How high will the RBA hike interest rates?

By Gareth Aird, head of Australian economics at CBA

Key Points:

- An RBA tightening cycle looms and we continue to expect the RBA will deliver the first hike in the cash rate at the June Board meeting.

- Our central scenario has the cash rate climbing to 1.25% by Q1 23 where it is forecast to stay over the remainder of 2023.

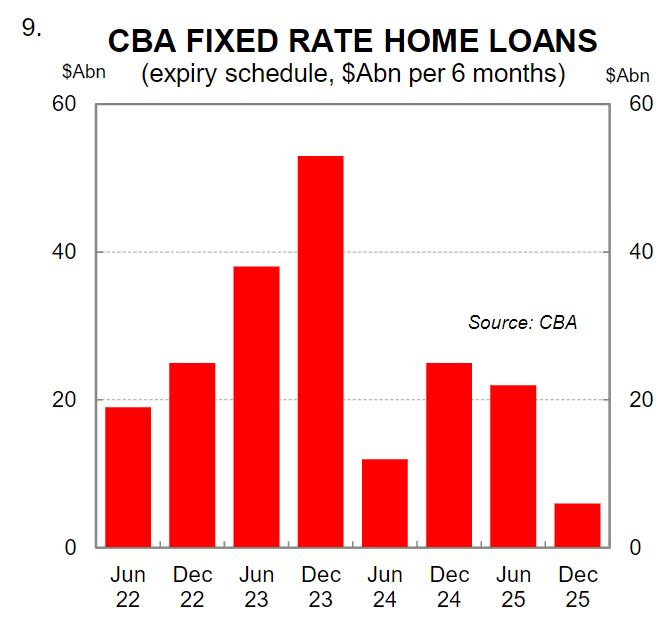

- We assess 1.25% to be the neutral cash rate and therefore at this stage we believe once the cash rate is at that level it is the logical place for the RBA to pause in its tightening cycle – there is also a significant expiry of fixed rate home loans in 2023 which will create a natural tightening over 2023, even with the RBA on hold.

- It is possible, however, that the RBA takes policy into contractionary territory; either intentionally to put downward pressure on inflation or inadvertently if the RBA’s assessment of neutral is higher than ours.

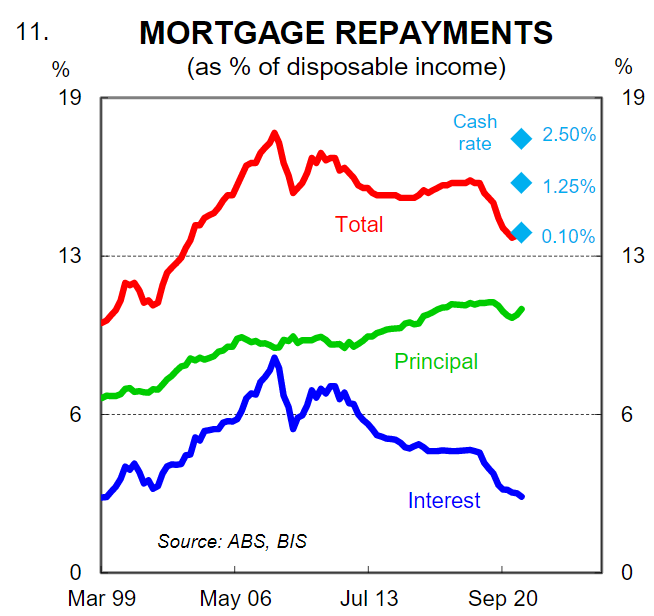

- Our analysis indicates that a cash rate of 2.50%, i.e.in-line with market pricing, is deeply contractionary and would result in mortgage payments as a share of household disposable income rising to a record high(data we use goes back to 1999).

- Fiscal policy will play a very important role in determining how high the RBA takes the cash rate –looser fiscal policy than we currently anticipate increases the probability that the RBA takes the cash rate to a contractionary setting.

- If the RBA commences raising the cash rate later than our June start date that also raises the risk that the cash rate is taken above our estimate of neutral.

Overview

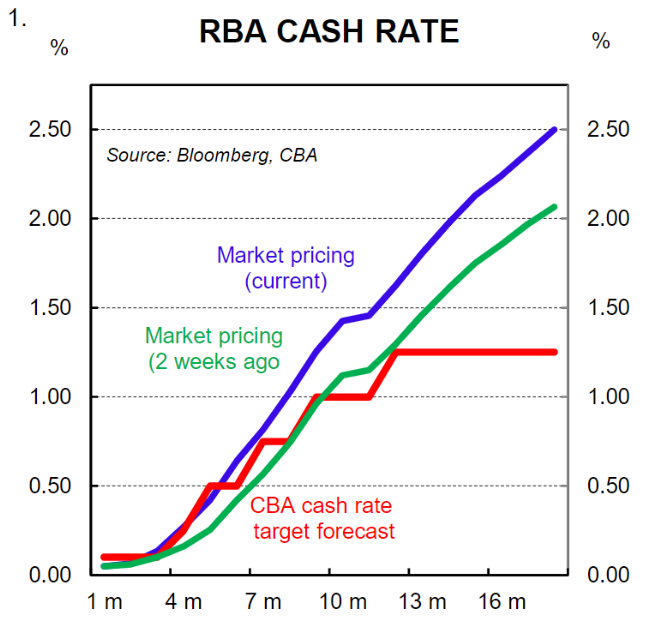

Markets have moved very quickly to price a much more aggressive RBA tightening cycle than we anticipate (Chart 1). We acknowledge that there is a clear risk that the RBA takes the policy rate above our estimate of the neutral cash rate, which we believe isjust1.25%. And as we discussed earlier in the week, fiscal policy will have a large bearing on where the cash rate eventually peaks. Indeed the outlook for public policy is complicated by an upcoming federal election.

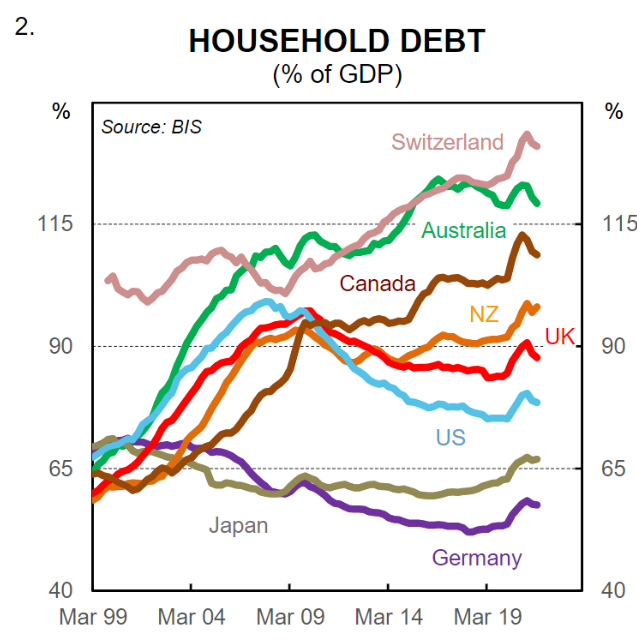

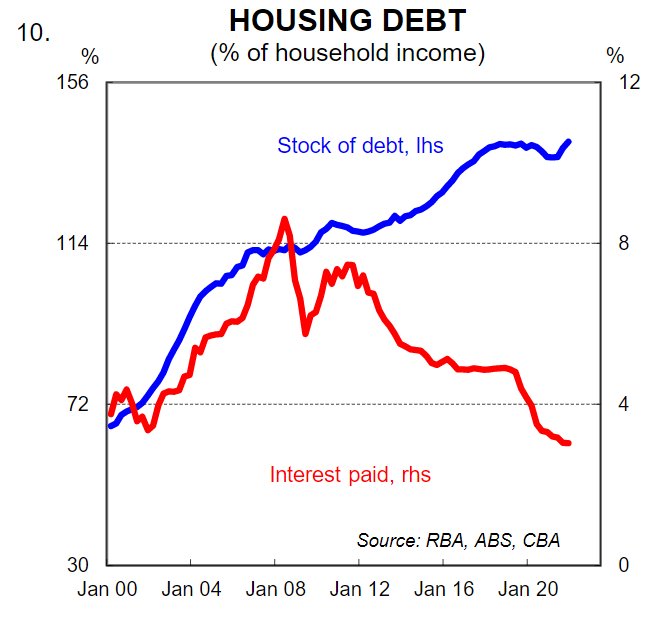

However, the economy is not static. Interest rate increases will generate changes in household behaviour and consumer confidence, which in turn will impact economic outcomes. For context, we estimate there are over one million home borrowers who have never experienced an increase in mortgage rates. The Australian household sector is one of the most indebted in the world (Chart 2). This means that rate hikes have a more powerful impact on our household sector than they doin almost all other jurisdictions. Our expectation is that many households will tweak spending decisions as interest rates begin to normalise. Those changes will become more pronounced as the RBA moves through their impending tightening cycle.

The RBA will look to engineer a smooth policy transition from an accommodative stance to a neutral one. Taking monetary policy to a contractionary setting will not be Plan A in the RBA’s playbook.

The RBA has a very good track record of calibrating policy appropriately through a tightening cycle. Their hiking cycles have generally not preceded economic downturns, which is a claim some other central banks can’t make, notably the US Federal Reserve. The RBA’s task is also made less difficult in an inflationary environment given they have an inflation target that is higher than most other central banks. The RBA wants to see inflation and wages growth settle at a higher level than the other major central banks. Indeed that is their objective. In this note we discuss why we believe the upcoming tightening cycle will be shallow. Our thoughts are very much focussed on what rate hikes will do to the Australian household sector.

A reminder of the CBA call on the RBA

On 15 February 2022 we shifted our central scenario for the RBA to commence normalising the cash rate to June 2022, from August 2022. Since that time there have been a number of developments that have supported that call.

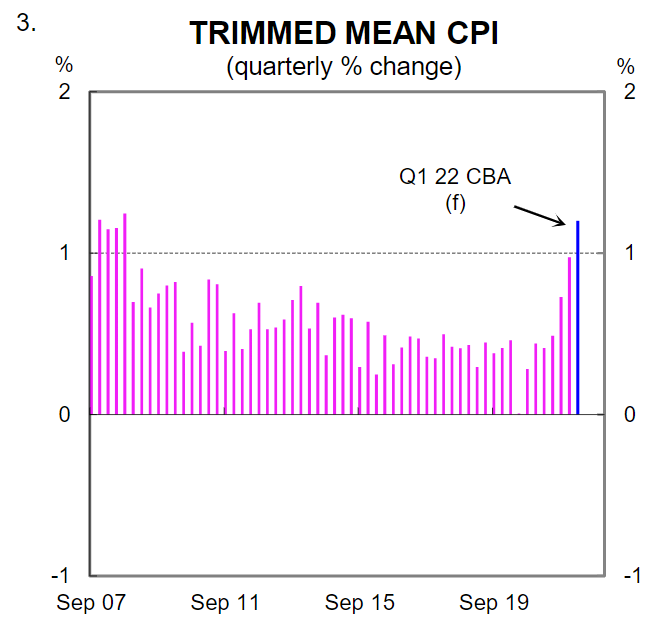

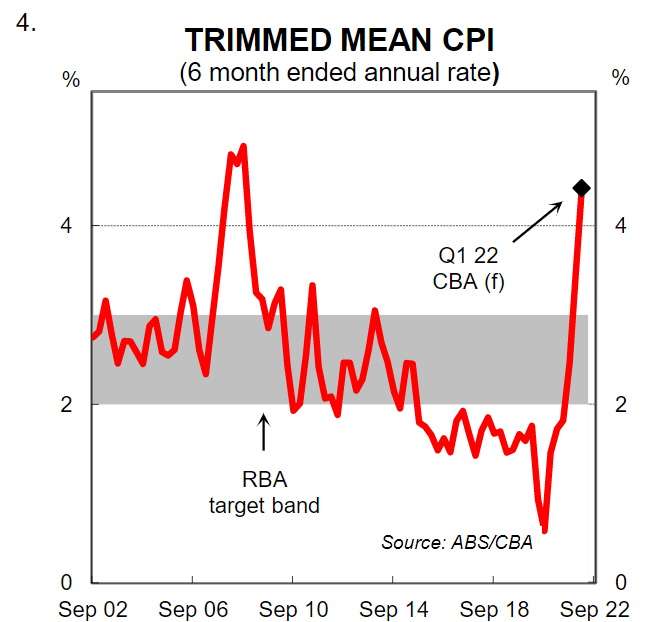

First, RBA Governor Lowe stated on 9 March that the Board did not necessarily need to see two further CPIs before raising the cash rate. Recall that on 11 February the Governor said that, “another couple of CPIs would be good to see” when asked if he like to see at least one or two more CPIs before concluding inflation is sustainably within the target range (note that the Q1 22 CPI prints 27 April and Q2 22 CPI prints 27 July). At the time we did not interpret the Governor’s comments as a firm commitment to needing to see two further CPIs before raising the cash rate. For context we forecast the Q1 22 trimmed mean CPI to increase by 1.2%/qtr, which would take the annual rate to 3.4%. The six month annualised rate on our figuring in Q1 22 will be 4.5% (Charts 3 & 4).

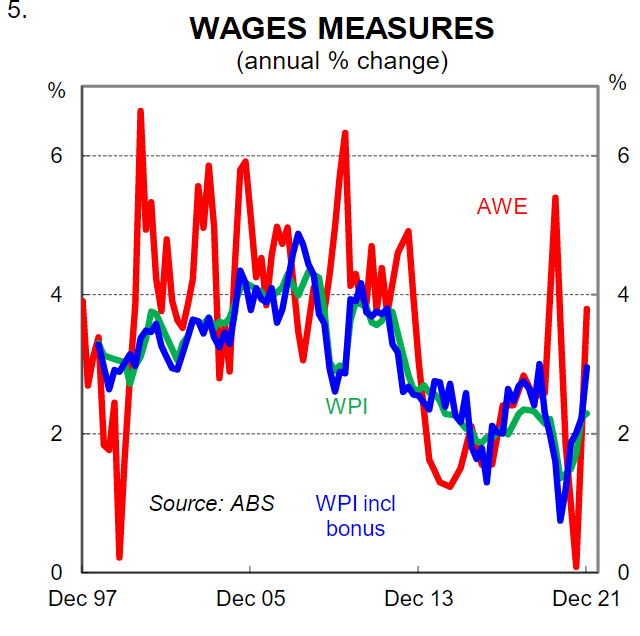

Second, the RBA has formally shifted the focus away from “aggregate wages growth” to “labour costs”. This creates flexibility to raise the cash rate without being beholden to the Wage Price Index printing at a particular level (chart 5).

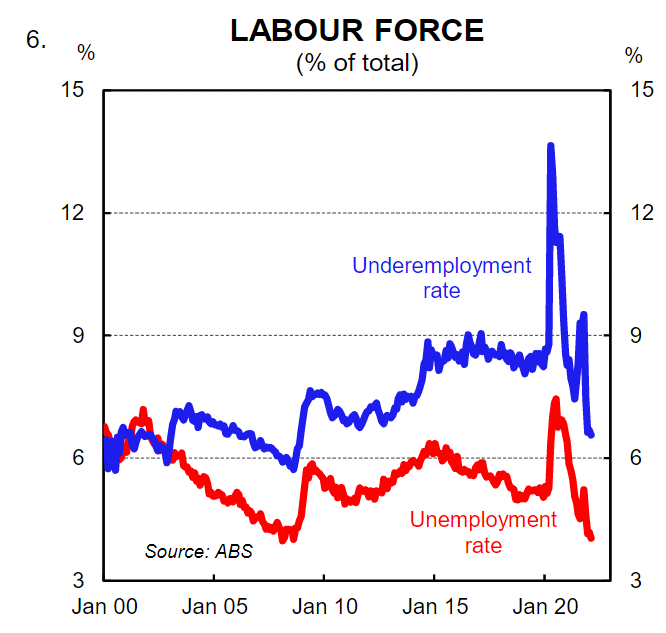

Third, the recent labour market data has been stronger than the RBA anticipated. The RBA’s forecast from the February Statement on Monetary Policy (SMP) put the unemployment rate at 4.0% at June-2022. That forecast has already been achieved based on the 4.0% unemployment rate in February 2022 (chart 6). This means the RBA will likely downwardly revise their forecast profile for the unemployment rate in the May SMP (subject to the March labour force survey which will be published on 14 April).

Fourth, the RBA has very recently expressed some concerns that there may be a shift upwards from the low“ inflation psychology” over the past two decades. Indeed Governor Lowe has recently made reference to the RBA as potential future inflation fighters.

These four developments leave us comfortable with our central scenario that the RBA commences normalising the cash rate in June. There is now a focus on what the tightening cycle looks like. Of course picking the exact timing of rate hikes through a tightening cycle is false precision. But economists need a forecast profile. Our central scenario sees the RBA deliver a 15bp increase in the cash rate in June 2022, which would take the cash rate to 0.25%. We expect that to be followed by two 25bp increases in Q3 22 and a further 25bp hike in Q4 22, which would take the cash rate to 1.0% by end-22. We expect one further 25bp rate hike in Q1 23 that takes the cash rate to 1.25% -our estimate of the neutral cash rate.

The neutral rate

Typically when a central bank seeks to normalise monetary policy the first stopping point is “neutral” or the neutral interest rate. In the RBA’s case, the neutral rate is the cash rate consistent with full employment, trend growth and neither upward nor downward pressures applied on the price level through monetary policy. It can be thought of as the cash rate that exerts neither contractionary nor expansionary forces on the economy. There are a variety of ways to estimate neutral. Our preferred approach is a pragmatic one which looks at the impact that changes in the cash rate have on debt serviceability for the household sector.

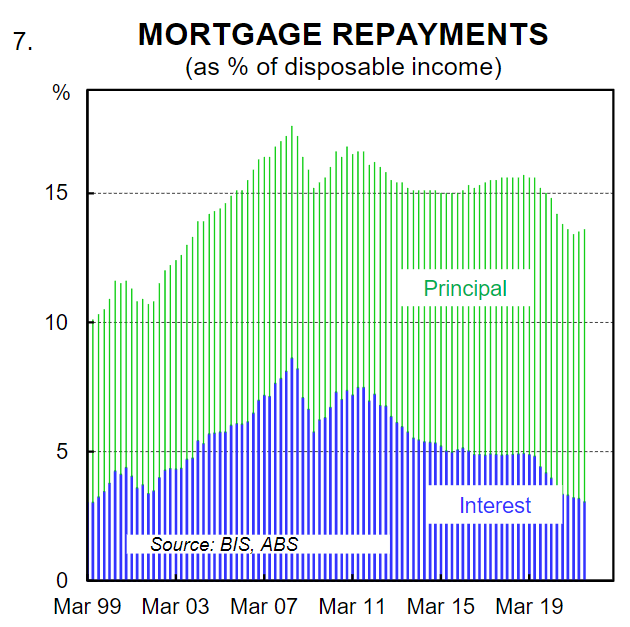

Our analysis indicates that a cash rate of 1.25% would take mortgage repayments as a share of household disposable income to ~15½%, which is the level which repayments have averaged over the past 20 years (Chart 7). Note that this analysis assumes that all mortgage debt is floating, which it basically is in Australia over a three year period; most fixed rate mortgages expire within 3 years.

We believe that mortgage repayments of ~15½% as a share of household disposable income should be considered a ‘normal’ level based on the notion that the economy has been in equilibrium on average over the last two decades.

That of course is a big assumption. It could be argued that the economy has been in a false equilibrium over the previous two decades given interest rates have been in a structural decline. In other words, in order to maintain some semblance of equilibrium, monetary policy has been required to be a tailwind on the economy which explains the decline in the neutral rate. But that idea is probably best explored in another paper. We do not know for sure if 1.25% is the magic number for the neutral cash rate. But we can calculate that a cash rate of 1.25% would take mortgage repayments to around their average share of household disposable income.

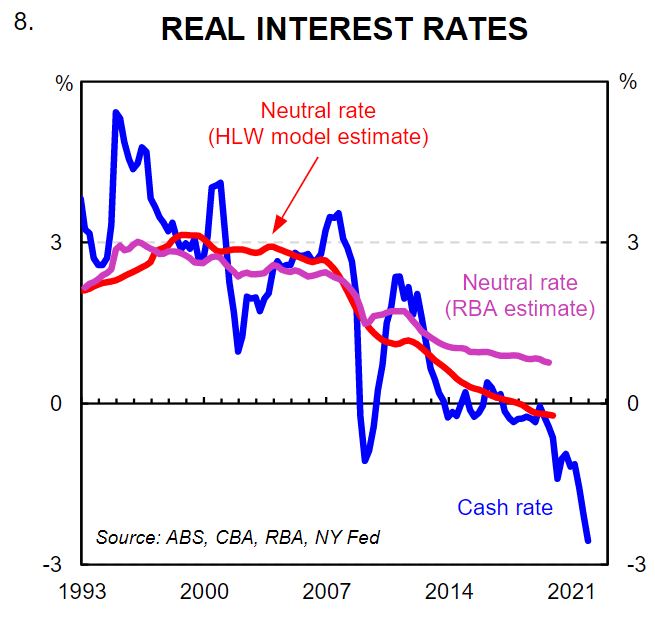

My colleague Stephen Wu has also looked at the neutral cash rate through a more academic lens. Stephen’s work, based on the Holston-Laubach-Williams model, points to a neutral rate of ~1½% (Chart 8).

The case to hike above neutral

Our central scenario sees the RBA sit on the sidelines once they have taken the cash rate to 1.25%, our estimate of neutral. Based on our forecast profile for the cash rate this is reached in Q1 23. And as we have covered previously, over the remainder of 2023 a natural tightening continues given the fixed rate home loan expiry schedule (Chart 9).

Our forecast profile for the cash rate to sit at 1.25% over 2023 looks radically different from current market pricing. Financial markets have priced a 2.50% cash rate in eighteen months.

We are very open to the idea that the RBA may need to take monetary policy into contractionary territory. Inflation will be above the target band when the RBA commences its tightening cycle and we believe we are already at full employment. As such, there is a genuine risk that the RBA’s very patient approach to normalising the cash rate leads to stronger inflation that is harder to contain. Consequently, it could be forced to raise rates more abruptly and to higher levels than we have in our profile for the cash rate.

However, we do not believe we are at the point where we need to incorporate a contractionary policy setting into our base case for the RBA. Rather we prefer to think about it as a risk to our central scenario.

Increases to the cash rate will be very powerful given the level of household indebtedness in Australia (Chart 10). Rate rises will be far more potent than in most other jurisdictions where households do not carry as much debt. In addition, the transmission mechanism from the cash rate to mortgage rates is much more direct in Australia. This means RBA rate hikes have a more immediate impact on the Australian economy than rate hikes from some other key central banks will have on their respective household sectors.

Here we note that our rates strategists believe there is a risk that the interest rate for the average standard variable loan rate could increase by a little more than the cash rate over the upcoming tightening cycle, given the cost of funds for lenders has increased.

We conducted some scenario analysis to highlight the sensitivities of changes in the cash rate on mortgage repayments (here we assume changes in the cash rate and the standard variable rate are the same). Our work indicates that a cash rate of 2.50% would take mortgage repayments to their highest level on record as a share of household disposable income (Chart 11 –note that the data from the Bank of International Settlements dates back to 1999). For context, the 17.6% peak in mortgage repayments as a share of income was in June 2008, just before the global financial crisis (the cash rate was 7.25% at the time). The RBA subsequently took the cash rate down to 3.0% by August 2009.

Our message here is that the corridor in which the RBA can move the cash rate from where it goes from what we estimate to be a neutral setting to a deeply contractionary one is very, very narrow. And the reason it’s so narrow is very simple –the record amount of household debt as a share of income means the impact of rate hikes on the household sector is greater than at any other point in time. We should add here that leverage is still rising–housing credit was 7.7%/yr at January 2022,which is significantly stronger than income growth. It is also worth pointing out that the percentage change in interest rates is incredibly large for each absolute increase in the cash rate given the starting point is a record low cash rate. It means that the interest cost on debt goes up very quickly in percentage terms for a given increase in the cash rate.

The RBA reaction function changes once the tightening cycle starts

The RBA’s reaction function to commence hiking rates is based on lagging indicators of the economy; inflation, wages and unemployment. But the RBA’s reaction function once it starts normalising policy will need to shift to forward looking indicators of the economy, otherwise the RBA will inadvertently take the cash rate too high.

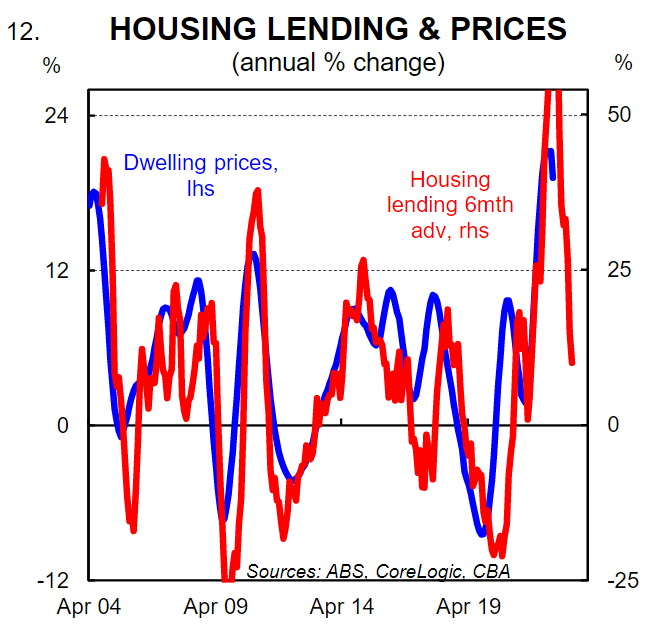

We do not know yet what the RBA will focus on to guide them as to how high and quickly they should take the cash rate. But we believe the RBA will place weight on the impact rate hikes have on the demand for credit, which in turn has a big influence on the housing market (Chart 12).

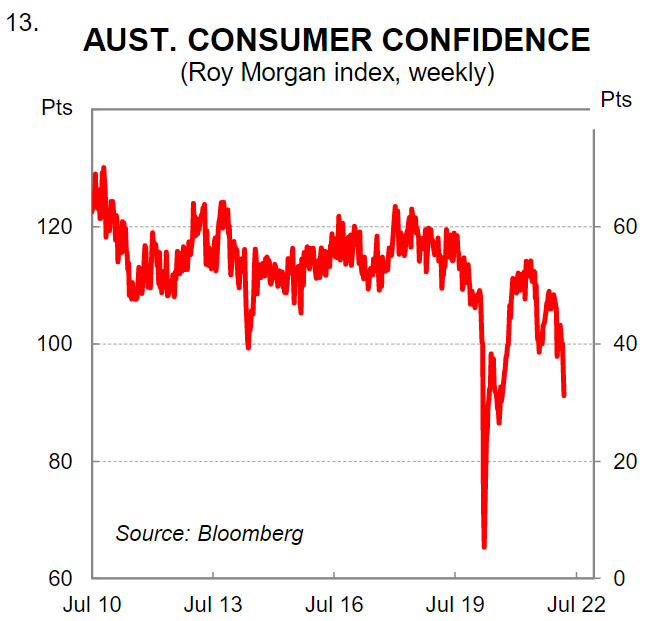

The RBA does not target home prices. But the housing market and the broader economy cannot be separated. Changes in home prices impact wealth, household balance sheets, sentiment, consumer behaviour and spending decisions. There is already signs of consumer anxiety creeping into the survey data (Chart 13). Rising consumer prices and talk of rate hikes will do that.

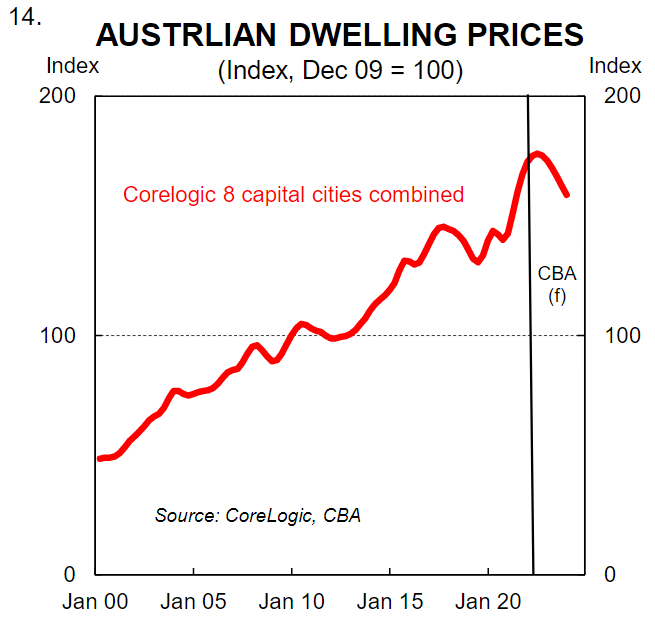

Monetary policy is the key determinant of house prices in the short run. Earlier this month we released updated home price forecast that incorporated our revised profile for the RBA cash rate. We expect national dwelling prices to end the year broadly flat and for prices to decline to ~8% in 2023 (Chart 14). Such a decline we believe would have no negative material impact on the economy.

However, we would expect bigger falls in home prices if the RBA was to take the cash rate higher than we currently anticipate. Larger falls in home prices would have a negative impact on the real economy.

Households are less likely to spend accumulated savings if interest rates rise too far and home prices fall too quickly. Indeed the argument that savings buffers will insulate the economy from rising interest rates starts to unravel if households become anxious about rising rates and declining home prices. Put another way, households are less likely to dig into savings buffers to fund discretionary consumption in an environment of sharply rising rates and falling home prices. Such a situation is unwanted and can be avoided.

In summary, the outlook for GDP, employment and wages growth in Australia is very positive. The RBA will seek to keep that outlook intact while it normalises the cash rate. As such, we maintain our view the tightening cycle will be shallow by historic standards and continue to look for the RBA to pause in early 2023 when the cash rate reaches 1.25%, our estimate of neutral. There is a clear risk that the RBA takes the cash rate to a contractionary setting. But it’s a risk that does not warrant crystallising into our base case at this point.