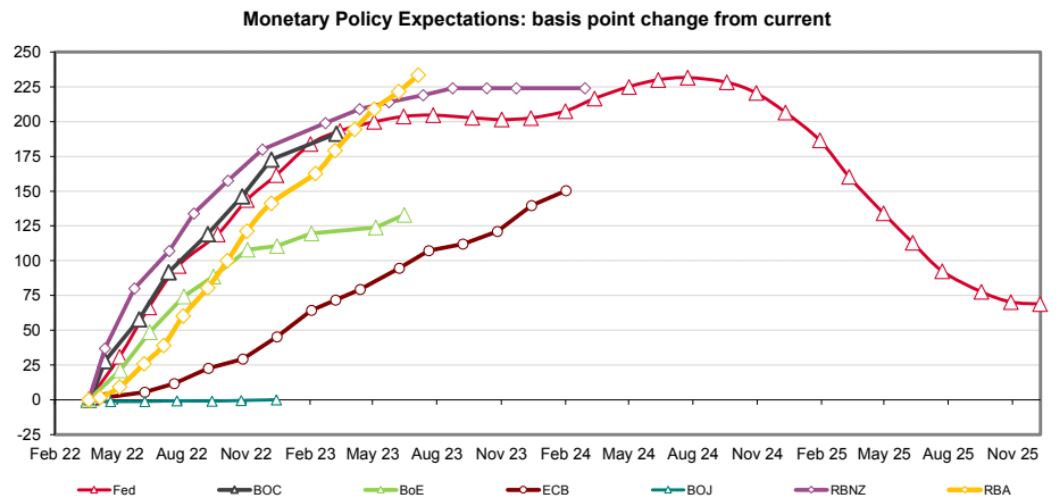

Australia is headed for the highest interest rates in the developed world. If you believe markets, that is, which are now pricing nearly eleven rate hikes by mid-2023. Westpac:

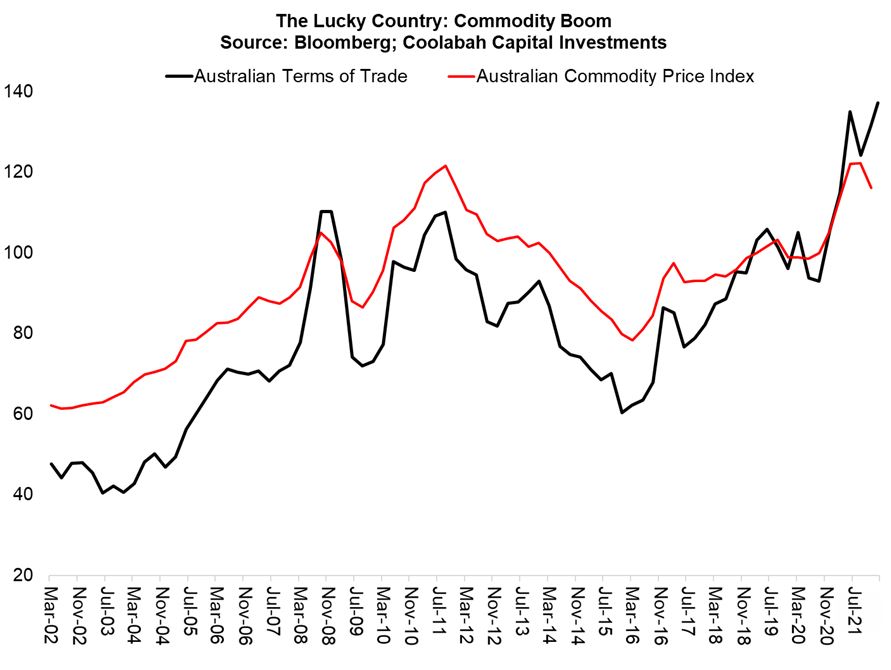

If one were to try to find rationality in this it would be in the commodities boom which has delivered a positive terms of trade shock. The Ukraine war has sent the entire commodities complex barmy and especially energy:

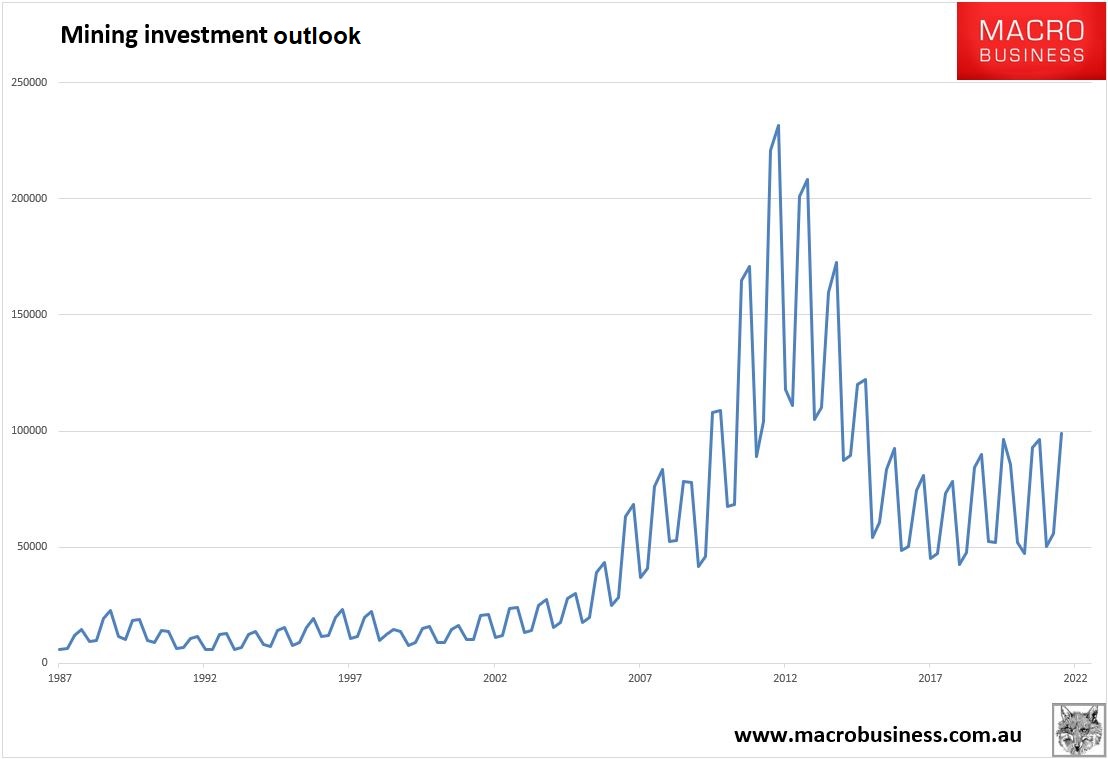

Normally, such price rises would trigger an inflationary follow-on of investment. We saw this after the GFC when the RBA did surprise many by lifting interest rates by 175bps.

However, while markets are gawking at these price blowoffs with slavering inflation expectations, they have neglected to understand a few significant points.

First, the transmission mechanisms from commodity prices to the real economy are significantly impaired versus the past:

- Coal will not see any or much investment follow through owing to climate change policy.

- LNG major projects are largely exhausted in Australia.

- Iron ore is in a glut with little new investment planned.

This means that despite high prices there is not much new investment on the books:

In consequence, most of the commodity income windfall will bypass wages.

Meanwhile, thanks to Australia’s corrupted gas management system, domestic utility prices will rise and actually cost households money.

The other two major commodity price transmission mechanisms to the real economy are also damaged. The stock market is falling and the budget is running huge deficits with little prospect of tax cuts.

In short, versus past commodity price booms, there will be significantly less reason for the RBA to “make room” for this commodity boom. It will not need to hike the cash rate to suppress household spending via crashing property prices so that business investment can expand without spiking inflation.

The commodity price boom will certainly be a net positive for the economy but nothing like 2010 and markets are still wrong on the degree and timing of RBA tightening.