For much of this year, I have been skeptical of interest rates increases in Australia. There were five reasons for this.

First, the Australian labour market is still struggling to deliver wage gains consistent with sustainably rising inflation. In the latest data, only a fifth of surveyed labour market segments are delivering wage gains above the RBA’s 3% threshold.

Second, the RBA knows that it has embedded a large and automatic rate-hiking sequence moving into 2023. Come next year, the $500bn of fixed-rate mortgages that drove the pandemic house price boom will roll off to much higher floating rates. The housing market is already seeing falling prices owing to only the removal of the formerly cheap fixed rates.

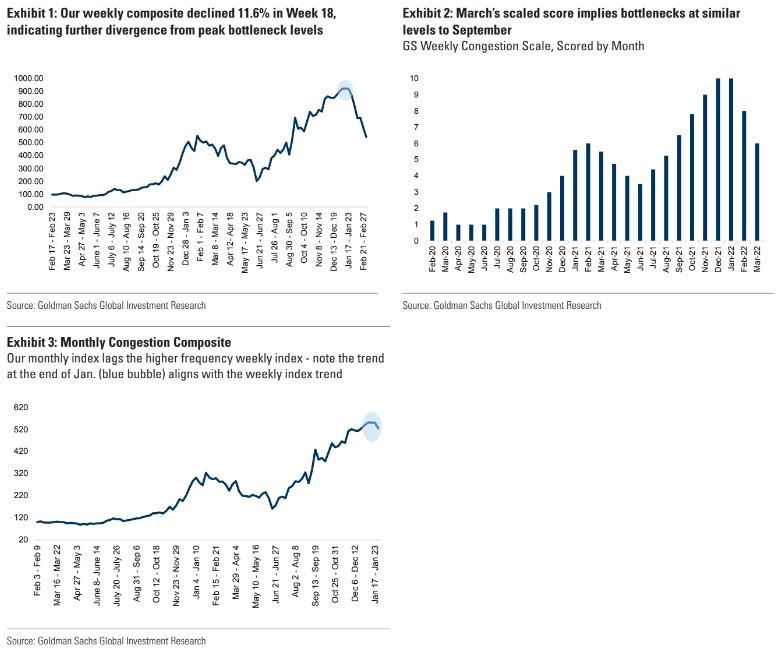

Third, I expected supply-side bottlenecks to ease as DM goods demand passed the baton to rising services activity post-COVID. This is happening, even though it has been slowed by a series of shocks that includes the Ukraine war, energy prices and OMICRON outbreak in China. In particular, car supply chains are starting to clear. Goldman:

Advertisement

This will lead to deflation in the global supply chain the more it advances.

Fourth, the Chinese construction economy is very weak as its property bust continues and, I argued, that this would deflate bulk commodities and energy prices in due course. It is still far weaker than anybody expected and producer deflation was well underway.

Advertisement

However, that argument was turned on its head as the Ukraine war and Russian sanctions introduced a new shock to supply and commodities have instead spiked. Even so, markets seem not to understand yet that this commodity boom will not deliver many benefits to most Australians given a lack of follow-on investment.

This brings me to the fifth and most important argument for why interest rates may not rise in 2022. It is this, TS Lombard:

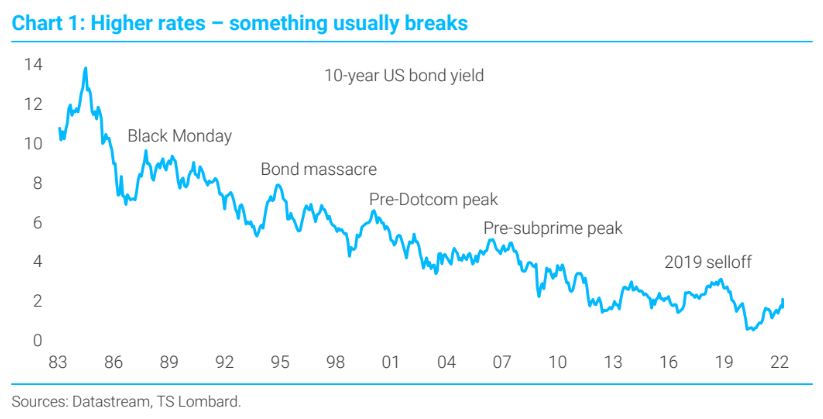

As every investor knows, interest rates have trended lower for 40 years and whenever central banks have tried to break out of this megacycle, something has gone wrong in financial markets and/or the real economy. Most pundits blame rising debt levels. Low interest rates encourage households, businesses and governments to take on more debt, which, in turn,makes the economy more sensitive to borrowing costs. In fact, you do not need to be an avid goldbug to realize that the post-Bretton Woods financial system seems to be stuck in a “bad equilibrium”, since high levels of leverage also add systemic vulnerabilities, which, in turn, increase the demand for safe assets, putting further downward pressure on interest rates. So, given the 40-year trend of “lower lows” and “lower highs” in interest rates, perhaps it is not surprising that most investors are sceptical about how far the world’s central banker sare going to be able to hike this time round as well. The possibility of an inversion in bond markets only reinforces this scepticism.

Advertisement

Before the FOMC had hiked even once we saw considerable distress in global junk debt spreads, so it was my view was that it would not take much tightening to trigger a new accident.

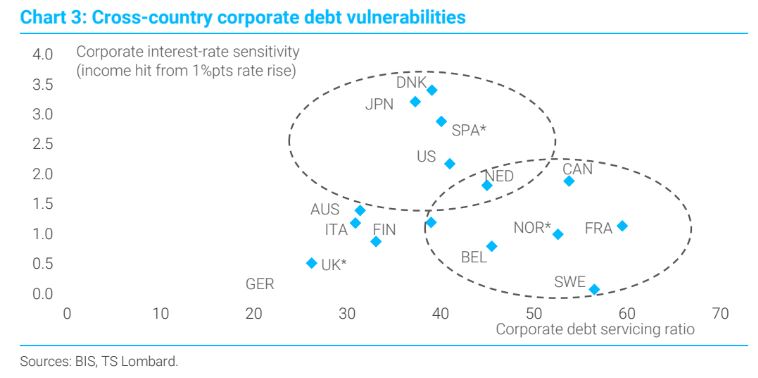

Where might it come? For most DMs, the key vulnerability is corporate debt:

Advertisement

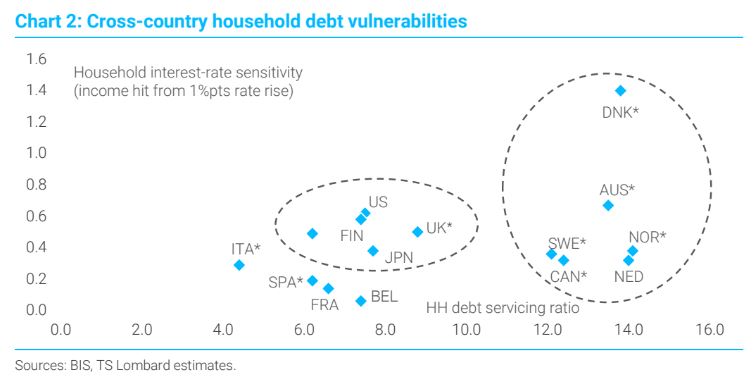

Not so Australia, where households carry the debt burden:

Australians coming a cool second in the world for leverage to mortgages, says it all.

It is the case that the balance of risks has shifted towards Aussie rate hikes post-Ukraine given the positive terms of trade shock. But there is still substantial doubt.

Advertisement

What we can say for sure is that there is a mighty tug-of-war underway between the economic shocks transpiring in Europe (war and energy), China (property and COVID) and the US (a very hawkish Fed) versus the stable conditions currently prevailing in the Aussie economy that will eventually give way to RBA tightening.

It may seem an odd argument to make, that many Australian households should pray for a global economic shock to save them.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.