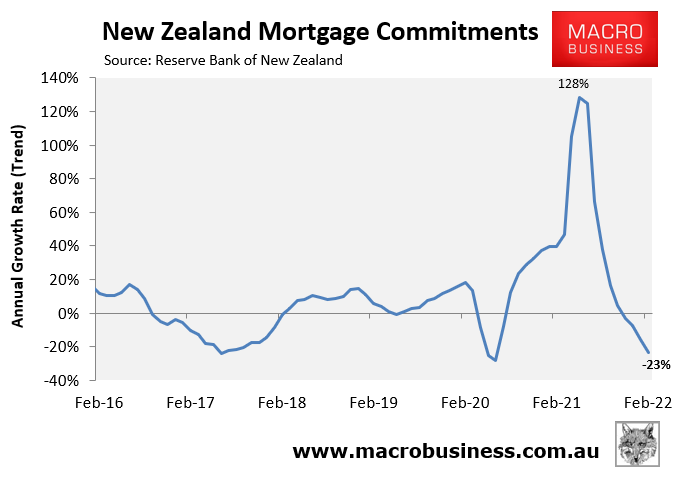

After experiencing one of the world’s biggest house price booms in 2021, the warning signs are piling up for New Zealand’s housing market.

First, after registering annual mortgage growth of 128% in May last year, the value of new mortgage commitments contracted by 23% in the year to February:

After the epic mortgage boom comes the bust.

Given almost every Kiwi purchases a home with a mortgage, this slump in demand is a negative signal for New Zealand house prices.

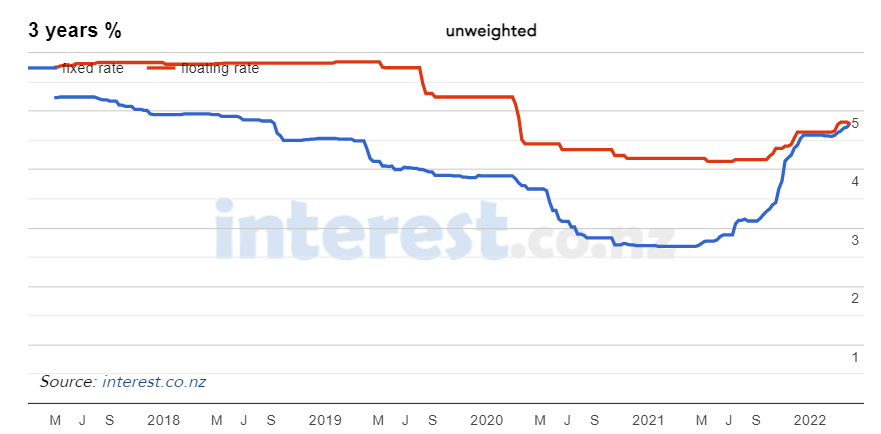

A key reason for the slump in mortgage demand is because mortgage rates are rising. As shown in the next chart from Interest.co.nz, floating mortgage rates have lifted by around 0.7% from last year’s low, whereas 3-year fixed rates have climbed 2.1% from their 2021 low:

Similar rises have been experienced across the other fixed rate terms.

The majority of New Zealand borrowers are on fixed rate mortgages. Accordingly, they already face a painful increase in mortgage repayments once their fixed terms expire.

To add further insult to injury, economists have projected that the Reserve Bank of New Zealand (RBNZ) will lift the official cash rate (OCR) from its current level of 1.0% to 2.5% by November this year, with Westpac and the financial markets also tipping the OCR to rise a further 1% by the end of 2023.

Therefore, New Zealand mortgage rates are certain to ratchet higher, which will further dent household finances, mortgage demand and house prices.

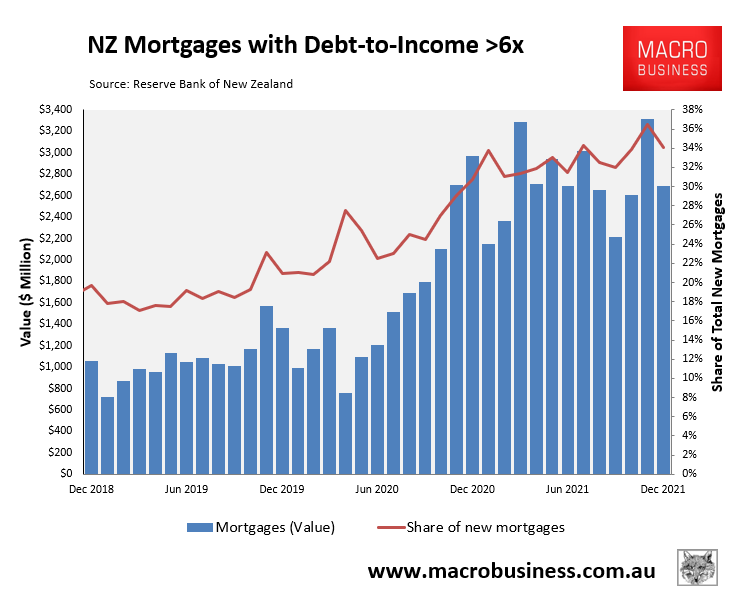

The prospect of soaring mortgage rates should be especially disconcerting for the one-third of mortgage borrowers in 2021 that originated their loans at a debt-to-income ratio above six times:

Recent Kiwi mortgage borrowers are very highly leveraged

These recent borrowers will be especially sensitive to rate rises.

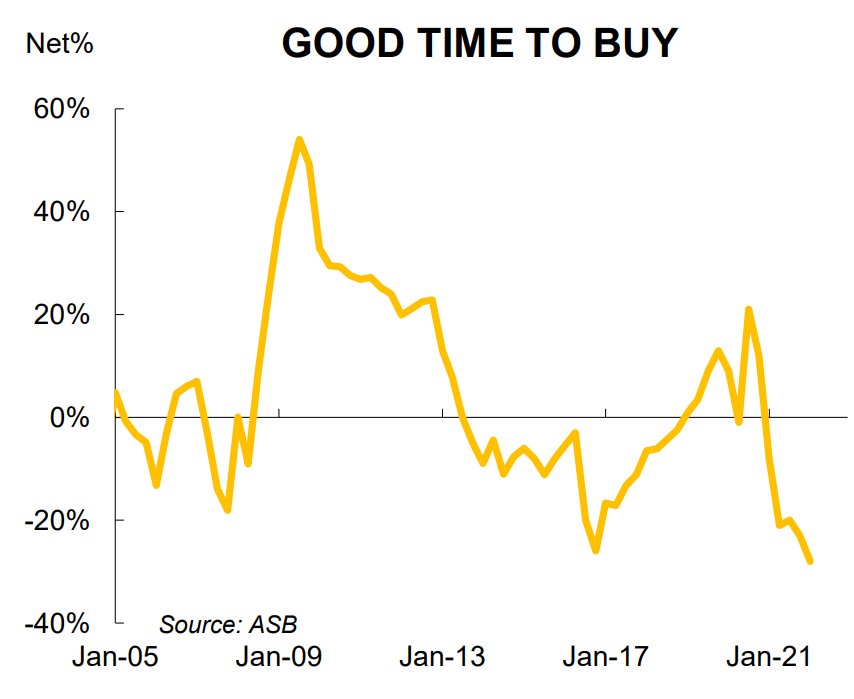

Next, Kiwi home buyer sentiment has collapsed with ASB’s “good time to buy a house” index plunging to a 26-year (record) low:

Kiwi buyers are very pessimistic on property.

ASB’s commentary is about as bearish as it can get:

When asked whether it is currently a good time to buy a house, our survey respondents have never been more definitive. A net 28% think it is a bad time to buy (7% think it’s a good time, 35% a bad time), the most negative reading for buyer sentiment since our records began 26 years ago.

And who could blame them? The housing boom has lifted prices to extremely stretched levels, mortgage rates are rising, and the weight of expert opinion is now warning of outright falls for this year.

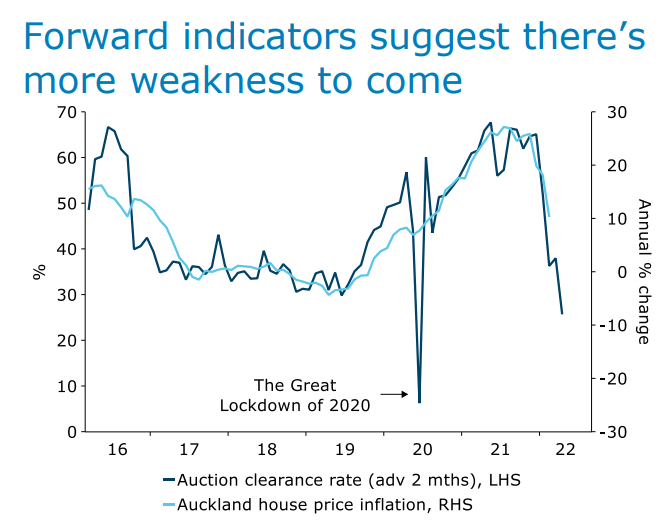

Next, New Zealand auction clearance rates have tanked, which is typically a bearish indicator for property prices (chart from ANZ):

Crashing auction clearance rates signal falling New Zealand house prices.

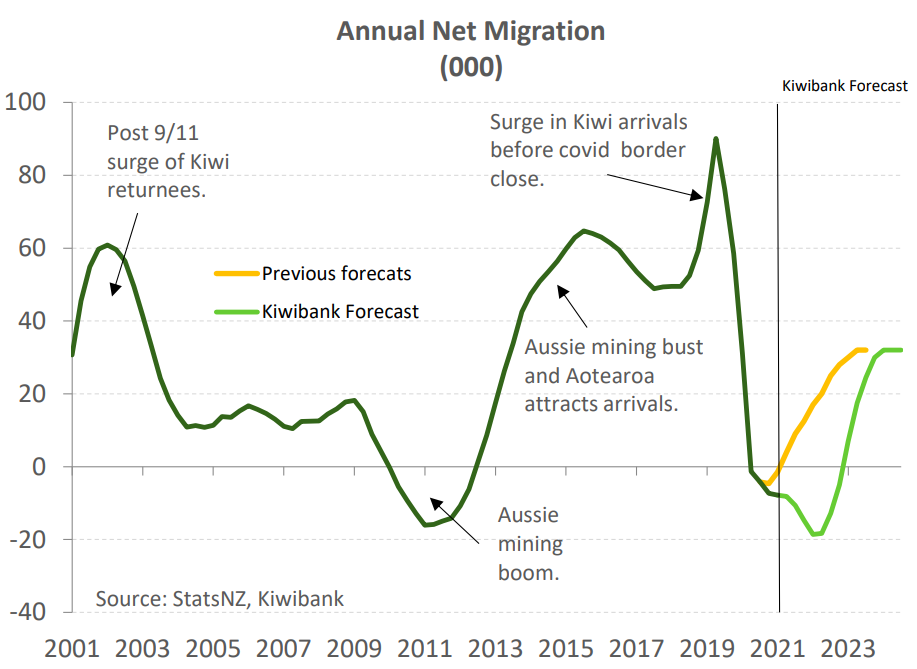

Next, Kiwibank tips that New Zealand immigration will go further negative over the coming year, which will further depress housing demand (other things equal):

Annual immigration to fall deeper into the red.

Finally, New Zealand’s Parliament this week passed legislation removing the ability of property investors to claim mortgage interest as a tax deductible expense on existing residential properties. Accordingly, interest will no longer be deductible for residential property acquired on or after 27 March 2021, with earlier investors’ ability to deduct interest to be phased out by 31 March 2025.

Logically, this rule change should dampen future investor demand as well as prompt a significant number of pre-existing investors sell their properties – either of which would put downward pressure on house prices.

The incentives for investors to sell will also increase in line with interest rate rises, since investors will be less able to share the rising mortgage costs with the taxman.

When weighed up together, the various indicators are pointing to a sizeable New Zealand house price correction, which could turn into a crash if the RBNZ hikes rates too far.