ANZ Capital’s chief economist, Shane Oliver, has warned that Australia’s housing market faces bigger risks this cycle because the 30-year structural fall in interest rates has come to an end:

“The previous cyclical downturns were all against the backdrop of a downtrend in interest rates”…

“So we’ve had a bit of a downswing, and then we’d get a new low in interest rates and prices would take off again, and before you know it, they’ve hit record highs, and anyone who got in had done spectacularly well.

“This time around there’s more uncertainty over it because we’re moving into a world of higher inflation, potentially higher interest rates on a longer-term basis, then that tailwind behind property prices may not be as strong as it once was.

“So we could see a longer downturn and if buyers can’t pay as much because of higher interest rates and elevated prices, then that will limit the upswing that can occur afterwards.”

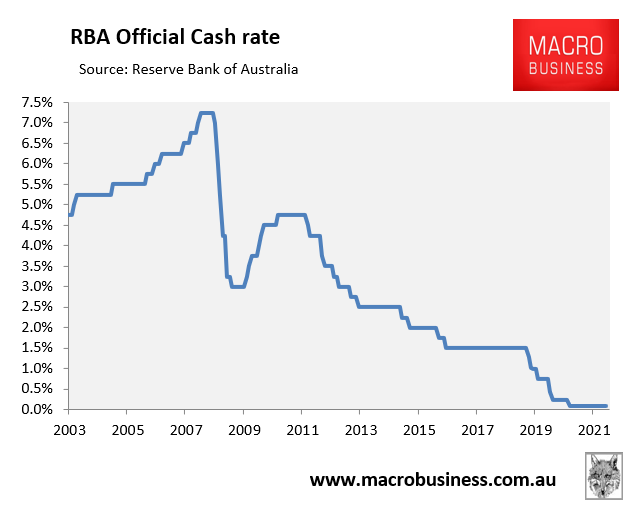

Dr Oliver is mostly right. With the RBA tanking the crash rate to a record low of 0.1%, there appears to be little prospect of rates going lower.

Interest rate at rock bottom

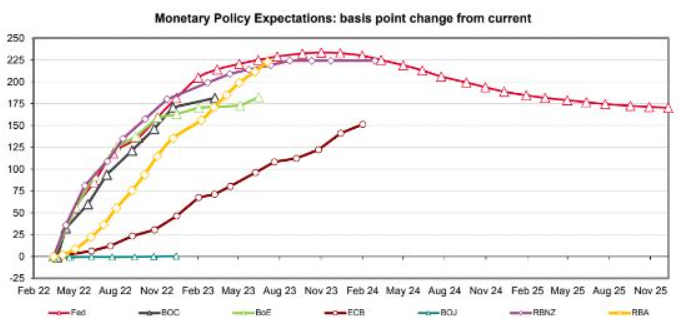

Economists (including Dr Oliver) are forecasting hefty rate rises from mid-year, whereas financial markets are now tipping a whopping 2.25% of increases in the RBA cash rate by mid 2023 (yellow line below):

Markets are tipping 2.25% worth of RBA rate hikes by mid-2023.

While I am nowhere near as bullish on rates, I do believe the RBA will begin hiking the cash rate late this year by up to 100 basis points. This alone would be enough to drive a significant housing correction.

That said, there is nothing stopping the RBA from driving interest rates even lower next cycle.

My prediction is that the RBA will implement negative interest rates mid decade following the pending housing correction.

The template has already been set by other central banks. For example, the European Central bank (ECB) began with 0.1% funding for banks in 2014. By 2016 the rate had turned negative (-0.4%) and subsequently fell to -1.0%, meaning the ECB is paying banks up to 1% for every dollar they lend. The Bank of Japan has done similar.

Denmark has already offered homeowners 20-year loans at a fixed interest rate of zero percent.

The precedent has been set. But we’ll have to wait through another housing/economic downturn first.

Then the RBA will likely end up following the pattern of the past 25 years and will attempt to stimulate the market/economy by lowering borrowing costs. Following other central banks into negative interest rates is the next logical step.