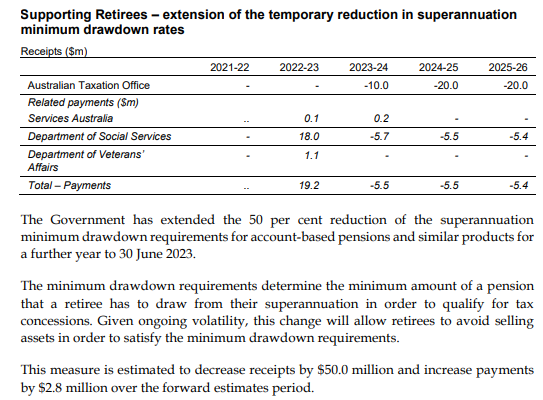

Tuesday’s federal budget extended its minimum pension drawdown requirement for a further 12 months, enabling affluent retirees to keep their superannuation balances without needing to sell their assets.

This policy was introduced in March 2020 as an emergency COVID measure when the Australian stock market was in freefall, reducing minimum drawdown rates by 50%.

The biggest beneficiaries of the extension are wealthy retirees, who use superannuation tax breaks to escape tax on funds they are accumulating to pass on to their children.

Advertisement

It provides next to no benefits to less well-off retirees who need to use money they have accumulated in superannuation to fund their retirement.

Before the temporary halving of drawdown requirements in March 2020, a retiree aged between 65-74 was required to withdraw at least 5% of their account balance each year.

The rationale for this requirement was that it limited the ability of wealthy retirees to use superannuation as a pure tax dodge. Funds accumulated in superannuation retirement accounts have a zero tax rate on earnings and are untaxed when withdrawn.

Advertisement

Given superannuation fund returns have boomed over prior 18 months, more than reversing the temporary losses in the March quarter of 2020, the rationale for extending the temporary reduction in the minimum pension drawdown rates is missing.

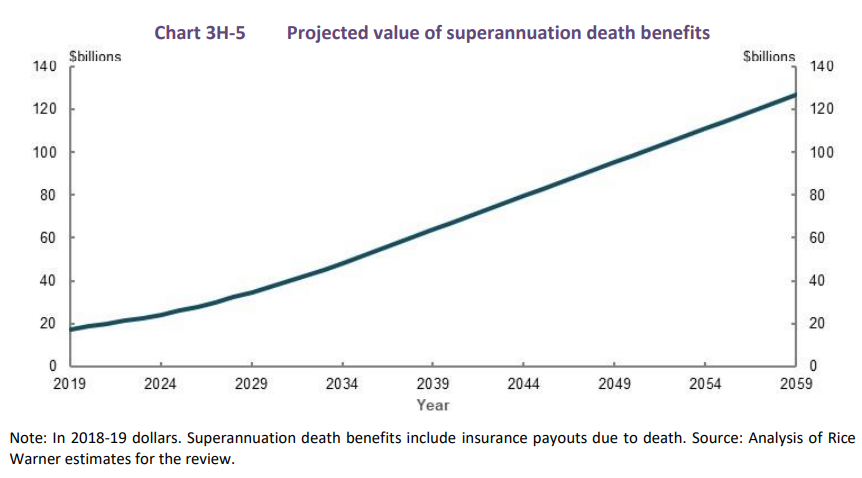

The Morrison Government’s decision to extend this measure will simply mean that wealthy retirees will accumulate larger superannuation nest eggs to pass onto their heirs via tax free inheritances. This policy contradicts the recommendations from Treasury’s Retirement Income Review, which urged retirees to spend their nest eggs:

Inheritances are significant, representing the transfer of wealth from one generation to another. They are not distributed equally and increase inequity within the generation that receives the bequests. Most people die with the majority of wealth they had when they retired. If this does not change, as the superannuation system matures, superannuation balances will be larger when people die, as will inheritances. Superannuation is intended to fund living standards of retirees, not to accumulate wealth to pass to future generations…

For example, assuming no change in how retirees draw down their superannuation balances, superannuation death benefits are projected to increase from around $17 billion in 2019 to just under $130 billion in 2059 (Chart 3H-5)…

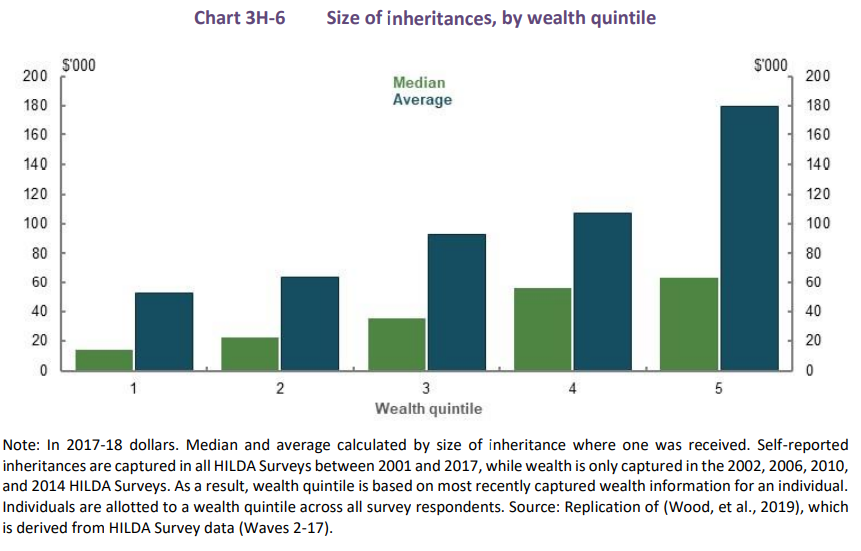

Although inheritances can help people to prepare for retirement, they are distributed unequally, with wealthier people tending to receive larger inheritances than those with lower wealth (Chart 3H6). Inheritances therefore increase intragenerational inequity…

Advertisement

The above is more confirmation that superannuation is really a tax minimisation and inheritance scheme for the rich rather than a genuine retirement system.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.