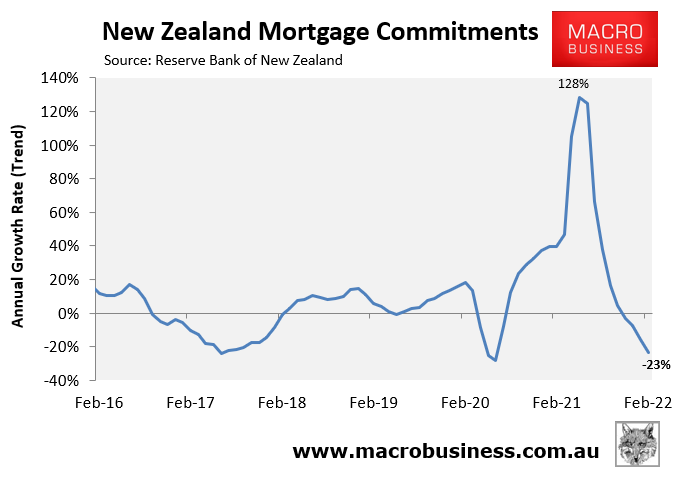

Data released on Friday by the Reserve Bank of New Zealand (RBNZ) revealed that mortgage growth has collapsed across New Zealand.

After rising a whopping 128% in the year to May 2021, annual new mortgage commitments fell by 23% in the year to February 2022 in trend terms:

Mortgage commitments move from boom to bust.

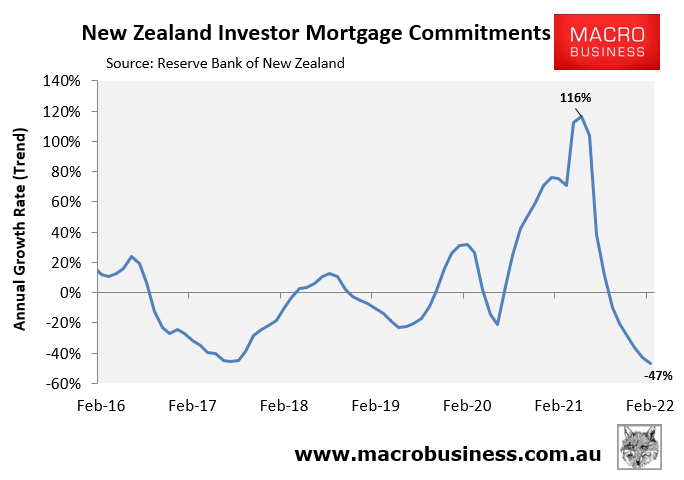

This decline was driven by a sharp turnaround in investor mortgage commitments, which swung from growing by 116% in the year to May 2021 to plunging by 47% in the year to February 2022:

New Zealand property investors rush for the exits.

Given the overwhelming majority of New Zealanders purchase homes with a mortgage, the slump in finance commitments is a bearish indicator for house prices.

Independent economist Cameron Bagrie says the decline in mortgage commitments was inevitable after the insane boom that took place in 2021.

Bagrie claims a “ridiculous” amount of mortgage lending took place in the second part of 2020 and the first eight months of last year. This meant the “monstrous” level of home lending taking place was never sustainable.

“There is a lot more going on. There are loan-to-value ratios, banks tightening up on risk capacity, some banks imposing debt-to-income ratios, tighter servicing criteria, and also rising mortgage rates”, Bagrie said.

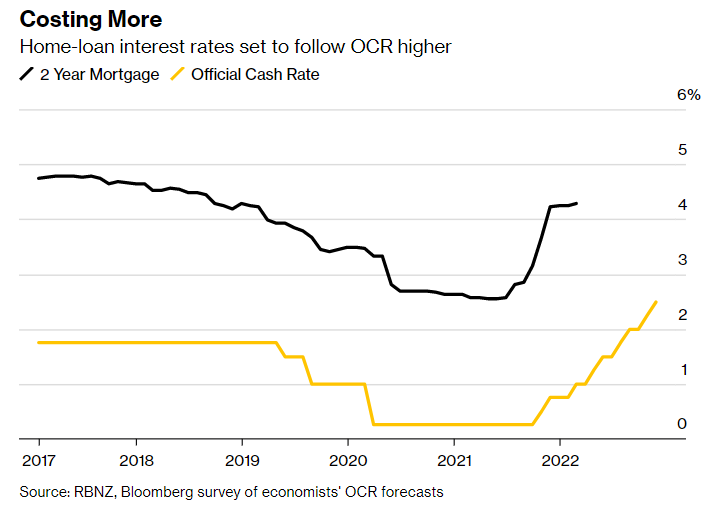

Meanwhile, New Zealand economists are warning that rising mortgage rates will further dampen mortgage demand and house prices.

A Bloomberg survey of economists are tipping that the interest rate on a two-year fixed mortgage will rise to 5.5% by the end of 2022, with one-year fixed rate mortgages climbing above 5%.

New Zealand mortgage rates are set to soar.

The majority of New Zealand mortgages are on fixed terms rather than floating rates, and around 80% of current fixed rate mortgages – many originated at rates below 3% – are due to expire over the next two years, according to Bloomberg.

Economists are also tipping the RBNZ will raise the official cash rate from its current level of 1.0% to 2.5% by November, which will also lift floating mortgage rates.

The prospect of sharply rising mortgage rates leaves New Zealand households and the economy exposed.

As noted by Sharon Zollner, chief New Zealand economist at ANZ Bank in Auckland, “the New Zealand economy has been famously described as the housing market with an economy attached. [Rising interest rates] has massive implications for how households behave”. As such, “there’s a wealth impact on consumers’ willingness to spend”.

Two of New Zealand’s major banks – ANZ and BNZ – are now forecasting a 10% decline in house prices in 2022.

But if interest rates rise another 2.5% by the end of 2023, as forecast by Westpac and the financial markets, then the expected house price correction could easily turn into a more severe crash as Kiwis are placed under severe mortgage stress.