By Gareth Aird, head of Australian economics at CBA:

Key Points:

- The war in Ukraine adds a significant layer of uncertainty to the global economic outlook, particularly in Europe.

- There is likely to be materially higher intraday volatility in financial markets in the near term.

- However the impact of Russia’s invasion of Ukraine on the Australian economy is expected to be minimal.

- Higher energy prices will boost export revenue and national income, while an expected increase in oil prices means higher petrol prices and further upward pressure on headline inflation.

- Measured consumer confidence may also be adversely affected by higher petrol prices, increased equity market volatility and a general apprehension, which is a natural response to war. But we do not expect this to change consumer behaviour.

- The overall picture for strong domestic demand in 2022 is unchanged and we remain optimistic on the Australian economic outlook.

- We have not made any changes to our central scenario for GDP, unemployment, wages or underlying inflation (near term headline inflation forecasts have been lifted a little).

- Our base case remains that the RBA will commence normalising the cash rate in June having concluded that, “inflation is sustainably within the target range” at the Board meeting.

The bigger picture

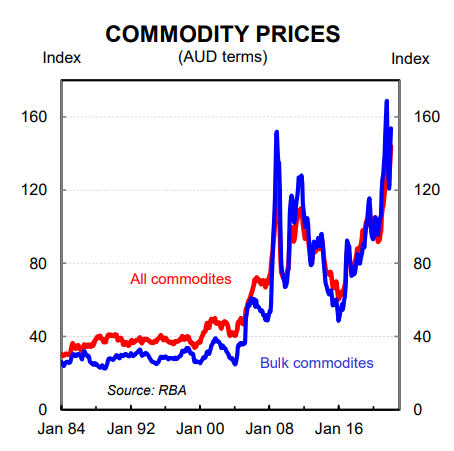

Russia’s invasion of Ukraine adds a significant layer of uncertainty to the global economic outlook, particularly in Europe. The wide range of potential geopolitical, economic and financial implications of the war have rattled financial markets. Commodity prices in particular have been incredibly volatile over the past week given Russia is a major supplier of thermal energy (oil, gas and coal).

Russia’s invasion of Ukraine comes at a time when inflation is high in many western countries which complicates the path of policy normalisation for some central banks. This increases the likelihood that there will be significant intraday volatility in financial markets over the period ahead. Put another way, markets will have a lot to contend with.

However, it is important to distinguish between financial market volatility and the real economy. Australia’s trading relationship with Russia and Ukraine is negligible. And it is our expectation that the Australian economy will largely be insulated from the war provided the major military powers in Europe and the US do not fight Russia in Ukraine or elsewhere (that is our base case).

We say largely insulated as there will be some repercussions from the invasion for the Australian economy. These are not significant enough for us to make any changes to our central scenario for GDP, unemployment, wages or underlying inflation, which means we retain our call for the RBA to commence normalising the cash rate in June. But they warrant discussion.

Oil prices were rising steadily before the invasion

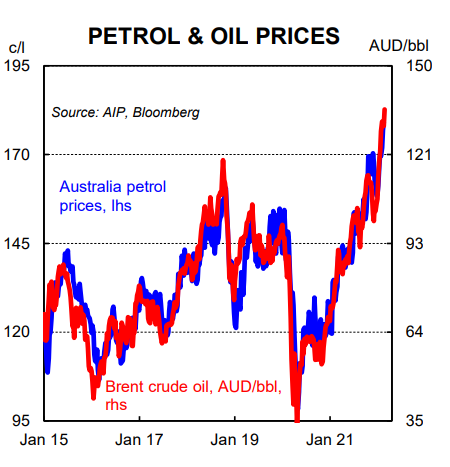

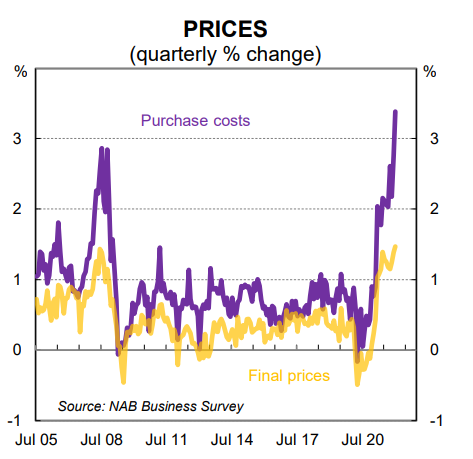

Prior to Russia’s invasion of Ukraine petrol prices had been on a steady increase in Australia due to the rise in global oil prices. For context, prices at the bowser lifted by ~15% over the six months to mid-February on rising global demand and some supply side issues. The lift in petrol prices contributed 0.3ppts to the quarterly increase in headline inflation in Q3 21 and 0.2ppts in Q4 21.

Automotive fuel (i.e. petrol) accounts for ~3¼% of consumer spending. But the share of spend on petrol for each individual household varies greatly. Lower income households on average spend a much greater proportion of the household budget on petrol compared to higher income households. A lift in petrol prices therefore disproportionately negatively impacts households at the lower income end of the spectrum.

Petrol has trended down over time as a share of total consumer spending. Notwithstanding, it’s still a material share of many households expenditure and significant increases in the price of petrol are a de-facto tax for households.

Over the past six months there is no evidence that rising petrol prices have weighed on total household expenditure. Aggregate spending has risen strongly in line with the broader improvement in the economy and labour market. A big surge in household income due to government transfer payments, tax cuts and an acceleration in wages growth has left households better able to cope with the lift in petrol prices.

Oil prices will rise further

Russia is responsible for ~10% of global oil production. Russia’s invasion of Ukraine and potential sanctions on Russian exports means further rises in the oil price and by extension petrol prices are likely over coming months.

Our hard commodities strategist Vivek Dhar expects Brent oil to average ~$US110/bbl over the next six months (the peak in prices could be a lot higher than this). On an unchanged AUD/USD, an average Brent price of $US110/bbl over six months would see domestic petrol prices average ~$A1.95p/l. This would add a further 0.5ppts to headline inflation over the period and we have upwardly adjusted our forecast profile accordingly (we now expect headline inflation to reach 4.4%/yr at mid-2022).

However, we have not made any modifications to our forecast profile for underlying inflation (we expect core inflation to be 3¾% by mid-2022 and to broadly hold there over H2 22). Higher oil prices due to Russia’s invasion of Ukraine may result in prices rising further for other goods and services where oil is an input in production. But our central scenario for underlying inflation already incorporates stronger input costs and output prices due to the steady increase in oil prices prior to the war. As such, at this stage we consider Russia’s invasion of Ukraine an upside risk to our base case for underlying inflation.

We have not adjusted our profile for real household expenditure or the unemployment rate. Some households at the margin will cut back on discretionary expenditure due to a further increase in petrol prices. However, we do not expect this to be significant enough to warrant a change in our assessment for the path of consumer expenditure over 2022. By extension our forecasts for the labour market are unchanged.

The level of household savings accumulated over the pandemic is extraordinary (~12% of GDP) and this will provide a tailwind on spending over the next two years. The bigger picture remains intact.

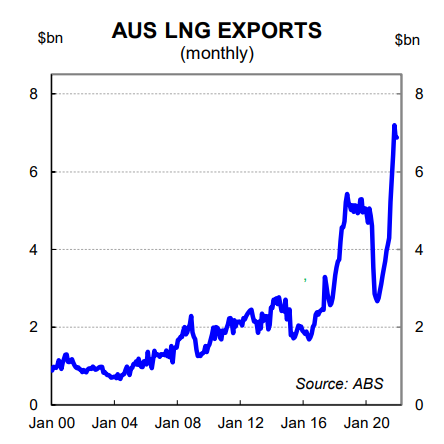

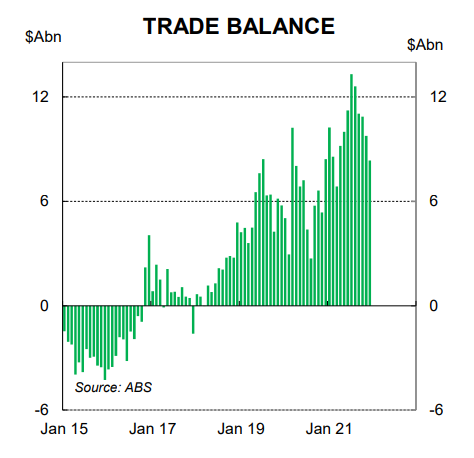

Higher energy prices means a bigger trade surplus and stronger nominal GDP growth

Rising oil prices will flow through to higher gas prices and this will be beneficial for Australian gas producers. LNG is Australia’s second largest export and in 2016 Australia became a net fuel exporter. This means that a lift in oil and gas prices boosts the trade balance, terms of trade and nominal GDP, all else equal.

The pass through from higher export receipts to the broader economy is less direct, however, than the impact of higher oil prices on consumers. It takes time for profits to be paid to shareholders and there is a high level of foreign ownership in Australian’s LNG sector.

Notwithstanding, domestic shareholders of Australia’s gas exporters will benefit from a lift in energy prices. And the budget bottom line also improves from higher export prices through the company taxes and royalties channel.

Our RBA call is unchanged

The RBA will commence normalising the cash rate when the Board conclude that “inflation is sustainably in the target range.”

Based on our expectation that Europe and the US do not fight Russia in Ukraine we retain our call that the first increase in the cash rate will be in June 2022. This risk is skewed towards a later date for lift off with August being the next most likely month.

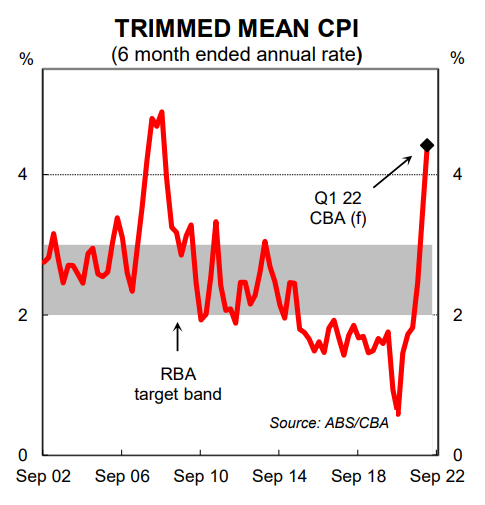

We expect a red hot Q1 22 CPI that will take the underlying rate of inflation to ~3.4% (4.5% on a six month annualised basis). We believe that an underlying inflation print in line with our forecasts means that the RBA will not need a further CPI report to conclude that inflation is “sustainably within the target range”. The RBA will simply need to be satisfied that wages growth is moving towards the desired levels and the economy is at full employment.

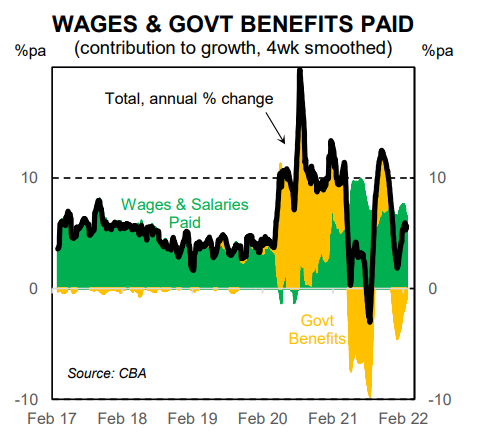

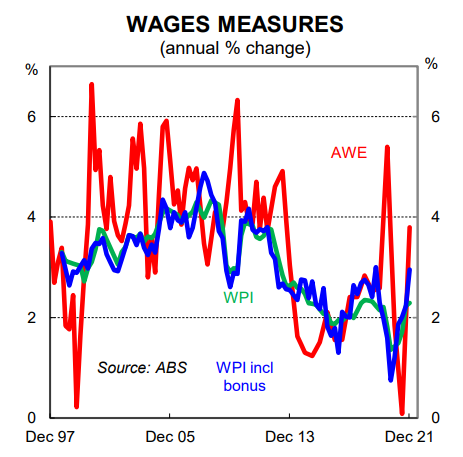

Wages data published last week indicated that wages pressures were intensifying towards the end of 2021. The 0.7% increase in the wage price index (WPI) over Q4 21 was the strongest quarterly increase in the WPI since March 2014. And according to the ABS, “the proportion of pay rises reported over the December quarter was higher than usually seen”.

The WPI including bonuses picked up considerably over Q4 21 and the annual rate lifted to 2.8%. Average weekly total earnings rose by a strong 3.8% over the year in November 2021.

The Q1 22 WPI, due 18 May, should show a further and more significant acceleration in wages growth. The unemployment rate printed at both 4.2% in December 21 and January 22 which is materially lower than the 4.7% average unemployment rate over the three months to November 21. At this stage we expect the Q1 22 WPI to increase by 0.8%/qtr and the risk sits with a stronger outcome.

Inflation data in line with our forecast as well as a strong Q1 22 WPI and an unemployment rate that is expected to have a 3-handle on it should be sufficient evidence for the RBA to conclude “inflation is sustainably in the target range” at the June Board meeting. As such, it will be appropriate to start a tightening cycle.

In summary, we think the impact of Russia’s invasion of Ukraine on the Australian economy is likely to be minimal. As such, we leave our forecasts unchanged for GDP, unemployment and wages. And we retain our RBA call.