Rising interest rates will crash Australian house prices

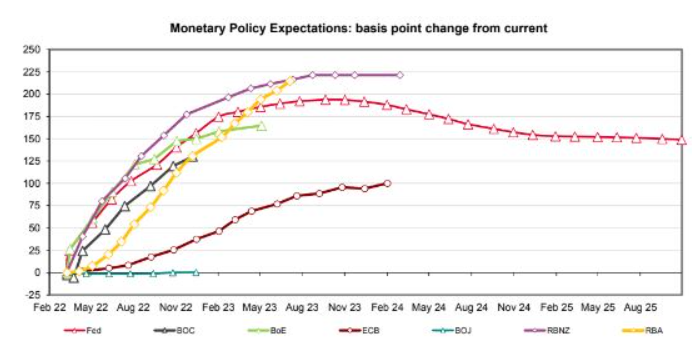

On Friday, MB’s David Llewellyn-Smith published the latest market forecasts on monetary tightening, which tipped the Reserve Bank of Australia (RBA) would lift the cash rate by around 2.15% by June 2023 (yellow line below):

Financial markets tip the RBA will lift the cash rate by 2.15% by mid-2023.

Such tightening, which is predicted to begin in May this year, would be the equivalent of nine interest rate hikes.

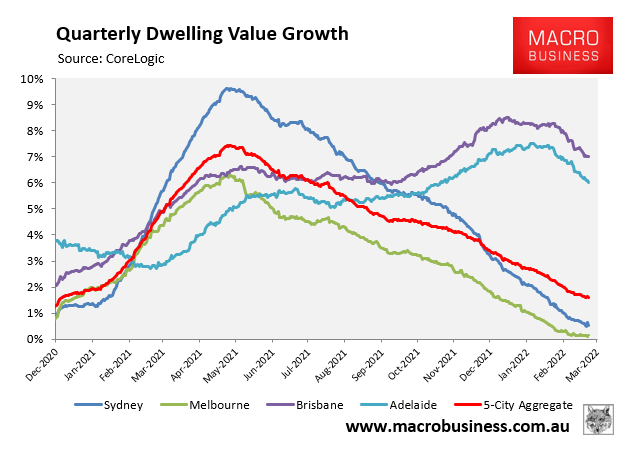

It would also arrive as Australia’s property market is already beginning to stall. As illustrated in the next chart, Australia’s largest property markets of Sydney and Melbourne are slowing fast. They have recorded only 0.4% and 0.25% growth so far in 2022, which has pushed national capital city growth to only 1.25%, according to CoreLogic:

Sydney and Melbourne dwelling values are already stalling.

It is fair to say that if the RBA cash rate was to rise in accordance with the Market’s forecasts, then Australian housing values would crash.

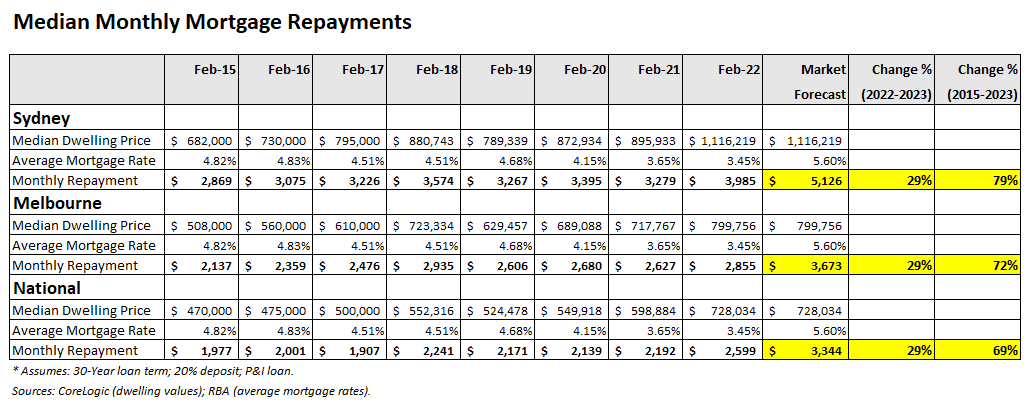

To illustrate why, consider the next table showing the average monthly repayment on the median priced dwelling across Sydney, Melbourne and nationally:

The above repayments are calculated using the median dwelling value (via CoreLogic), assuming a 30-year principle and interest mortgage, a 20% deposit, at the average discount variable mortgage rate (as provided by the RBA).

The highlighted section on the right shows that if the average discount variable mortgage rate was to rise by 2.15%, as predicted by the market, average monthly mortgage repayments would rise by 29% from their February 2022 level and by 69% nationally from their February 2015 level.

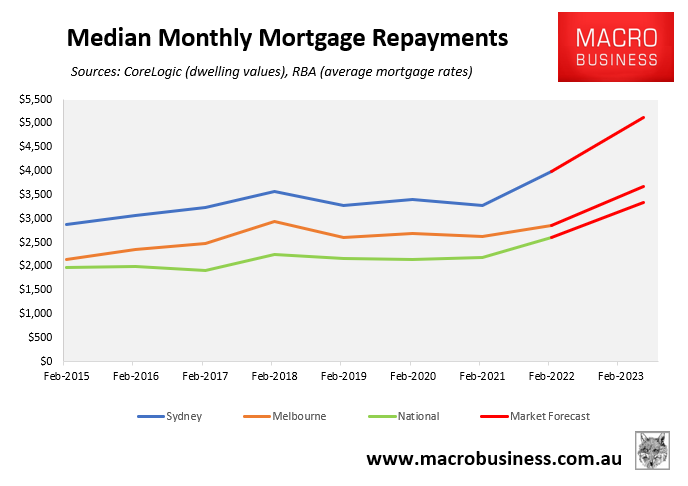

The next chart plots the same data as a time series (Market’s forecast in red):

Monthly mortgage repayments would rise 29% if the market’s interest rate projections come true.

The impact would be even more severe for the circa $500 billion worth of fixed rate mortgages due to expire over the next two years, most of which were originated at rates of under 2.5%. Those borrowers are facing more than a doubling of mortgage rates when it comes time to refinance.

Such a dramatic increase in monthly mortgage repayments would very likely crash Australian house prices, especially across the most expensive and unaffordable markets like Sydney and Melbourne.

Because the impacts would be so severe, the likelihood of the RBA raising the cash rate by 2.15% is slim at best. Nor are the RBA likely to begin tightening from May 2022.

A more plausible scenario is for the RBA to begin lifting rates late this year once wage growth picks up above 3% and then only incrementally. Since Australians are so indebted and are so sensitive to interest rate rises, a few 0.25% increases in the cash rate would be enough to temper demand. These smaller rises in the cash rate would also ensure that house prices experience a ‘correction’ (circa 10% fall) rather than a crash.

There is also a decent chance that the Russian-Ukraine War tips the global economy into recession, in which case the RBA might respond with further monetary stimulus rather than tightening.

Whatever the case, the market’s interest rate projections are far too heroic and detached from reality.