The Conversation’s Peter Martin has published an interesting article explaining why the Reserve Bank of Australia (RBA) will be reluctant to lift interest rates, despite soaring inflation.

Martin’s key contention is that Australia’s inflationary pressures have been imported via soaring oil prices from the Russian-Ukraine war and supply-side bottlenecks impacting inputs like semiconductors. Accordingly, lifting interest rates to combat this imported inflation would be futile and could tip Australia into an unnecessary recession:

Buoyant demand (spending) is most certainly not the main thing pushing up prices now. The main things are beyond the Reserve Bank’s power to control.

Petrol prices have skyrocketed… Everything that is shipped and trucked using oil is set to cost more.

And trucks and cars themselves are climbing in price because of a global shortage of computer chips…

[Wage growth] has remained historically low at 2.3%, little more than it was before COVID…

It is best to think about most of what has happened as a series of isolated externally-driven price rises that have dented our standard of living.

Pushing up interest rates to dent living standards further won’t stop them.

…Asked on ABC’s 7.30 this week whether there was a role for higher interest rates in an oil crisis, a former Reserve Bank board member, Warwick McKibbon, said “the worst thing a central bank can do in a supply shock or an oil crisis is to target inflation, because by targeting inflation you push downward pressure on the real economy”.

He went on to say that if the bank did it without success and then kept doing it, it would bring on a recession. I am sure the bank doesn’t want to do that.

I agree 100% and have been running the same line of argument for months.

Interest rates are a blunt demand-management tool, which are only effective in taming domestically generated inflation. Since Australia’s inflation is import-driven, lifting rates to tame it would be futile.

That’s why I believe the RBA will only lift rates once wage growth rises above 3% (from 2.3% currently). This will be the best sign that a wage-price spiral could be taking hold and domestically generated inflation is rising.

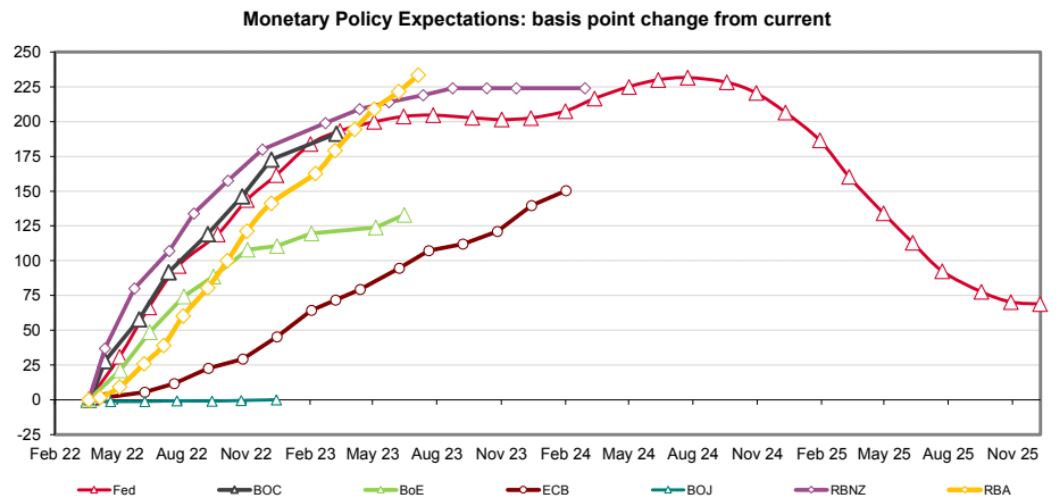

Markets are tipping 2.25% of RBA rate hikes by mid-2023

For these reason’s I am far less bullish on rate rises and believe the RBA won’t lift rates nearly as early, swiftly nor far as the 2.25% increases the market is predicting.