Goldman with the note. Not sounding so bullish suddenly:

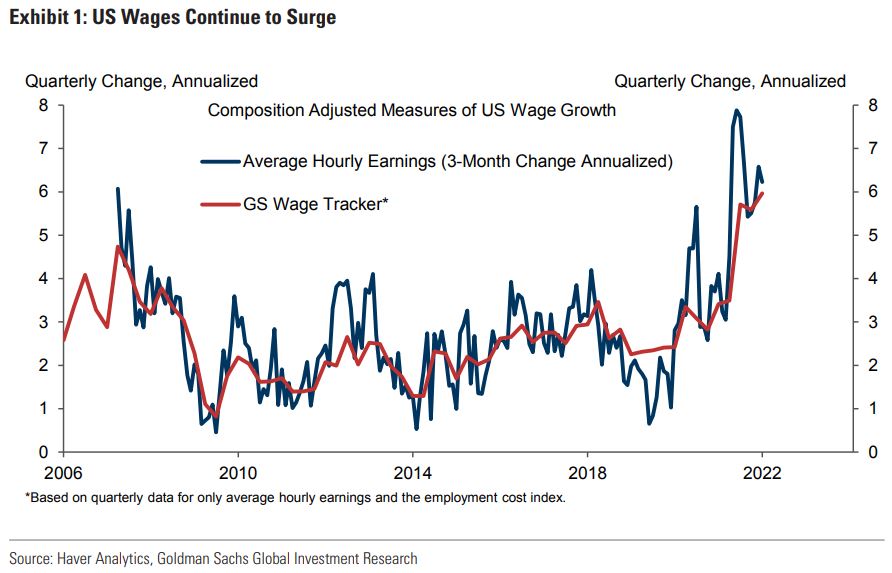

1. The most important number in the US employment report for January was not the surprising 467k increase in nonfarm payrolls, but the 0.7% increase in average hourly earnings. It reinforces the message from our composition-adjusted wage tracker, which has accelerated to a 6% annualized rate over the past 2-3 quarters. With core PCE inflation running at about a 5% rate over the past 3, 6 and 12 months, this raises the question whether we are already in the middle of a wage-price spiral that will need to be broken by aggressive Fed rate hikes and a large tightening in financial conditions.

2. So far, we don’t see a spiral where wage and price inflation feed on each other while expectations become unanchored to the high side. Our wage survey leading indicator remains consistent with just under 4% growth, as does a narrower set of business surveys that ask specifically about compensation budgets for 2022. And while short-term inflation expectations have surged, longer-term forward inflation expectations—whether measured via bond yields, forecaster surveys, or household surveys—remain well anchored. Taken together, these observations suggest that firms, households, and market participants still expect the current wage and price surge to level off as the economy emerges more fully from the pandemic.