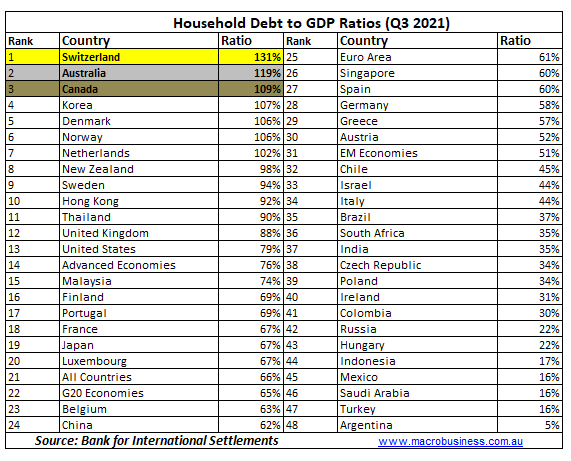

The Bank for International Settlements (BIS) has released its global household debt statistics for the September quarter of 2021. This data shows that Australia still has the second highest stock of household debt in the world when measured against the size of its economy, as measured by Gross Domestic Product (GDP).

As shown in the table below, Australia’s household debt-to-GDP ratio was 119% in Q3 2021, second only to Switzerland (131%):

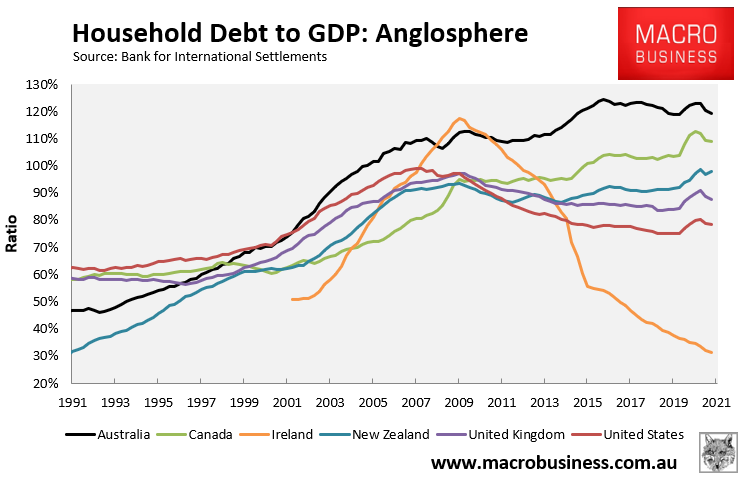

The next chart plots the time series across the Anglosphere, with Australia’s household debt load well ahead of Canada (109%), New Zealand (98%), the United Kingdom (88%), the United States (79%), and Ireland (31%):

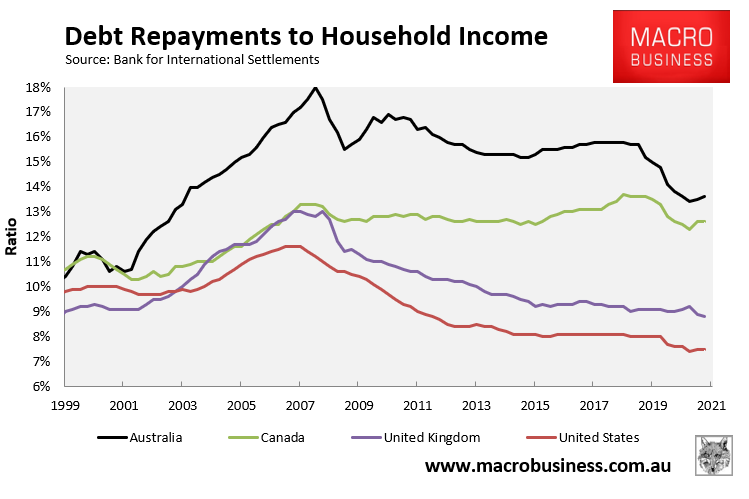

However, because mortgage rates fell so heavily over the pandemic, Australian household’s debt repayment burden – i.e. principal and interest repayments as a ratio of disposable income – has also fallen markedly; albeit remains well above the Anglosphere nations surveyed by the BIS:

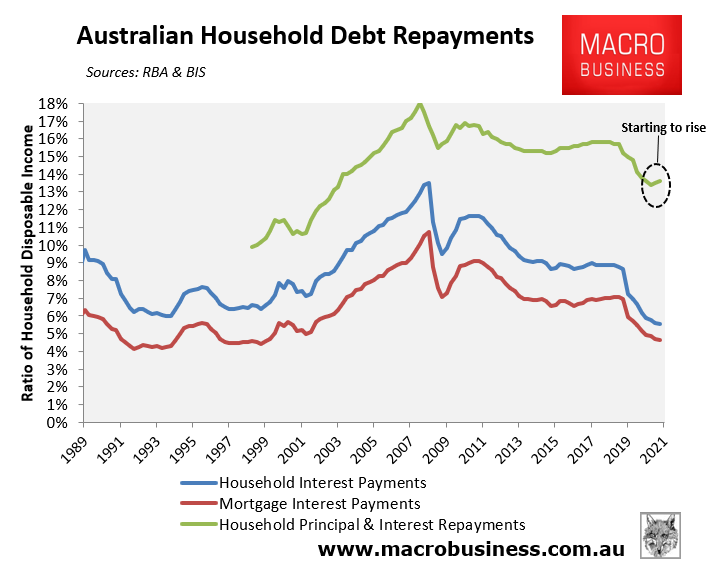

The situation is also beginning to change. The next chart combines the BIS series with the RBA’s household/mortgage interest payment data:

The ratio of household interest repayments to income fell to 5.5% in September 2021, less than half the peak of 13.3% in December 2008:

In a similar vein, the ratio of mortgage debt interest payments to income fell to 4.6% in September 2021, less than half the peak of 10.6% in December 2008.

However, the green line in the above chart is interesting. It shows total household debt repayments (i.e. both principal and interest), which rose over the June and September quarters on the back of the sharp appreciation of house prices:

Basically, the rise in mortgage principal repayments due to higher house prices exceeded the fall in mortgage interest repayments due to declining rates.

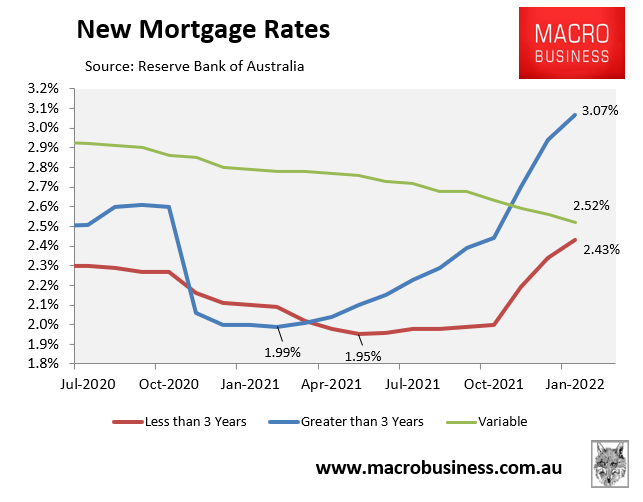

The implication going forward should be obvious. Fixed rate mortgages have already risen quite sharply since the September quarter (see next chart) and variable mortgage rates are tipped to rise this year as the RBA lifts the cash rate.

The upshot is that the share of household income going towards debt repayments are about to rise quite sharply, which will sap disposable income, restrict growth, and put strong downward pressure on housing prices.

I’ll upload a Macro Breakdown video later today explaining these dynamics in more detail.