For years I’ve argued that superannuation is more a tax minimisation scheme for the rich than a genuine retirement system.

Yet despite the system’s fundamental flaws, the federal government has increased the share of income that Australians are required to contribute into superannuation, damaging the Budget’s long-term sustainability, increasing inequality, and fattening the wallets of fund managers.

Like Groundhog Day – or maybe because an election is in the air – calls are growing to limit the amounts that wealthy people can dump into super.

Last week, Fund manager Mercer called for superannuation balances to be capped at $5 million, a stance already favoured by the likes of Super Consumers Australia and the Australian Institute of Superannuation Trustees:

Advertisement

Mercer senior partner David Knox said the distribution of superannuation concessions needed to change.

“We know that the biggest beneficiaries of the current super tax concessions are, in fact, those that need it the least – high-income earners,” Dr Knox told The Australian Financial Review.

According to The Australian’s James Kirby, wealth advisers are growing“increasingly concerned” that “investors with higher superannuation balances are in the firing line pre-election as a proposal to ‘cap’ how much can be kept in tax-protected superannuation gathers pace”:

Super is tax free up to $1.7m per person. Once that ‘cap’ is passed, tax must be paid on the extra investment income received. But there is no obligation for super investors to pay full tax on these amounts. They can leave the money inside the super system in so-called ‘accumulation phase’ where the tax is still low at 15 per cent…

The issue which was first identified in the government’s Retirement Income Review has been picked up in recent weeks by an unlikely coalition of interests with some citing misuse of tax concessions and others more likely to back the current proposal on the basis that the ALP might ultimately target amounts of considerably less than $5m…

The most recent research in the area which goes back to 2020 suggests there is around 11,000 with super in excess of $5m…

A new cap would mean superannuation investors would have to remove any funds in excess of $5m entirely from the super system – any such money could then be taxed at conventional marginal tax rates of up to 45 per cent plus the 2 per cent Medicare levy.

Advertisement

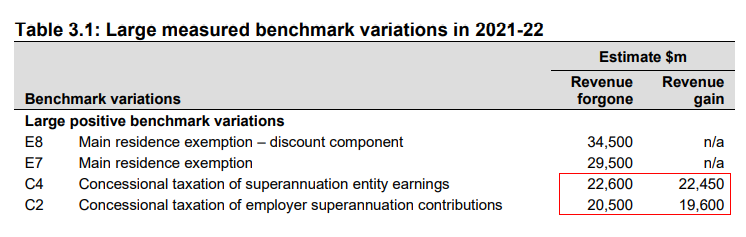

The Australian Treasury’s Tax Benchmarks and Variations Statement 2020-22revealed that the budgetary cost of superannuation concessions has ballooned past $40 billion, and is expected to grow over the forward estimates:

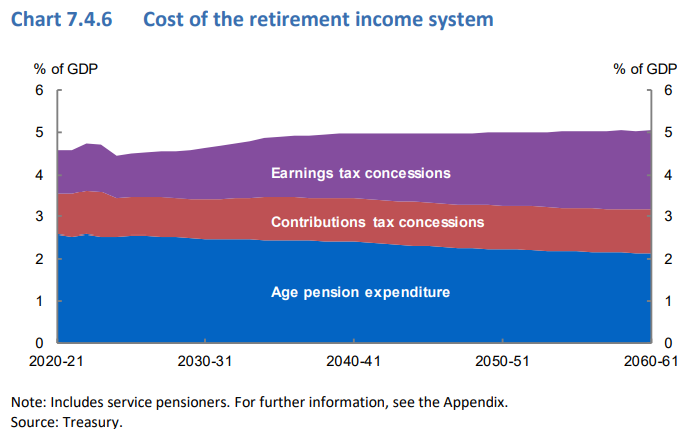

Treasury’s Intergenerational Report also showed that the cost of superannuation concessions will over take the cost of providing the aged pension by around 2040:

Advertisement

Cost of superannuation to overtake aged pension by 2040.

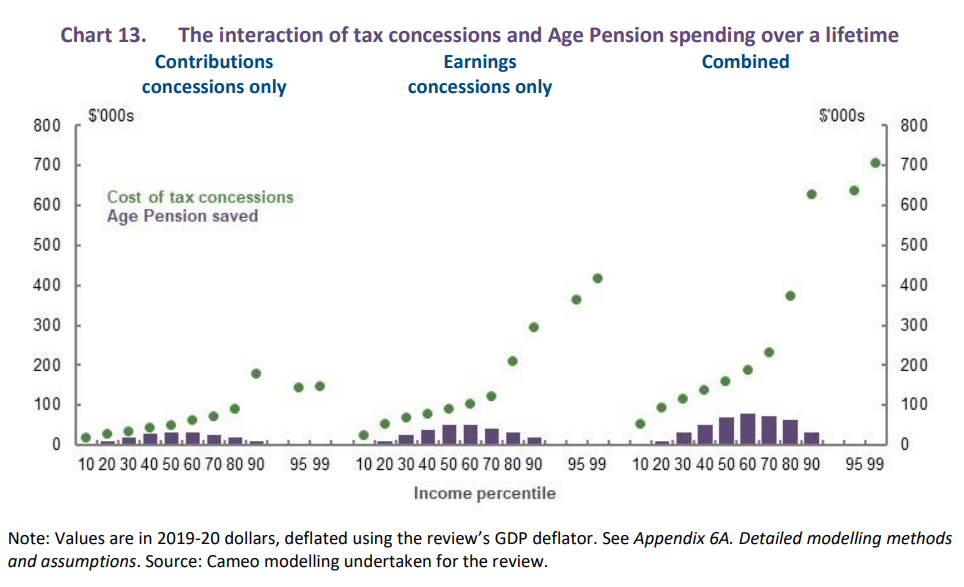

Meanwhile, Treasury’s Retirement Income Review, released in 2020, estimated that the superannuation system will cost taxpayers more in net terms over the long-run, that is after taking into account savings in Aged Pension costs. The Retirement Income Review also showed that superannuation concessions are poorly targeted to high income earners, thereby increasing inequality:

To the extent that superannuation tax concessions are contributing to higher superannuation balances of lower- to middle- income earners, they help to reduce Age Pension expenditure. But the main influence behind the growth in superannuation balances is the SG. Tax concessions are largely concentrated among higher-income earners who are close to and above preservation age. Across the income distribution, the lifetime cost of superannuation tax concessions is projected to outweigh the associated Age Pension saving (Chart 13)…

Advertisement

Thus, it is patently obvious that the superannuation system is grossly unfair and needs to change.

But rather than tinkering at the edges with $5 million caps, it would make more sense to unwind the superannuation system altogether and direct the budget savings into providing a more generous and comprehensive Aged Pension. This would improve efficiency, equity and budget sustainability.

This will never happen, of course, because the superannuation industry is now so large and powerful that genuine reform is impossible.

Advertisement

Labor is also tied heavily to union-owned industry super funds and created the system. Therefore, it vigorously defends the status quo and lobbies incessantly to lift the super guarantee.

The end result is that we are left with a Frankenstein’s monster system that actually worsens the sustainability of the Budget, favours the rich, and increases inequality.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.