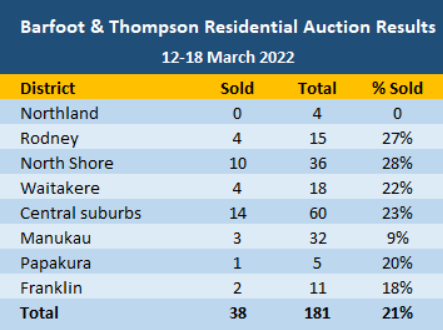

Last week saw only 21% of homes taken to auction across New Zealand sell, with the rest being passed in:

Poor auction clearances across New Zealand

The poor results have prompted prominent New Zealand property investor, Andy Thackwray, to declare the nation’s housing market is “about to tank”:

Thackwray doesn’t mince his words – he says the market is about to tank, and auctions have had their day.

“Selling by auction is a good thing to do if you’re in a price range where you’re going to get a lot of interest, and there’s a lot of people in a position to be able to buy,” he says.

But with the market currently retracting, and a “perfect storm” brewing of rising interest rates, tighter lending, and rising inflation, Thackwray says that’s not the reality most sellers are facing.

He sold two of his properties last year after becoming convinced the market would fall, and says prices could tumble 10 per cent, and properties in the first home buyer market and those earmarked for development could fall 20 per cent.

All signs are flashing red for New Zealand’s housing market.

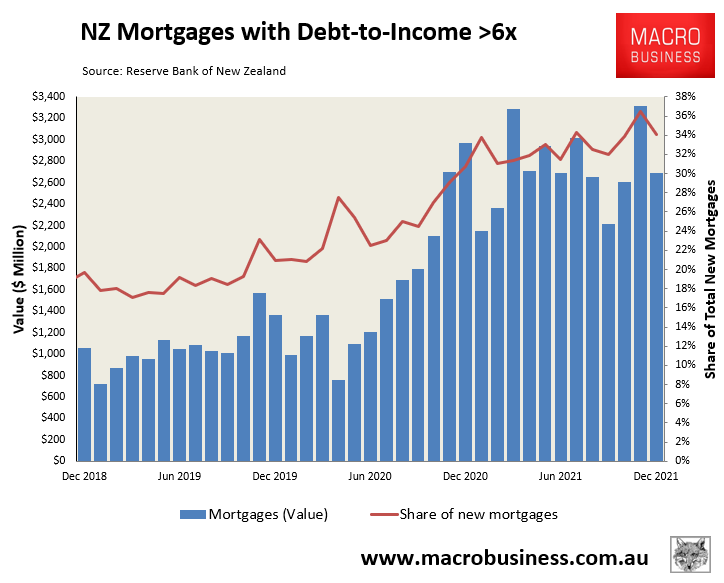

Recent New Zealand home buyers are highly leveraged, with one-third of mortgages taken out in 2021 (valued at $32.6 billion) originated at debt-to-income ratios above 6 times:

Recent New Zealand mortgage borrowers are highly leveraged

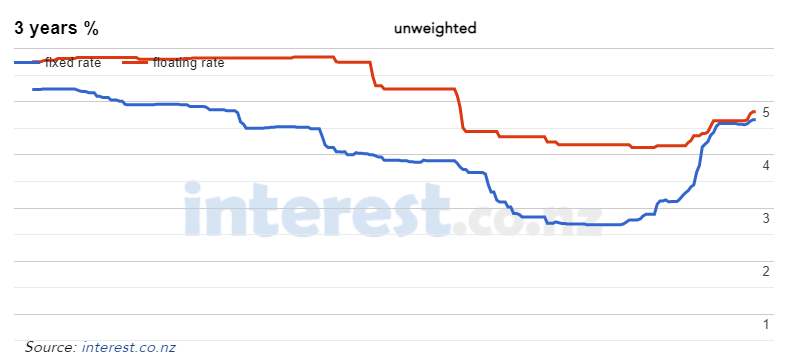

This has made New Zealand mortgage holders especially sensitive to rising interest rates, which have already increased sharply following successive rate hikes from the Reserve Bank of New Zealand (RBNZ):

New Zealand mortgage rates are rising

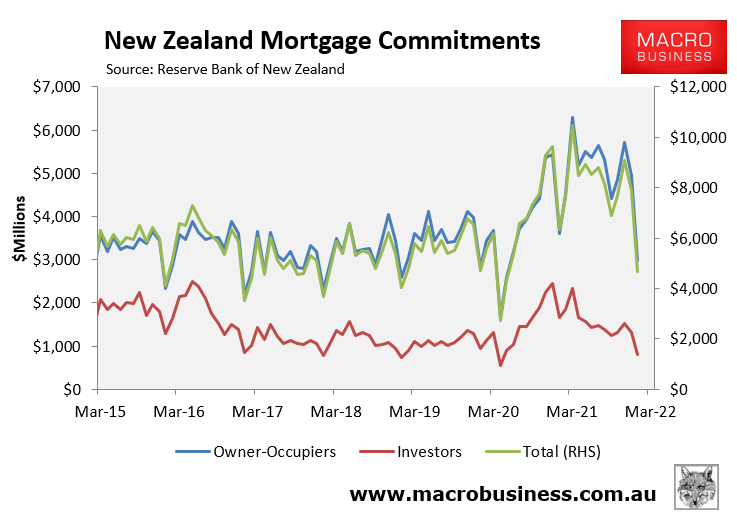

Mortgage demand has tanked hard in New Zealand, falling 21% in the year to January 2022, led by a 51% collapse in investor mortgage commitments:

New Zealand mortgage commitments have slumped

Part of the sharp fall in investor demand has been driven by the Ardern Government’s recent decision to ban interest rate deductibility on investor mortgages. This decision has meant that the cost of any interest rate rises are borne solely by investors, rather than being shared with the taxman.

Buyer confidence has also collapsed in New Zealand. The ASB housing confidence survey collapsed to a 26-year low over the three months to January, with REINZ CEO Jen Baird declaring “there is now a fear of overpaying among buyers”, meaning vendors must “adjust their expectations to meet the market”.

New Zealand’s economists are tipping the RBNZ will hike the official cash rate from its current level of 1.0% to between 2.75% (ASB’s forecast) and 3.5% (Westpac’s forecast).

The nation’s army of leveraged borrowers better hope the bank economists’ rate predictions are wrong. Because another 1.75% to 2.5% lift in mortgage rates could very easily tip the market over the edge and crash house prices.