By Gareth Aird, head of Australian economics at CBA

Key Points:

- The 2022/23 Australian Budget is scheduled for release at 7.30pm (AEST) 29 March 2022.

- The Budget bottom line on an unchanged policy basis is significantly improved because of the much better performing economy and materially higher commodity prices.

- But a pre-election Budget means more stimulus is expected to be announced, which adds to the Budget balance. More stimulus also increases the risk that the RBA has to take monetary policy into contractionary territory.

- The Government is likely to retain a conservation slant with their forecasts, particularly the ones that drive the revenue side of the equation, which means the actual deficits over the next two years will likely end up lower than what will be forecast in the 2022/23 Budget.

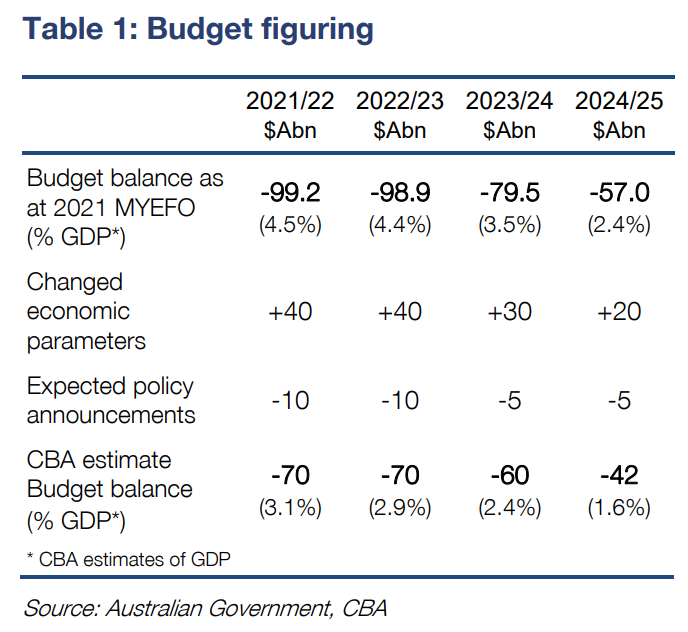

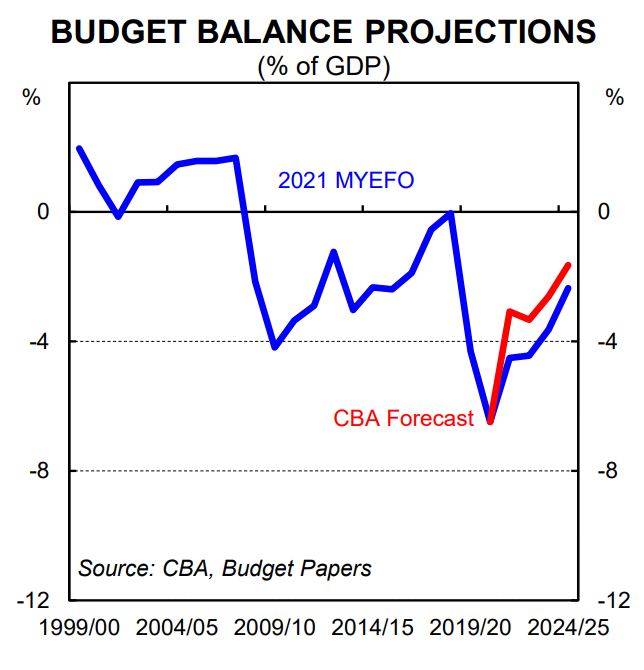

- Our point estimate that the Government will publish for the underlying cash deficit in 2022/23 is $A70bn (2.9% of GDP).

- Net debt is forecast to reach 31.4% of GDP in 2022/23.

Overview:

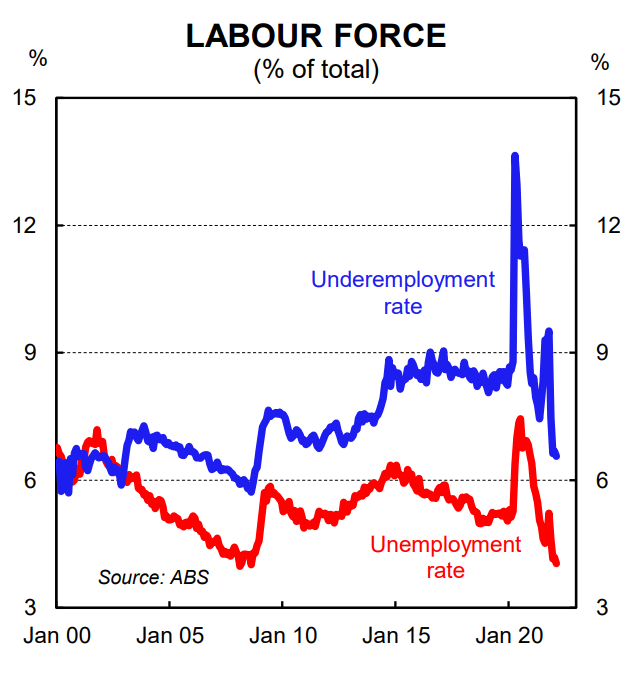

The backdrop for the March 2022 Budget comprises a pandemic that is largely behind us, a domestic economy that is firing on all cylinders, a 4.0% unemployment rate that is trending lower, rising inflation, surging commodity prices and a war in Ukraine. An election is also just around the corner, which makes the upcoming Budget a ‘pre-election Budget’.

History indicates pre-election Budgets generally contain new policies that add to demand in the economy. This year’s Budget should be no exception. But any such policies should be small in size and scale given the domestic economy is currently running red hot and the labour market is very tight. Put another way, there is no compelling economic case to ease fiscal settings in any material sense.

Of course the Budget is more than just an economic publication. It is also a political document that articulates the fiscal priorities and strategy of the Government.

Treasurer Josh Frydenberg last week indicated that the upcoming Budget will see the Government transition to the second phase of their fiscal strategy.

The first phase of the fiscal strategy supported employment and economic growth through the pandemic with temporary and targeted measures (e.g. JobKeeper and the Coronavirus Supplement). The second phase is a normalisation of fiscal settings. The Government will target a Budget position that stabilises and then reduces gross debt as a share of the economy. Net debt, on our figuring, continues to rise as a share of GDP, albeit very modestly.

There will be no policy pivot to austerity. According to the Treasurer the pace of fiscal consolidation will be ‘gradual and measured’. We believe this is the right approach as it enables the RBA to take monetary policy from a highly accommodative stance to a more neutral one.

The Budget is expected to contain additional expenditure on infrastructure, education, digital transformation and energy. Policies are also anticipated to be announced which will address what has been termed ‘cost-of-living pressures’.

Real wages growth is currently negative and that will be the rationale that underpins targeted policies to support low -to-middle income earners. But of course such policies are stimulatory in nature which supports demand and in turn pushes up the prices of goods and services.

Finally, the war in Ukraine means more spending on defence will be announced in the Budget. We will have more to say later in the week on what to look out for in the Budget from a policy perspective. This note focuses on the economy and the Budget, the key numbers we expect to see on Tuesday 29 March and the potential implications for monetary policy.

A better starting point

The Australian economy has performed better than the Government forecast in the 2021 Mid-Year Economic and Fiscal Outlook (MYEFO), which published 17 December 2021. The labour market in particular has posted much stronger numbers than Treasury forecast in the MYEFO. By way of comparison the unemployment rate was 4.0% in February, while the MYEFO forecast the unemployment rate to be 4.5% at mid-2022.

A better performing economy means an improved fiscal position. We put the starting point for this year’s Budget in a materially better position than expected at the time of the MYEFO in December 2021. Indeed the January 2022 monthly financial statement put the underlying cash balance $A13.2bn better off relative to MYEFO. This is an astounding result considering the January 2022 outcome comes just two months after MYEFO!

On our estimates, changes to the economic parameters that drive the fiscal forecasts will deliver an improvement of $A40bn in 2021/22 relative to MYEFO. But we suspect that Treasury will opt for a more conservative estimate of $A30bn (see Table 1).

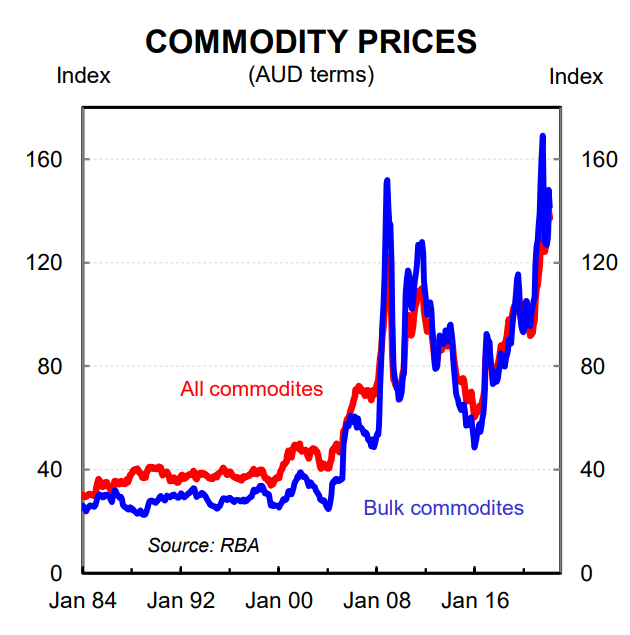

Nominal GDP growth (the tax base) is running well above expectations. Our forecasts have nominal GDP growing by 9% in 2021/22 compared to the MYEFO estimate of 6.5%.

The stronger than expected improvement in nominal GDP has been driven by a sharp rebound in production and employment, a strong lift in average weekly earnings and a surge in commodity prices. Our fiscal model indicates that tax receipts should be boosted by ~$A30bn in 2021/22 relative to what was expected in the MYEFO (indeed the monthly Government financial statistics indicate that revenue was tracking $A7.9bn higher in January 2022 relative to MYEFO). But we anticipate that the Government will take a more conservative approach to their revenue forecast and upgrade revenue by $A20bn –

$A25bn in 2021/22 relative to MYEFO (this will still be an extraordinarily large upgrade).

The expenditure side also looks in much better shape. The big decline in the unemployment rate relative to MYEFO means welfare payments will be a lot lower. Expenditure was tracking $A5.3bn lower in January 2022 relative to MYEFO.

Overall we estimate that the Budget will forecast a reduction in total expenditure due to changed economic parameters of $A10bn in 2021/22 relative to MYEFO.

Upgraded economic forecasts and a better starting point will lower the expenditure profile over the forward estimates on an unchanged policy basis. But some new policies in the Budget will of course add to the expenditure side of the ledger.

What will the Government forecast for 2022/23?

Economic forecasts drive the Budget projections which complicates the task for economists that need to estimate the Budget bottom line. Put another way, the job becomes to forecast what Treasury will forecast in the Budget. Indeed Treasury assumptions around commodity prices, wages, inflation and employment will have a large bearing on the forecast Budget deficit in 2022/23, notwithstanding any policy changes.

Our working assumption is that the Government will pencil in an improvement of $A40bn in the fiscal position in 2022/23 due to economic parameters (revenue up and expenditure down). And we have allowed $A10bn for expended policy announcements that subtract from the Budget bottom line in 2022/23. As such our point estimate for the Budget deficit in 2022/23 is $A70bn (2.9% of GDP).

The forecast Budget deficit will decline over the four year forward estimates period although we don’t put a lot of weight on the projections in the outer years given the economic and policy landscape can change significantly. Our expectation is that net debt as a share of GDP will hit 31.4% in 2022/23 (this compares with the MYEFO forecast of 34.7%).

Monetary policy implications

Overall we expect the March 2022 Budget to be supportive of demand in the economy. The improvement in the fiscal position will not be a result of policy changes, but rather it will be the result of an economy that is in much better shape than the Government forecast in the MYEFO.

We expect the RBA to commence normalising the cash rate in June 2022 and we do not expect anything in the upcoming Budget will shift that call.

Fiscal policy, however, will play a critical role in the tightening cycle to the extent that stimulatory fiscal measures mean a higher terminal rate, all else equal. Our base case sees the cash rate at 1.25% in Q1 23 and then on hold over the rest of 2023. However, if fiscal policy ends up more stimulatory than we anticipate and the Government injects a material amount of policy support to deal with ‘cost-of-living pressures’ we may need to upwardly revise our forecast profile for the cash rate in 2023.

Policies that seek to help households deal with higher consumer prices by adding to demand in the economy will put further upward pressure on prices, which in turn increases the probability that the RBA takes monetary policy into contractionary territory. We estimate the neutral cash rate to be 1.25% which means we believe contractionary monetary policy is a cash rate above that level.