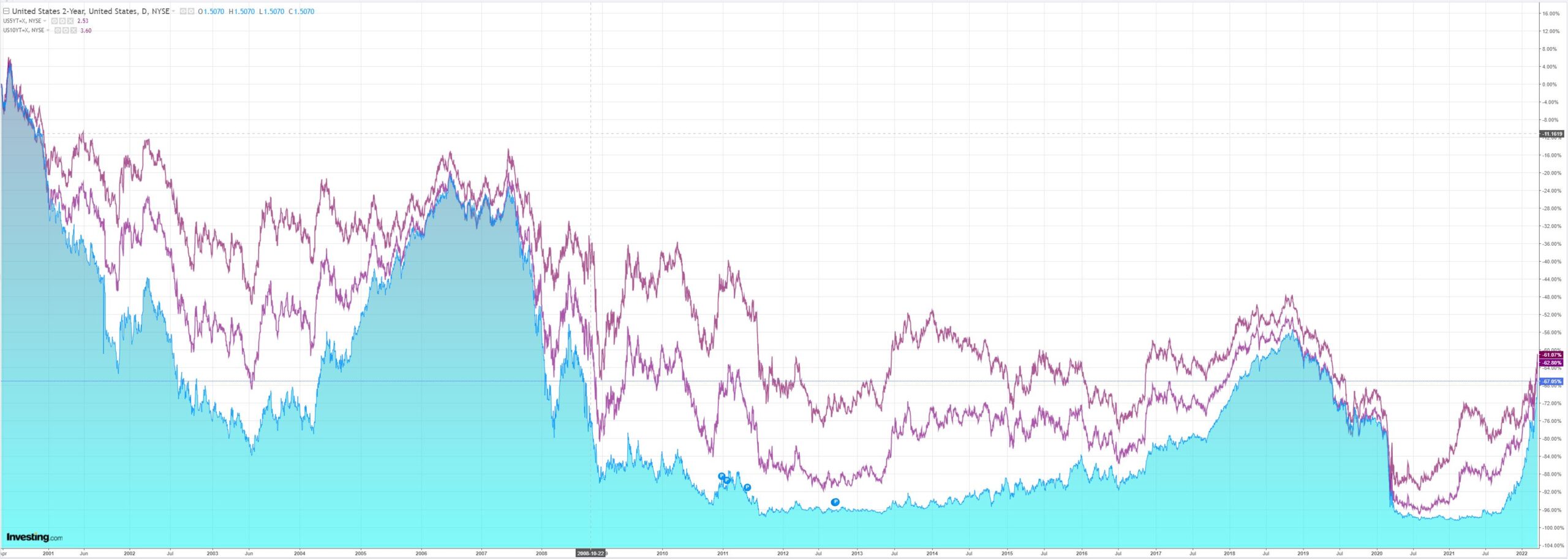

There are some perverse things happening in bond yields. Yields are rising in both the US and Australia:

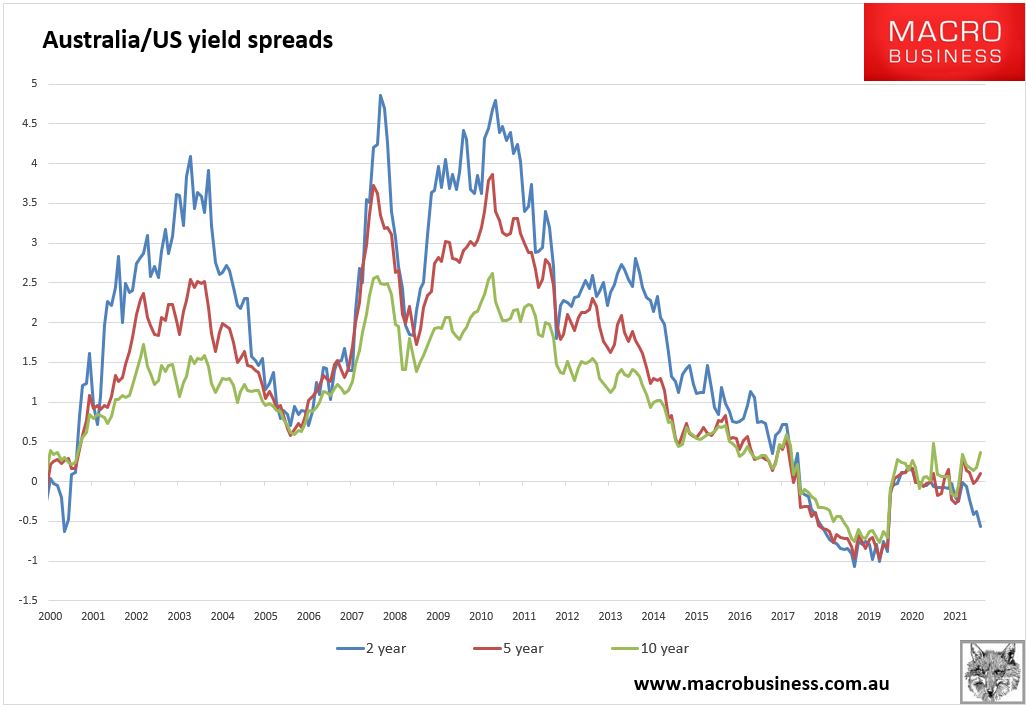

But is in the comparative shapes of the curve where we find whackness. At the short end of the curve, Aussie yields are inverted to the US as the RBA remains dovish. It has not been this way for two decades. Yet the long end is going the other way:

Advertisement

Markets clearly see Australia compressing an inflation spring that will uncoil in due course.