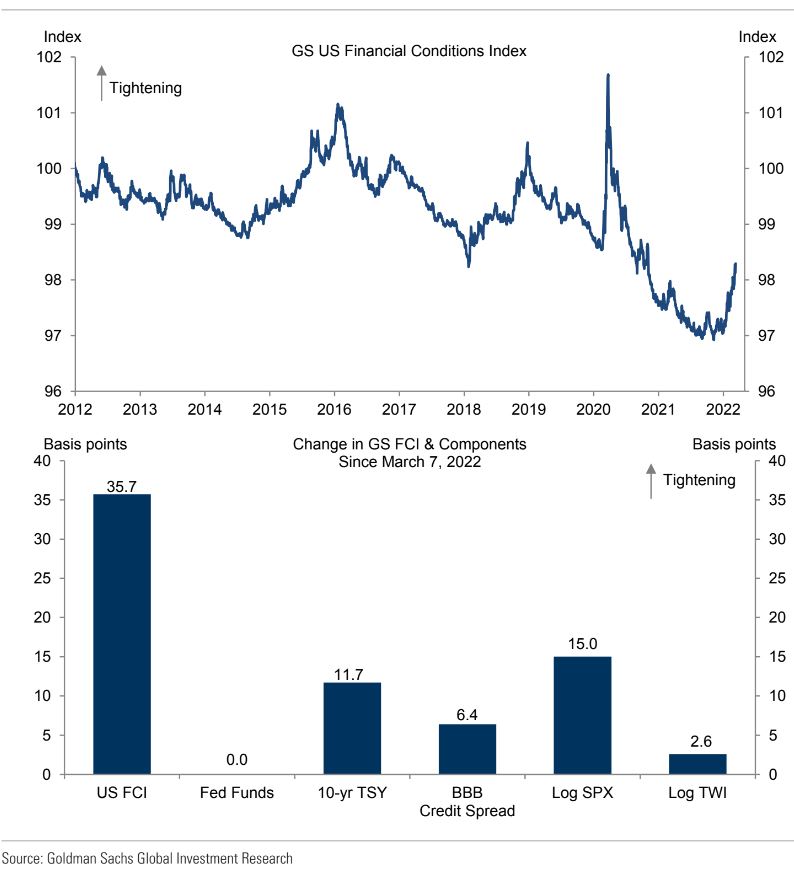

Yet this is all happening before the Fed has even hiked once while US inflation is raging and US financial conditions remain obscenely easy: