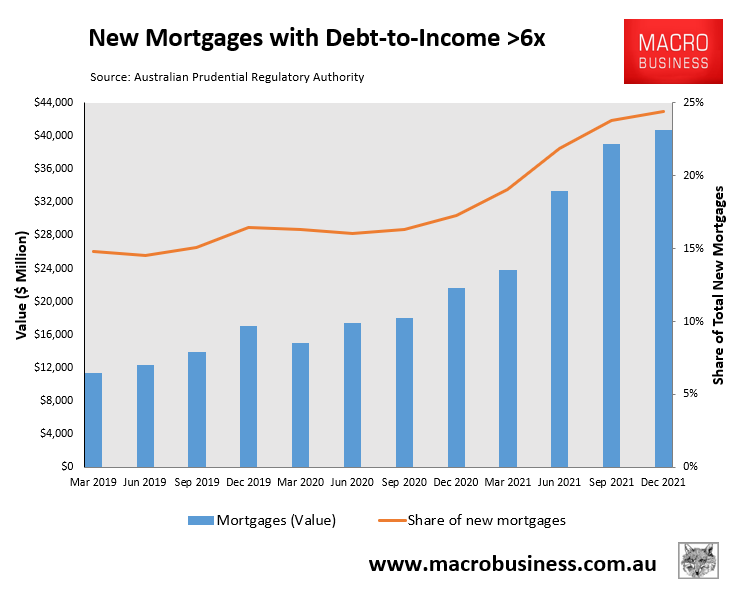

The latest mortgage exposure data from the Australian Prudential Regulatory Authority (APRA) showed that nearly one-quarter of mortgage borrowers in the December 2021 quarter originated a mortgage at a debt-to-income (DTI) ratio of six or above. This was up from around 15% of mortgage borrowers pre-pandemic:

High debt-to-income mortgage lending has surged in Australia

In fact, $264 billion worth of mortgages have been originated across Australia with a DTI ratio of six or above since March 2019, suggesting there is a large pool of recent buyers that are extremely sensitive to interest rate rises.

New research from social housing advocacy group Everybody’s Home, Digital Finance Analytics and the University of New South Wales City Futures Research Centre, based on a survey of 52,000 Australian households, showed that a huge number of homeowners are already struggling to make ends meet, with many highly vulnerable to an interest rate rise of just 1%:

More than 135,000 Sydney households and 88,000 in Melbourne will slide into mortgage stress if interest rates increase by just 1 per cent. And it’s not just those on modest incomes either…

Financial stress was defined as having less than 5 per cent of income left over after expenses.

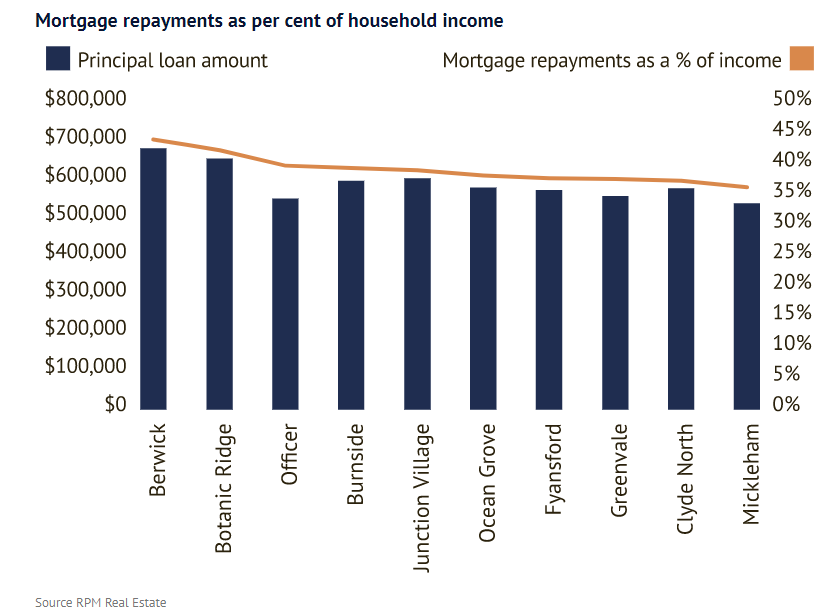

This follows separate research from property advisory group RPM, which showed that many families living in dozens of suburbs across Melbourne’s urban fringe are already experiencing acute mortgage stress:

Outer suburban suburbs are experiencing mortgage stress.

Similar results are presumably being experienced across Sydney, particularly across the city’s west.

To make matters worse, these outer suburban areas are more likely to be car-dependent, making them particularly sensitive to the sharp spike in petrol prices, which will further drain household disposable income.

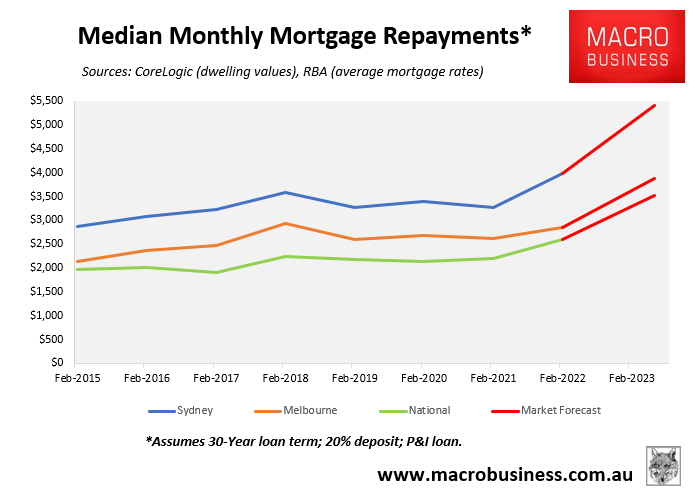

Markets are now tipping 2.65% of RBA rate rises by mid-2023. If this happened, it would raise mortgage repayments by 36%, equating to $930 extra in repayments a month on the median priced Australian dwelling:

If markets are right, and rates rise by 2.65%, then monthly mortgage repayments will balloon.

Monthly mortgage repayments on a median priced Sydney and Melbourne dwelling would rise even more, by $1,426 and $1,022 respectively.

The outlook is even more worrying for the 500,000 fixed-rate mortgages scheduled to expire by late-2023. Many of these borrowers originated their mortgages at rates of between 2.25% and 2.5%. Thus, if the RBA was to hike rates by 2.65%, as predicted by the markets, these fixed rate borrowers would face more than a doubling of mortgage rates once it comes time to refinance onto a variable mortgage.

If the markets end up being right, and mortgage rates surge by 2.65%, then thousands of recent home buyers across Australia’s suburbs will be in deep financial trouble.

For what it’s worth, I believe the markets are wrong for reasons explained in the video below. The RBA wouldn’t be so stupid to hike rates as quickly or aggressively as tipped by the markets, as it would crash both housing and the economy.