Stuart Wemyss, an independent financial adviser, penned an article playing down concerns that rising interest rates could crash Australia’s property market.

According to Wemyss, “financial theory, which proves there is a strong relationship between interest rates and asset values, cannot be used to explain property price movements”. Wemyss also claims there is a “weak historic relationship between interest rates and property price growth” and claims he has “failed to observe a consistently strong relationship” since 1980.

Accordingly, the threat of rising mortgage rates does not pose a major threat to property prices:

Owner-occupier variable mortgage interest rates are about 2 per cent. If mortgage rates increase to 3 per cent, they are still very low by historical standards…

There is no doubt in my mind that some people have overpaid for property over the past couple of years. There have been some mind-boggling transactions…

When interest rates do eventually rise, it may further dampen buyer demand and market sentiment. This may culminate in one or two quarters of slightly negative growth, which would be considered immaterial in the context of last year’s growth rate.

But I think it is highly unlikely that prices will drop by 15-25 per cent as some of the more bearish commentators are now suggesting.

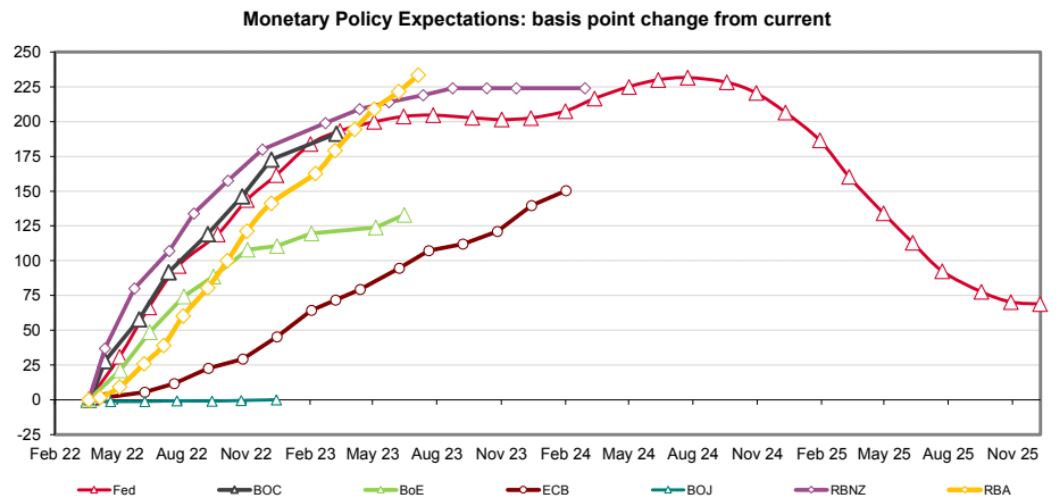

I agree with Wemyss that a 1% rise in mortgage rates would be unlikely to tank Australian house prices by 15% to 25%. The problem is that markets are now tipping a whopping 2.25% of RBA cash rate rises by mid-2023 (yellow line below):

Markets are tipping 2.25% of RBA rate hikes by mid-2023

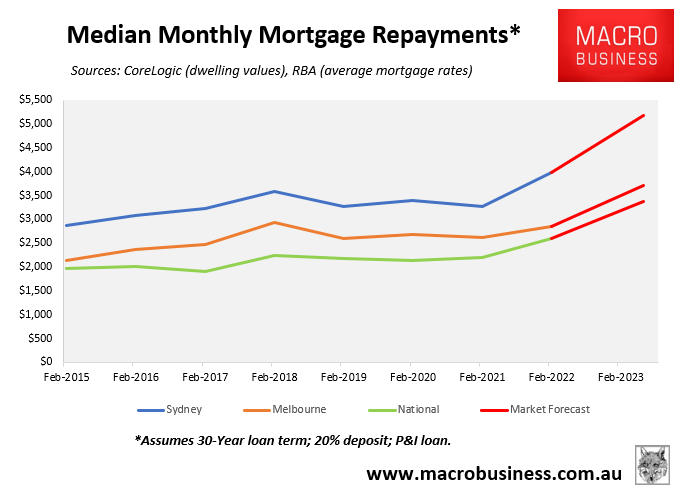

If mortgage rates rose by 2.25%, average monthly repayments on the median priced Australian home would soar by a whopping $781 (30%), with larger rises across Sydney ($1,198) and Melbourne ($858):

If mortgage rates rose by 2.25%, average monthly mortgage repayments would rise by $781

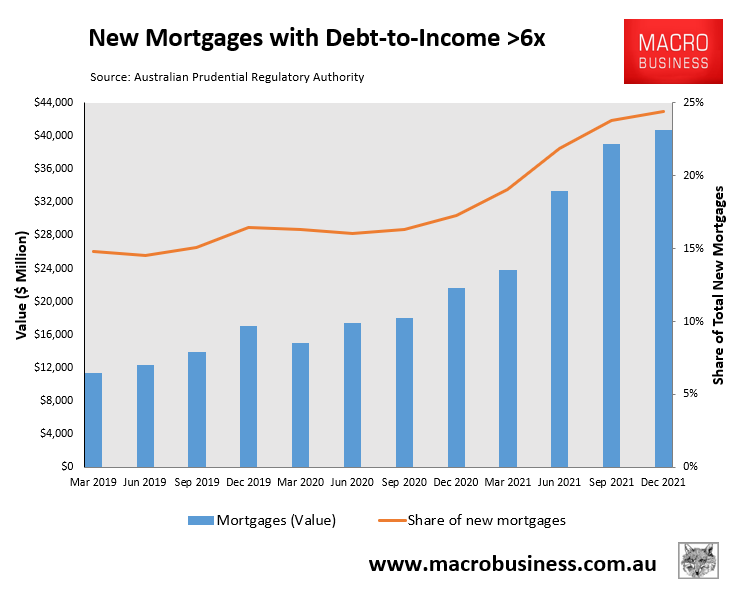

Such a large increase in mortgage repayments would put many recent home buyers under extreme stress, especially the 24% of buyers in 2021 that purchased with a debt-to-income ratio above 6 times:

Highly leveraged mortgage lending boomed in 2021

Many of these highly leveraged buyers are also likely to have purchased in areas that are car-dependent and more sensitive to the spike in petrol prices, which acts as a drain on household disposable income.

Finally, we should also remember that there are around 500,000 fixed-rate mortgages scheduled to expire by mid-2023, many of which were originated at rates below 2.5%. If variable rates were to rise by 2.25%, as predicted by the markets, then many of these fixed rate borrowers face a doubling of mortgage rates once their loan term expire.

The bottom line is that if the markets get its way, Australian house prices would likely crash.

Thankfully, the lever is in the hands of the RBA, not the markets. And the RBA is highly unlikely to raise rates as early, swiftly nor far as the market is predicting.