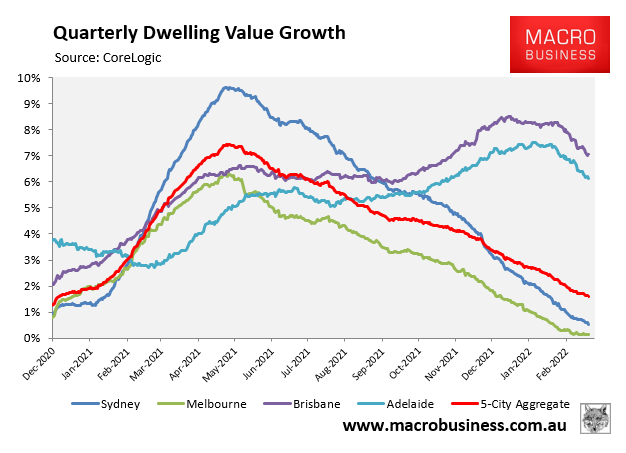

Because so much of the last house price cycle was driven by $500bn in cheap fixed-interest rate mortgages, their removal has been enough to snuff out price gains and begin a property price correction:

Prices are now falling in Sydney and Melbourne and decelerating fast everywhere else. Without the sub-2% fixed rates there is simply not enough credit to support prices.

This is going to eat away at consumer confidence before long and that component of the economy will begin to slow. This is all to the good. There’s a big pipeline of state government public investment in infrastructure to help support growth.

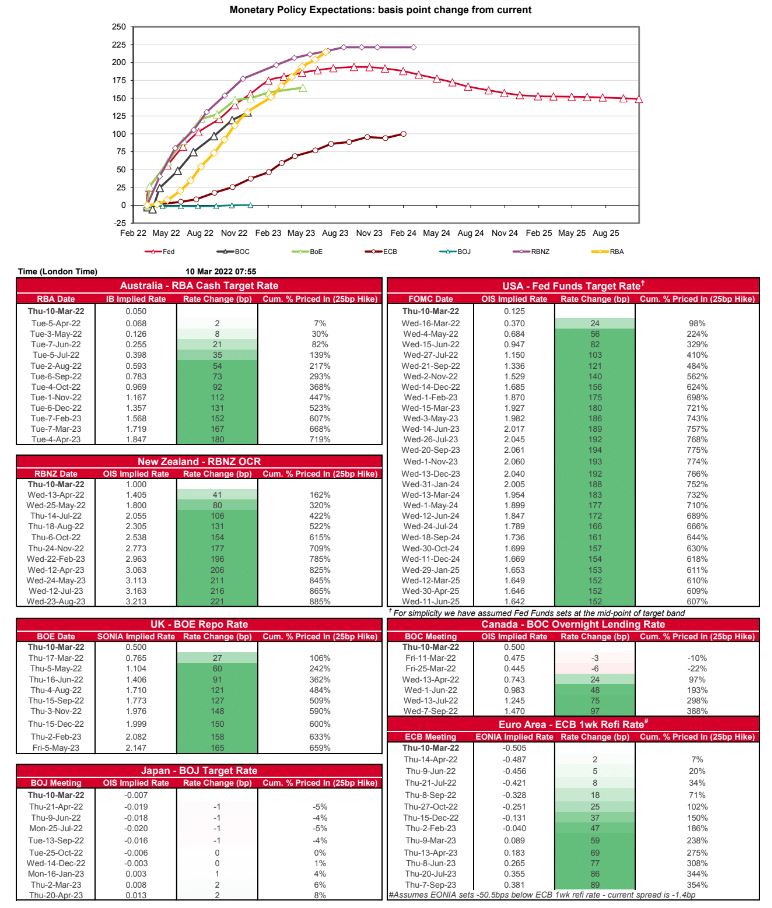

However, just imagine what is going to happen to already falling house prices if the RBA now tightens with ten…yes ten…rate hikes by mid-2023. That’s what interest rate markets are forecasting, via Westpac:

According to markets, Australia is headed for the highest cash rate in the developed world with a bullet.

Now, picture what will happen to the bulk of that $500bn in sub-2% fixed-rate mortgages as they roll off to flexible mortgage rates at 4.5% in 2023. Repayments will more than double overnight on the entire 20/21 mortgage bucket.

Good luck with that.