Here is the glass-half-full take on Commodity Boom 3.0 from Coolabah Capital:

There are, however, silver linings for Australia, which truly remains the “wonder down under”. As a net energy exporter, we are getting the benefit of huge increases in the value of our most important commodities: iron ore has surged from US$87/ton in November 2021 to over US$150/ton; our thermal coal prices have jumped from US$150/ton in January to US$370/ton; and LNG prices have doubled from a year ago.

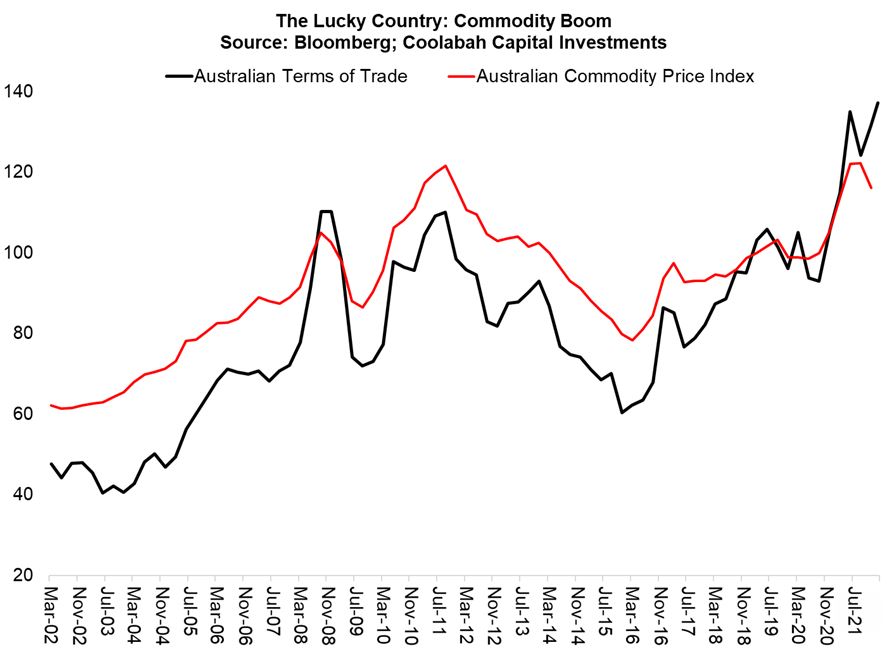

In fact, the Reserve Bank of Australia’s official index of commodity prices in trade-weighted terms has, as Terry McCrann recently pointed out, appreciated by an incredible 46 per cent since December 2019. It is now on par with the peak registered in the great commodity price boom a decade ago. This has meant that Australia’s terms of trade, representing the ratio of our export prices to import prices, is likewise at similar levels to its maximum point in the last cycle.

The commodity boom is providing an unexpected revenue boost for both State and Federal budgets with Western Australia, Queensland, and New South Wales, in particular, making out like bandits. On our seasonal adjustment, WA’s general government surplus increased from $1.7 billion in the third quarter to $2.3 billion in the fourth quarter of 2021. This means WA has achieved a $4 billion surplus in the first half of the financial year compared to the state’s forecasts of a $2.8 billion surplus for 2021-22 as a whole. And there are more revenue upgrades to come.

Another silver lining is evidence of global investor diversification out of Europe and into relative safe havens like Australia and the US. In recent months, the Japanese have poured billions into State government bonds, which pay the highest yen-hedged yields of any AAA or AA rated government bonds globally.

The next big event risk is where the Fed’s cash rate ends up. Investors currently believe the Fed’s terminal cash rate will be only 1.75 per cent. Our analysis implies it will move to 2.50 per cent as a minimum, which could precipitate another materially adverse repricing of risk assets. But that may be a story for late 2022 or early 2023.

So, why do I say it will make most Aussies poorer? Because today’s commodity boom comes at the tail end of a decade of the worst resources policymaking in Australian and world history bar none.

Surely, that’s a jest, you say. Nope.

Advertisement

The disaster began in 2010 with a mining coup that removed Kevin Rudd from power over the Resources Super Profits Tax (RSPT). This tax aimed to ensure a fair split for the owners of the commodities – the Australian people – by rendering higher taxes upon those that lease them – the miners – as prices rose.

The tax would today be pumping scores of billions of new tax revenue into budget coffers with iron ore at $150. Instead, it is all going to shareholders, most of them foreign.

Sadly, even for those Aussies that do own equities and miners, they are all striding backward as the global post-COVID tightening of stimulus crushes stock markets. Sure, the commodities boom is helping the ASX fall a little less but that’s not the same as getting richer!

Stocks prices and dividends are one of three main channels through which most Aussies get richer during commodities booms. Unfortunately, the other two paths are equally choked.

Advertisement

They are rising budget surpluses leading to tax cuts, and wage rises.

On the first, the post-COVID fiscal consolidation means new tax cuts are unlikely (though we can’t underestimate the desperation of one “Psycho” Morrison). It would be a bad idea to finance new structural tax cuts from a cyclical mining revenue boost.

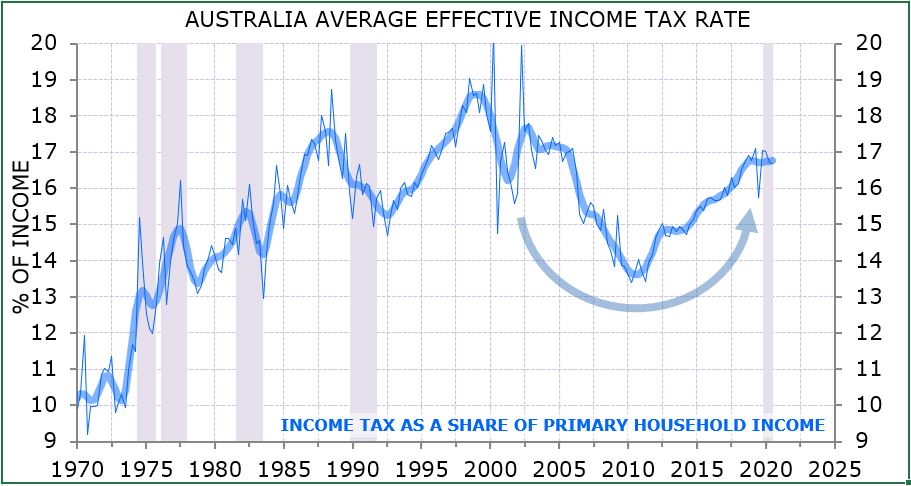

The best we can probably say is that more tax hikes via bracket creep may be held at bay a little by the current boom but the tax burden on households is already far higher than it was during previous commodity booms and trending upward:

Advertisement

Those tax breaks that are already scheduled are very poorly targeted at the rich and will bypass the vast majority of Aussies.

As for wages, despite the hoopla of various pundits, wages growth is unlikely to rise much into the future as mass immigration is explicitly restored to crush them.

Advertisement

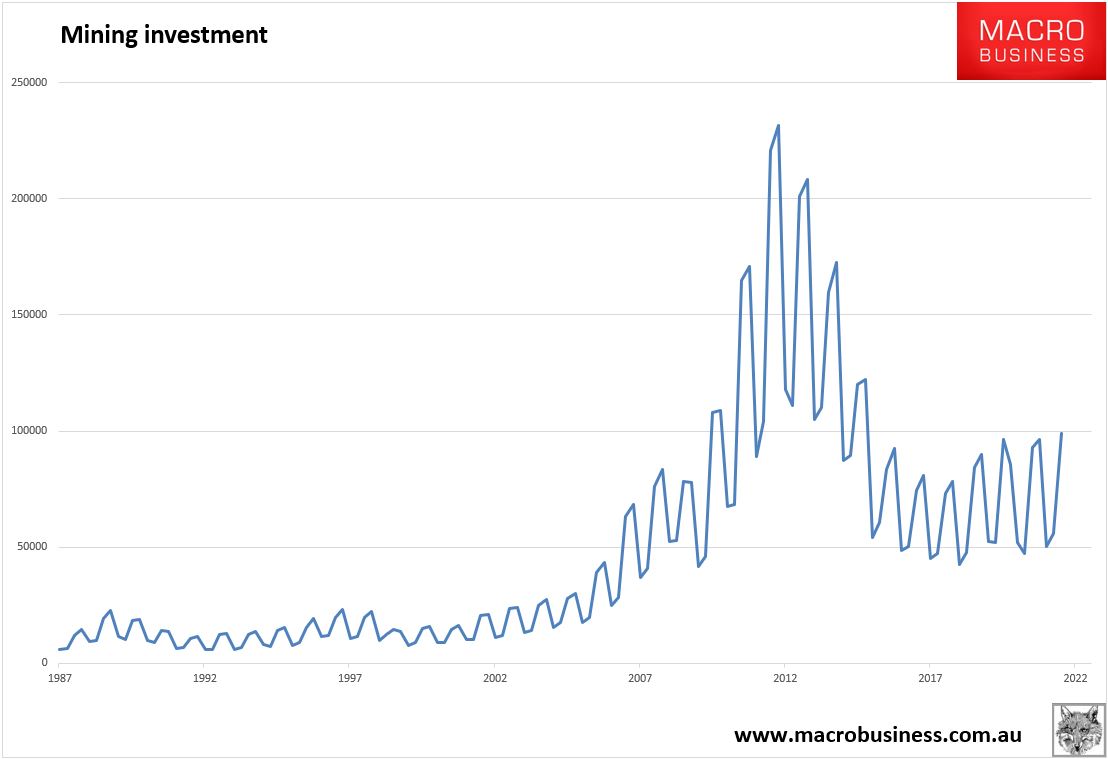

Moreover, compared to past commodity booms, this one is NOT triggering the investment needed to lift wages:

Why? Because, believe it or not, this commodity boom is despite all of our major products being in structural oversupply not because of it. Iron ore is glutted. Gas is glutted. Thermal coal is dying. Coking coal is plentiful.

Advertisement

All that has happened is that COVID has temporarily crimped supply in some regions and/or geopolitics has threatened supply in others. No miner is going to invest in such a febrile and temporary context.

So, wage rises are not going to share the bounty with ordinary Aussies this time because there are no new mines. Even as strong global inflation is going to eat away at their pricing power. Indeed, real wages are currently falling.

This brings me to where the last ten years of resources policy goes from bad to calamitous. In one sense, the booming terms of trade chart above is very misleading. For energy.

Advertisement

In the terms of trade, skyrocketing oil and gas prices more or less cancel each other out. That is, rising gas export revenues are offset by rising oil import costs.

But, when we figure out how these various effects are actually distributed through the economy the picture is much worse for Aussie households and small businesses, the vast majority of the population.

LNG exports benefit a very narrow set of equities which are, again, caught in wider stock market losses anyway. The rest of the gas exports are 90% foreign-owned.

Advertisement

Moreover, they collect no tax. Literally NO TAX. The LNG tax regime is so corrupted by interests that it has actually ceased to exist in any meaningful sense.

At current prices, LNG exports will deliver $60-80bn in revenue that will leave no next-to-no-mark on the country’s tax base.

And while it does so, the same price rises will lift gas and power bills for every household and business east of the WA border.

Advertisement

This perverse impact of a failed tax regime was long ago modeled by Victoria University such that the higher the LNG export price, the worse the impact on the local economy:

The outcomes for real GDP reflect the balance of two offsetting forces. The expansion in LNG exports at the high global price results in a terms-of-trade increase for the economy. This tends to reduce the real cost of capital, leading to increased capital and increased real GDP. We call this the quantity effect. It is shown in Figure 3 by the upper dashed line. By 2020, the quantity effect adds around 0.8 per cent to real GDP. The annual increment persists thereafter.

Offsetting this, though, is the increase in gas prices for domestic use. The increase gas price allows for larger than normal profit for the local gas producers, but it also raises the cost of production for gas-using industries. Many of these industries cannot pass on these increases, and so cut production. Thus for these industries the increase in cost of gas means reduced production, employment and capital utilisation, resulting in a loss of real GDP for the economy generally. In Figure 3, this adverse price effects is shown by the lower dashed line. By 2020, the price effect subtracts around 0.6 per cent from real GDP.

If we then add the cost of rising oil prices to households and non-mining businesses for this equation then the outcome is obvious. Most Aussies are materially worse off as oil and gas prices boom.

Advertisement

Of course, it did not need to be this way. Had any of the Coalition governments over the decade installed domestic gas reservation and a proper taxation regime then we would all be creaming it instead with an enormous tax revenue windfall measured, again, in the scores of billions per annum with no utility bill shock.

I don’t mean to suggest that the country in aggregate is not better off for this commodity boom. We all benefit when mining tax receipts boost government budget balances even if they aren’t recycled directly to us. Wages and equities will be stronger than otherwise. And I haven’t accounted for the agri-boom that will help regions.

But is the vast majority of Australians getting poorer more slowly than other nations a satisfactory outcome for the greatest commodity price boom in the history of the country?

Advertisement

Or is it the final indictment of a Coalition regime that is so corrupt that even global rivers of gold now make most Aussies worse off!?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.