Westpac with the note.

—

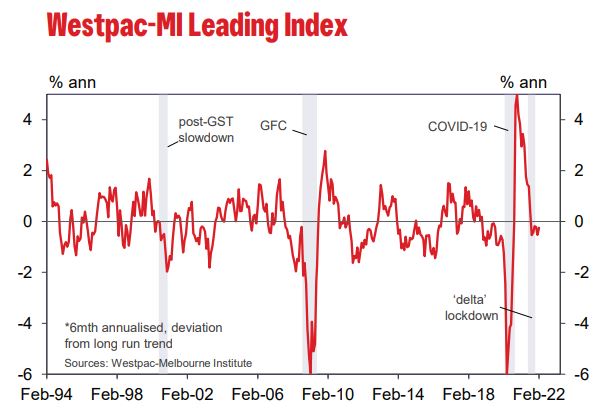

Previous estimates had the Index growth rate nudging into slight positive at the start of the year. That has been revised away with the Index growth rate marked down following updates showing a more material impact from the omicron outbreak in January. While the growth rate lifted in February, the latest read remains in negative territory but only slightly below trend.

In contrast with this cautious signal from the Leading Index Westpac is expecting strong above trend growth in 2022. This is largely due to the aftermath of the extraordinary emergency policy measures from both the fiscal and monetary authorities during 2020 and 2021.

Australian households have accumulated around $250 billion in excess savings while their current savings rate, at 13.6%, is well above the ‘normal’ savings rate of around 6%. As households move that savings rate down to more normal levels, considerable spending power will be freed up.

While we expect households to be careful with their accumulated excess savings, the fall in the savings rate and solid disposable income growth will support very strong consumer spending. Not surprisingly, the Leading Index is likely to be understating the delayed impacts of these extraordinary emergency policies.

While still negative, the Index growth rate has lifted from –0.54% in September 2021 – when the two major eastern states were still in delta lockdowns – to –0.25% in February 2022. The 0.29ppt improvement has been driven by: a widening yield spread (+0.51ppts); a continued recovery in US industrial production (+0.18pts); and improved labour market conditions, hours worked and the Westpac-MI Unemployment Expectations Index adding a further 0.24ppts on a combined basis (despite a sharp drop in hours worked in the most recent month).

This was partially offset by considerable drags from equity markets (–0.29ppts), dwelling approvals (–0.27ppts) and commodity prices (measured in AUD terms, –0.13ppts). Note that the surge in commodity prices seen since Russia’s invasion of Ukraine has yet to be reflected in the Leading Index. This will be captured with the March update.

The Reserve Bank Board next meets on April 5. The Minutes from the March Board meeting emphasised the Board’s patient approach while noting the slow recovery in wages growth.

Such commentary effectively rules out a move at the April meeting.

We expect that the Board would be disposed to the standard protocol of adopting a clear policy bias prior to adjusting the policy rate.

After digesting a substantial lift in inflation in the March quarter on April 27 and further progress on wages growth which will be announced on May18 we expect the Board will move to a tightening bias over June and July prior to raising the cash rate by 0.15% on August 2.