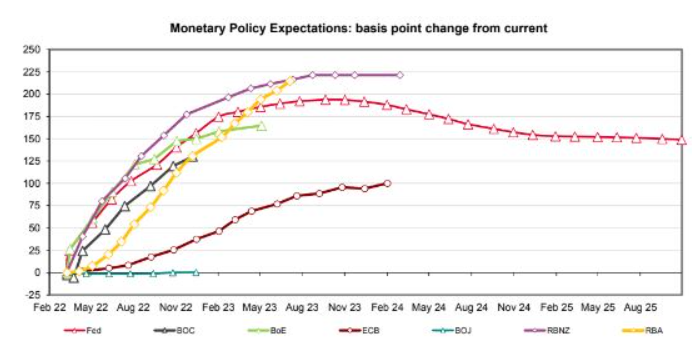

As we know, financial markets are tipping the Reserve Bank of Australia (RBA) will lift the official cash rate by 2.15% by June 2023 – the equivalent of nine rate hikes (yellow line below):

Financial markets tip the RBA will lift the cash rate by 2.15% by mid-2023.

On Tuesday, the RBA released its Minutes of the Monetary Policy Meeting of the Reserve Bank Board, which again pushed back hard against the notion that rate rises are imminent [my emphasis]:

Turning to the decision for the cash rate, members remained committed to maintaining highly supportive monetary conditions to achieve the objectives of a return to full employment in Australia and inflation consistent with the target. As agreed at previous meetings, the Board will not increase the cash rate until actual inflation is sustainably within the 2 to 3 per cent target band. While inflation had picked up, members agreed it was too early to conclude that it was sustainably within the target band. There were uncertainties about how persistent the pick-up in inflation would be given recent developments in global energy markets and ongoing supply-side problems. Wages growth also remained modest and it was likely to be some time before aggregate wages growth would be at a rate consistent with inflation being sustainably at target. The Board is prepared to be patient as it monitors how the various factors affecting inflation in Australia evolve.

Specifically on wages, the RBA noted that it has only recovered to sluggish pre-COVID levels:

Wages growth had picked up, but only to around its pre-pandemic rate…

Across industries and states, wages growth outcomes had been unusually tightly clustered in the low-to-mid 2 per cent range. While the share of jobs recording wage increases of 2–3 per cent had recently returned to around pre-pandemic levels, the share of jobs with wage increases above 3 per cent had been little changed in recent quarters. The share of jobs that experienced a wage change was higher than usual for the December quarter in both the public and private sectors, but this largely reflected catch-up following pandemic-related delays to regular pay increases. Information from the Bank’s business liaison program had suggested that the distribution of firms’ wages growth expectations over the coming year remained similar to the pre-pandemic pattern. Surveys of unions’ expectations had also been consistent with wages growth of around 2½–3 per cent over the year ahead.

Thus, the RBA has yet to change its tune: it is in no rush to lift rates and will keep them on hold until annual wage growth rises above 3% (from 2.3% currently).

My prediction remains that the first rate rise won’t arrive until late this year. The tightening cycle will also be far shallower – i.e. less than 1% – because Australian households are so indebted and sensitive to small rate rises.

I discuss these issues in my latest Macro Breakdown, entitled “Why financial markets are wrong on interest rates”: