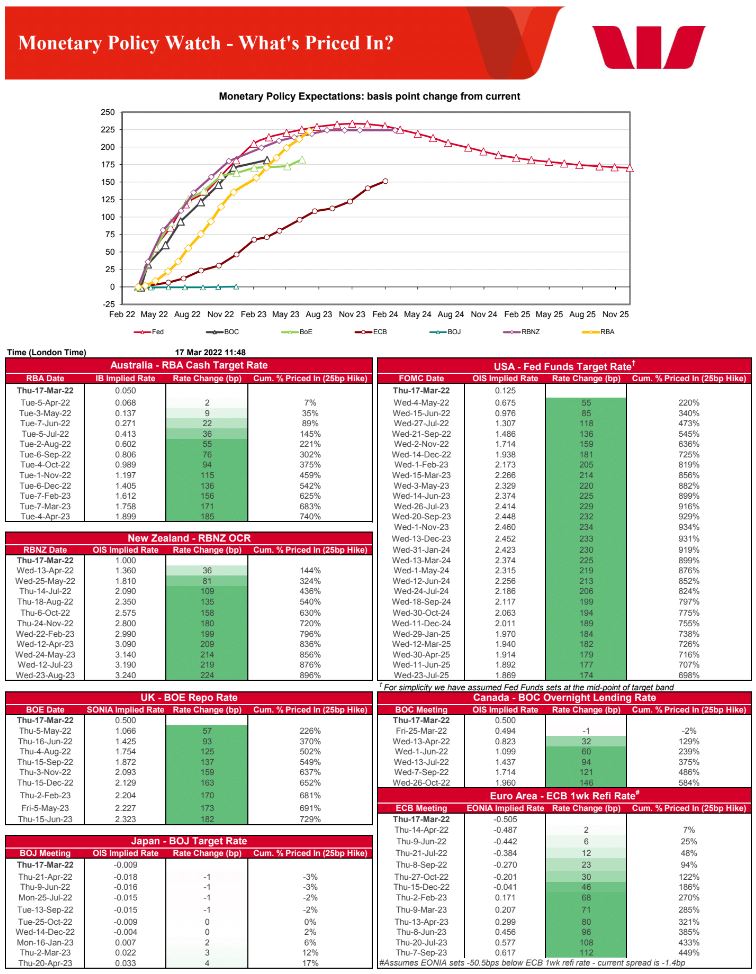

Amusing isn’t it? Markets are still preparing to halve Aussie house prices by hiking interest rates ten times by mid-2023. Via Westpac:

According to the RBA house price model, a tightening of credit of this magnitude and speed will crash house prices somewhere between a third and a half of value.

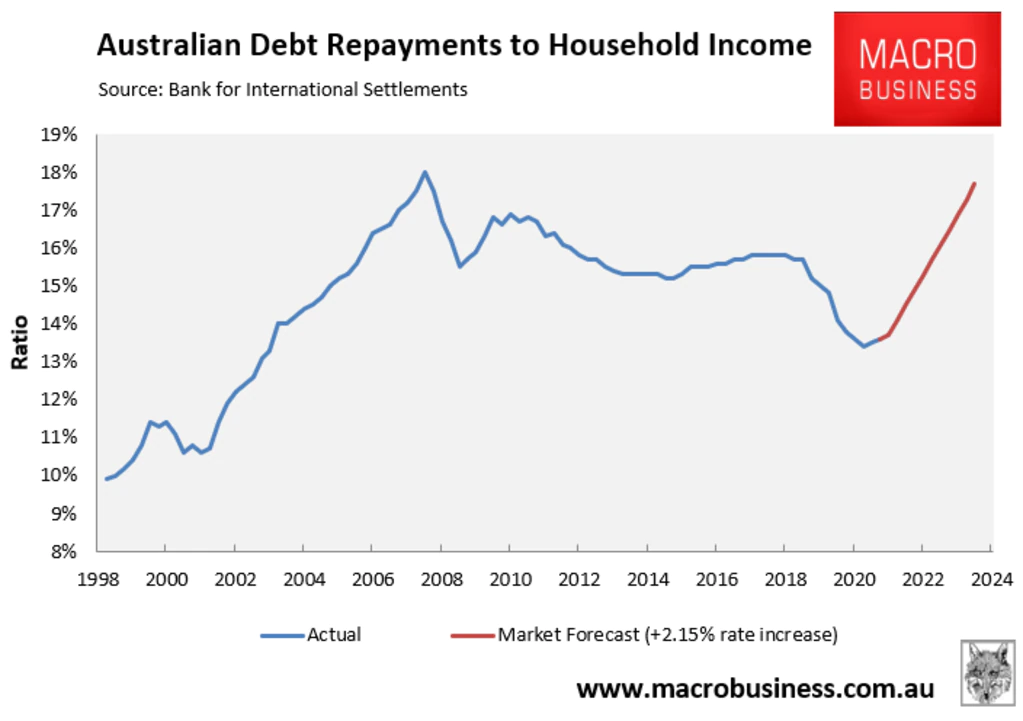

It’s easy enough to play out the implications. First, mortgage repayments would soar from 300-125% for all mortgages, gutting household discretionary income as repayments soared to the highest ever level (at pre-GFC peaks but without the wider economic boom to support it):

Next, some $3-5tr of value will be erased from household balance sheets.

This combined annihilation of Australian living standards will trigger a radical reduction in consumption and broader economic growth will crater and unemployment launch.

Australian banks will be insolvent by the end of 2023 as their loan collateral is also eviscerated and they are required to reweight tens of billions in reserves. Of course, adding to the hilarity, equity markets are currently bidding them up like crazy!

The banks will all be openly nationalised as their funding costs soar to paralytic levels and credit rationing turns the house price crash into endless Japanese-style debt deflation.

If the above rate hikes go ahead across the DM universe, the RBA’s mooted ten rate hikes will be transpiring within a global recession, cratering commodity prices and a raging equities bear market.

The Australian economy will be in the Second Great Depression. The budget wreckage will be unprecedented. Canberra will be in flames. And the RBA board hanging from a gibbet.

Even more bizarre, according to long-term bond pricing, all of this will transpire without any consequences for inflation or yields so Australia’s currency will be skyrocketing as our rates price deck moves above that in the US.

In short, current market pricing of the Australian interest rate outlook is irrational to the point of ludicrous.