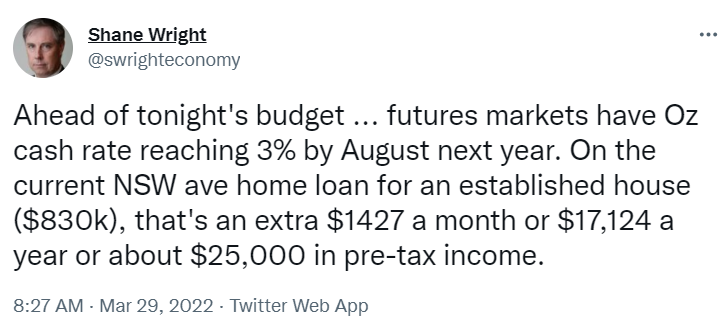

Just when you thought the financial markets couldn’t get any more crazy on Australian interest rates, the futures market is now tipping the RBA cash rate will rise to 3% by August 2023 from 0.1% currently:

A 2.9% increase in the RBA cash rate would represent twelve interest hikes in only seventeen months. As noted by Shane Wright above, the impact on household finances would be devastating.

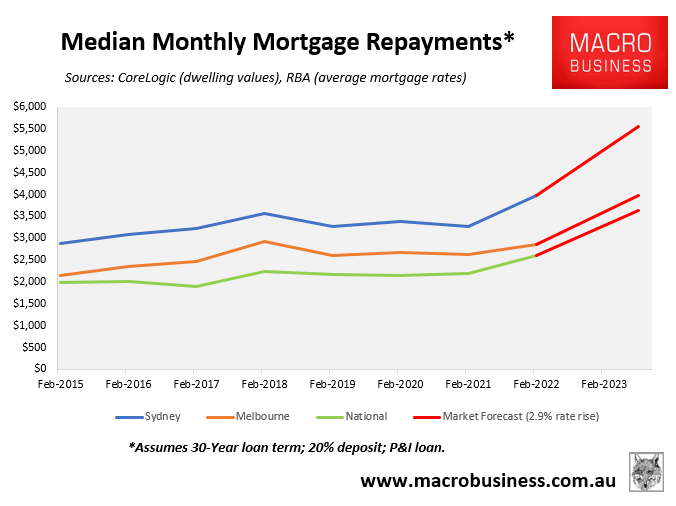

By my calculations, a 2.9% interest rate hike would lift the average discount variable mortgage rate to 6.35% (from 3.45% currently), assuming increases in the cash rate are passed onto mortgage holders in full. In turn, average principal and interest mortgage repayments would surge by 39%.

The dollar impact on monthly mortgage repayments is estimated below assuming an 80% loan-to-value ratio principal and interest mortgage on the median priced dwelling (as at February 2022):

Could you handle 12 interest rate rises in only 17 months?

Monthly mortgage repayments on the median priced Australian dwelling would surge by $1,025 under a 2.9% rate rise scenario.

The impact would be even more severe across expensive markets like Sydney and Melbourne. There, monthly mortgage repayments would surge by $1,571 (Sydney) and $1,126 (Melbourne) respectively.

Obviously, such a sharp increase in interest rates would place thousands of Australian mortgage holders under extreme financial duress, and would very likely crash both the housing market and economy.

For these reasons, the futures market’s latest interest rate forecast is delusional and won’t come to fruition. The RBA would never be so foolhardy.