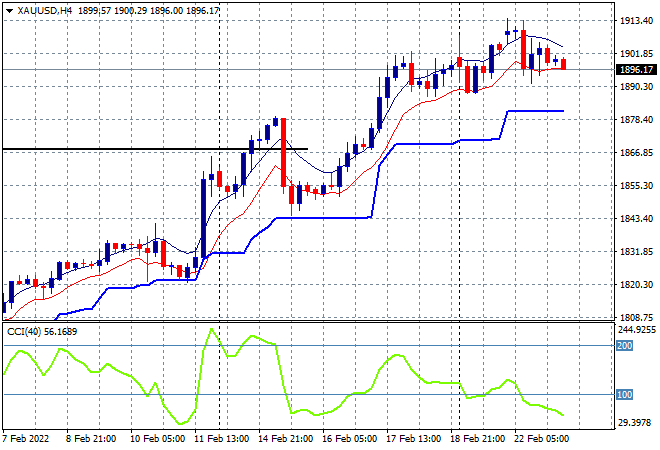

A slightly calmer day across stock markets in Asia today as the deep breath before the plunge maybe drawing risk into a trap here as Russia takes the next step in Ukraine. Energy prices remain elevated as Brent approaches $100USD per barrel while currency markets are still seeing the usual move towards safe havens, although the Kiwi spiked today on more RBNZ rate rise scuttlebutt, dragging the Aussie along with it. Bitcoin is failing to stabilise again, currently just below the $38K level while gold is pulling back below the $1900USD per ounce level as momentum inverts from an extremely overbought position:

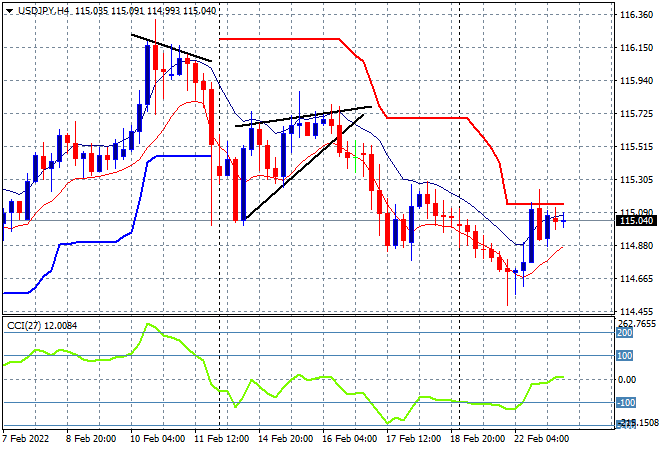

Mainland Chinese shares are seeing a boost straight after the lunch break with the Shanghai Composite climbing 0.7% to 3483 points while the Hang Seng Index is trying to make a comeback, up 0.8% to 23714 points. Japanese stock markets are having the day off for a holiday with light trading in Yen seeing the USDJPY pair remaining steady here just above the 115 handle:

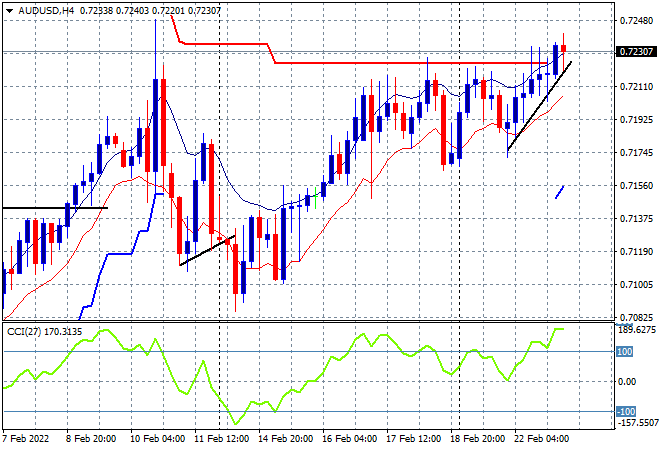

Australian stocks did a good job of filling in the short covering with the ASX200 gaining 0.6% to finish at 7205 points while the Australian dollar had burst again above the 72 handle, pushed up by solid wages data and dragged along with the Kiwi as it brushes aside a lot of resistance overhead and makes a new weekly high against USD:

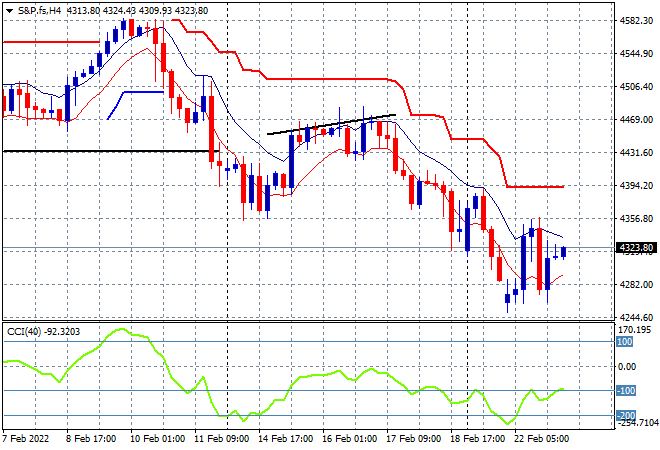

Eurostoxx and Wall Street futures are trying to get out of their rut here with the S&P500 four hourly chart showing price looking extremely oversold here as it tries to find a bottom somewhat below the previous support/resistance zone after crumbling below the key psychological 4400 point level:

The economic calendar continues with the latest German consumer confidence report, than Euro-wide inflation for January, followed up by the latest Redbook in the US.