A cabinet paper from New Zealand’s Ministry of Business Innovation & Employment, which explains how New Zealand has morphed into a low-wage guest worker economy on the back of extreme levels of temporary migration.

The cabinet paper also recommends the Ardern Government “rebalance the immigration system by pursuing a lower overall volume of migrants and improved composition of temporary and skilled migrants (compared to the pre-COVID-19 trajectory)”.

Below are key extracts from this paper:

Our pre-COVID reliance on temporary overseas workers and rate of population growth have been recognised for placing unsustainable pressure on our infrastructure (such as housing and transport) and placing downward pressure on New Zealand workers’ training, wages, terms and conditions…

Commentators note immigration settings could do more to support greater productivity…

We have an opportunity to rebalance our settings before we reopen our borders, rather than returning to 2019 levels and trying to reduce the rate from there…

The case for an immigration system rebalance: why we need lower overall volumes of inward migration, particularly of lower-skilled migrant workers…

Flags have been raised by experts regarding the volume and composition of migration to New Zealand and the challenges this poses to the country’s longterm prosperity.

The OECD, the New Zealand Productivity Commission and the New Zealand Institute of Economic Research are among those who have suggested that policy change may be required. For example:

‘The employer-assisted temporary work visa system is not limiting recruitment of migrants to resolving genuine skills and labour shortages, is attracting too many low-skilled migrants and may be weakening incentives for employers to employ and train New Zealanders.’

‘There have … been wellbeing costs [from large numbers of immigrants], including impacts on housing costs, urban infrastructure costs, congestion, and displacement of low-skilled New Zealanders from jobs.’

‘Infrastructure and housing supply have not kept pace with the demand generated by high net migration, resulting in traffic congestion, water pollution and large increases in house prices, which has redistributed wealth to property owners from non-property owners, who tend to be less well off.

There has been a recent surge in the rate of migration to New Zealand, and in New Zealand’s population growth rate, since about 2014. This has been fuelled by increasing inward flows of temporary migrant workers and international students in particular…

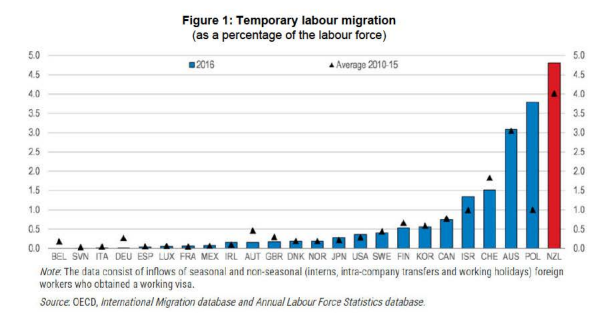

The increase has been significant. The decade prior to COVID-19 saw the number of people on temporary work visas in New Zealand more than double from fewer than 100,000 to more than 200,000. Temporary work visa holders now make up almost 5 per cent of New Zealand’s labour force. Pre-COVID-19 there were also around 60,000 people approved on (fee-paying) student visas each year, and the total number of student visa holders remains historically high, at over 100,000 each year.

As overall numbers have grown, the number of partners of visa holders who come to New Zealand is growing. The partners of some workers and some student visa holders are eligible for an open work visa for the same length as their partner’s visa. Most people being granted residence are partners, including partners and dependents of skilled migrants.

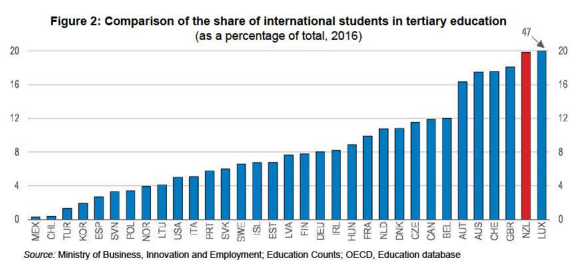

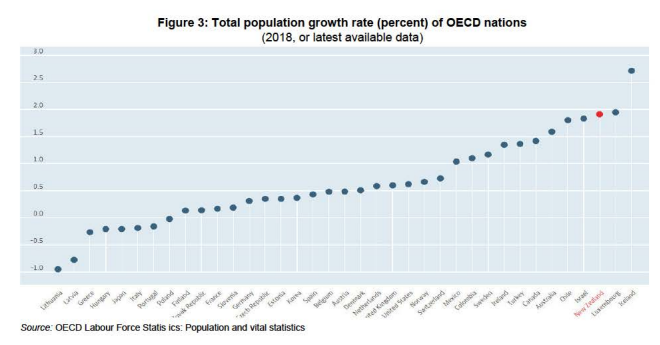

New Zealand is a conspicuous outlier compared to other OECD countries with the highest share of temporary work visa holders in the labour force among OECD countries by a significant margin (Figure 1), one of the highest shares of international students in tertiary education (Figure 2) and one of the highest population growth rates in the OECD (Figure 3)…

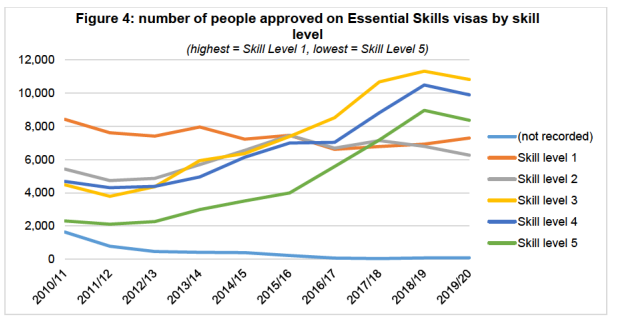

Migration is increasingly concentrated at lower skill levels… Nearly half of all Essential Skill visa approvals in 2019-20 were at the two lowest (of five) skill levels, up from 28 per cent in 2010-11 (Figure 4)…

In the international student market too, the growth has been at the lower levels – in below degree-level courses through private training establishments, with less market share over time for universities.

This has flow-on effects to the skill level of our long-term workforce, with more than 80 per cent of residence applications coming from people already in New Zealand…

The high and increasing volumes and the falling average skill level of temporary migrants are widely seen as concerning, with specific risks including:

reducing the attractiveness to employers of New Zealanders…

providing few incentives for employers to offer better wages and/or terms and conditions, including training and better career pathways

embedding low-cost labour models which in turn reduce incentives to shift to potentially more productive ways of organising businesses, including investment in automation and other changes to overall capital/labour ratios.

High levels of population growth can put pressure on infrastructure, including on housing and social services, especially when the expansion of said infrastructure cannot keep pace with said growth…

Returning to our pre-COVID immigration settings risks frustrating some of the foremost economic and social outcomes that the Government is working to achieve, such as higher productivity and higher wage economy and better jobs…

The above analysis could be equally applied to Australia, which suffers exactly the same problems.

Advertisement

The question is: will the Australian Labor Party mirror the New Zealand Labour Party and seek to lower Australia’s immigration intake to sensible and sustainable levels, alongside improving the quality of said intake?

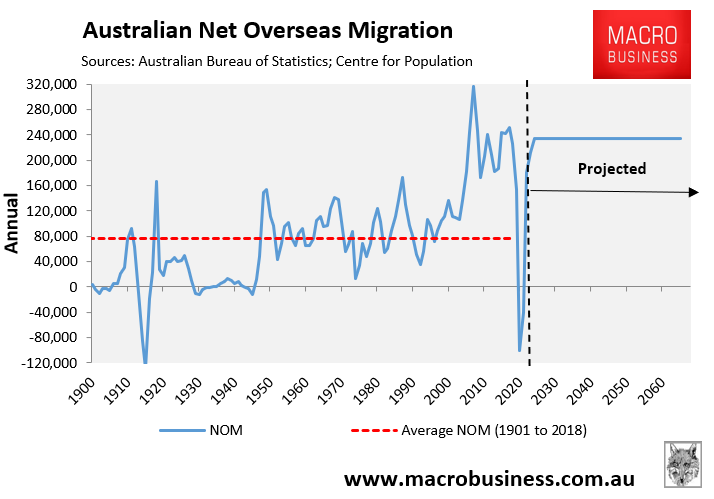

C’mon Albo, it’s time to stand up for Australian workers and reject the return to ‘Big Australia’ mass immigration, which is projected to flood the nation with 235,000 warm bodies every year into eternity.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.