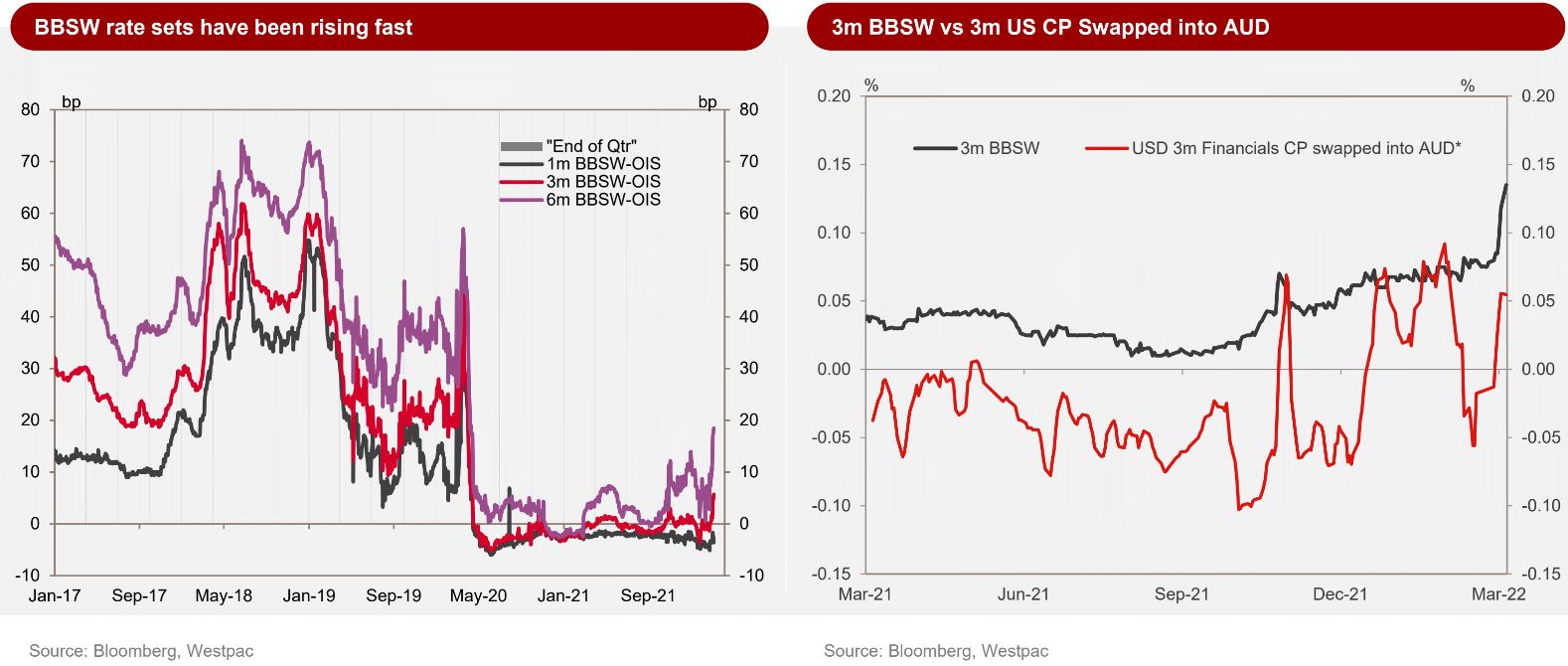

Fears around funding have started to impact rate sets pushing BBSW higher despite little reason for a sustained AUD funding squeeze. BBSW rate sets have been rising fast 3m BBSW vs 3m US CP Swapped into AUDBBSW rate sets and BBSW-OIS spreads (left chart) have been widening rapidly, with 3m BBSW higher by 5.5bps and 6m BBSW up by 15bps over the past week and the 3m-6mBBSW spread is as wide as it has been since 2017. So what does this mean? Given the amount of liquidity in the system as a result of TFF and QE policies, we do not see this as an AUD funding squeeze. There is plenty of short term cash in the system and banks do not need to significantly increase their short paper issuance in AUD. Indeed, some of last week’s rate sets were made on very little or even no volume. Rather this reflects the global situation and fears and volatility that arise from the geo-political crisis. During these episodes there is a natural demand for USDs as market participants try to protect their near term funding needs. Indeed, while US CP spreads have been rising prior to the war beginning, ahead of the Fed’s hike cycle, there is now a sense that some European companies are scrambling for USDs. The chart at right indicates the relationship between these CP yields and BBSW. There might be some element of “bring forward” of expected BBSW-OIS which has been on the radar given that the RBA has stopped growing its balance sheet, however it seems too early for that to be a major factor. So we believe that the recent moves will eventually settle lower, albeit given that whether or not BBSWrises or falls medium term is a one-way bet, perhaps the average BBSW rates ets over the next few weeks will remain higher than those that we have seen in recent months.

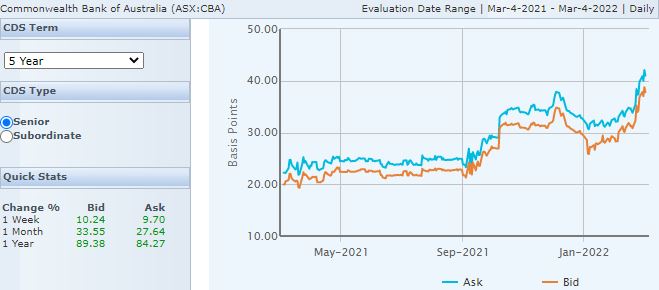

Longer duration wholesale funding spreads are widening fast as well though at 40bps they are still relatively narrow:

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.