By Gareth Aird, head of Australian economics at CBA:

Key Points:

- ABS data, private surveys and our internal data that captures salaries paid into CBA bank accounts indicates that wages growth has further accelerated over the final quarter in 2021 and the early part of 2022.

- An acceleration in wages growth is the natural response to a tight labour market.

- We expect the Q4 21 wage price index to increase by 0.8%/qtr which would take the annual rate of wages growth to 2.5%.

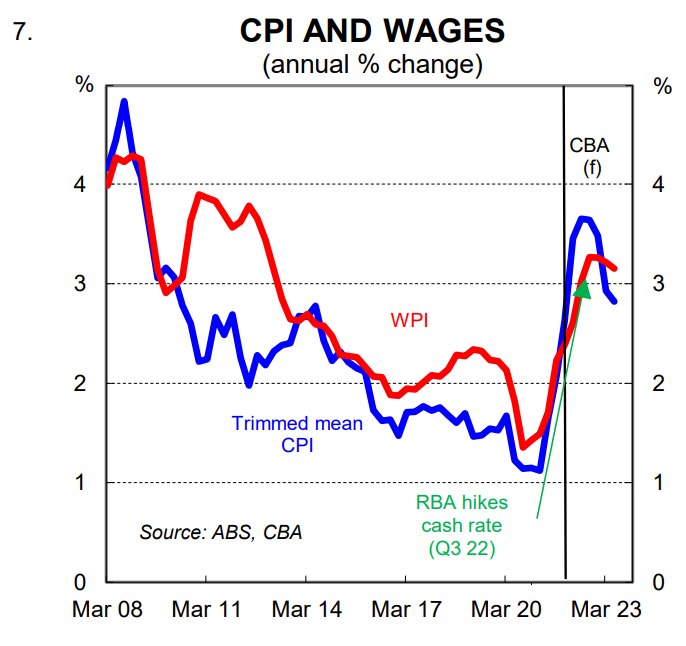

- We forecast annual wages growth to be 3% at mid-2022 which coupled with our expectation that underlying inflation will be at least 3½% by mid-2022 means our base case remains that the RBA will pull the rate hike trigger in August 2022 (note that we expect the six month annualised pace of wages growth to be 3¼% in Q1 22).

Overview

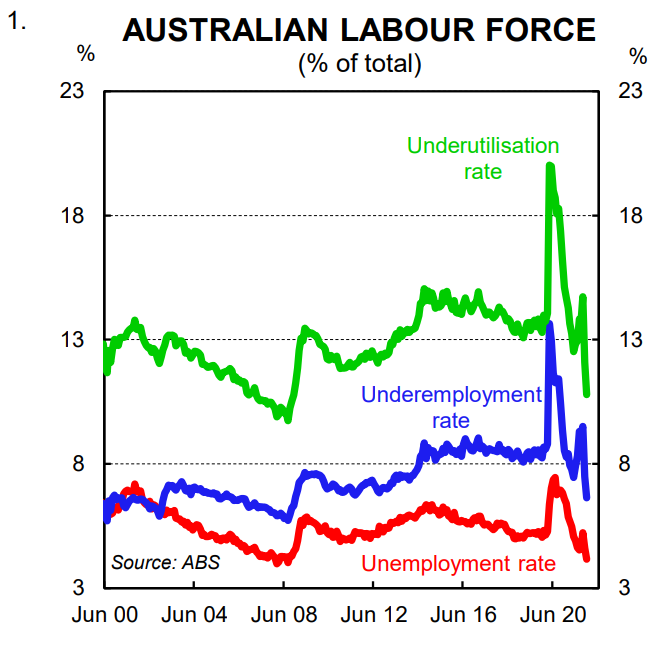

The Australian labour market is incredibly tight. The December labour force survey indicates the unemployment rate ended 2021 at 4.2% (its lowest level since 2008). Underemployment has also fallen sharply and the underemployment rate dropped from 7.5% to 6.6% in December; also its lowest rate since 2008.

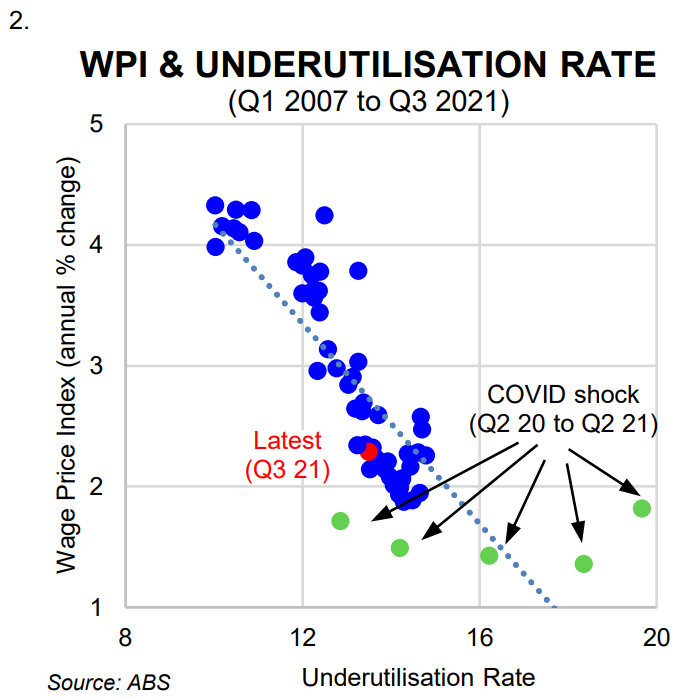

A tight labour market is a necessary condition for higher wages growth in a largely deregulated labour market (as is the case in Australia). Recent history indicates that the strongest relationship between wages growth and labour market slack lies with the wage price index (WPI) and the underutilisation rate (defined as the sum of the unemployment and underemployment rates). Put another way, wages outcomes have been most closely correlated with the broadest measure of labour market slack, the underutilisation rate, rather than

the unemployment rate (chart 2).

The level of the underutilisation rate in Australia suggests that wages pressures should emerge quickly. But after many years of soft wages growth the RBA has stated that elements of Australia’s wage setting process create inertia in aggregate wage outcomes. As such, they expect wage growth to pick up “only gradually”.

We understand the RBA’s argument around inertia and believe that it goes a fair way to explaining why wage rises so far over the pandemic have been relatively modest considering the level of job vacancies and skill shortages in the economy. But inertia has a shelf life. And a lot of workers will be able to leave a job for higher pay somewhere else if the opportunity presents itself (clearly not all workers will be in that position).

The current tightness in the labour market coupled with strong forward looking indicators of labour demand point to an acceleration in wages growth that would be stronger than the RBA’s expectations. Indeed we believe that there is a growing body of evidence that indicates wage rises are occurring at a faster pace than the RBA has forecast. We cover the key data below.

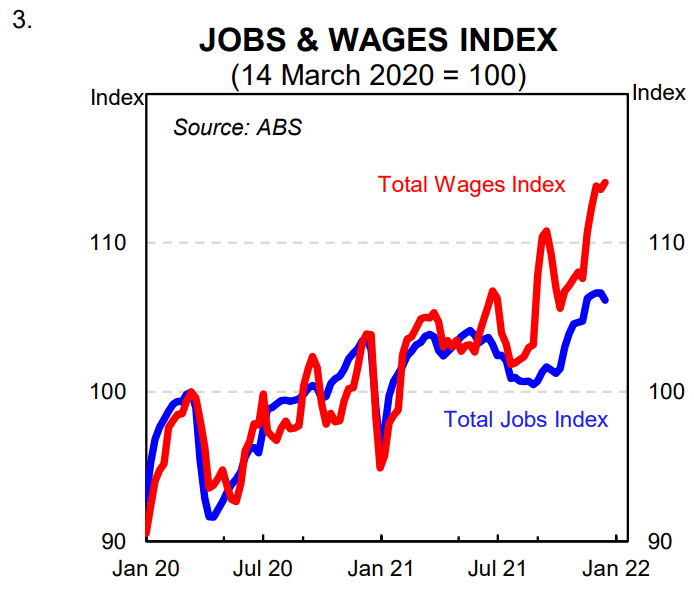

ABS payrolls

The ABS payrolls are essentially an experimental series that our official statistician brought in during the pandemic. The data is published in original terms which means there are big seasonal swings in the data. Nonetheless it has been a useful series to better understand the swings in the labour market over the pandemic.

The payrolls series measures both the number of payrolls jobs as well as reported wages associated with each payroll job (gross amounts prior to taxation and deductions).

For the bulk of the pandemic the payrolls jobs and payrolls wages indexes have moved broadly together. But since September 2021 the wages index has accelerated at a faster pace than the total jobs index and a significant spread has opened up between the two series (chart 3). To be clear, the wages index is not a pure measure of wages inflation. It is impacted by hours worked, compositional shifts in the labour market and bonus/one off payments. Notwithstanding, it does suggest that wages inflation is likely to have accelerated materially over Q4 21.

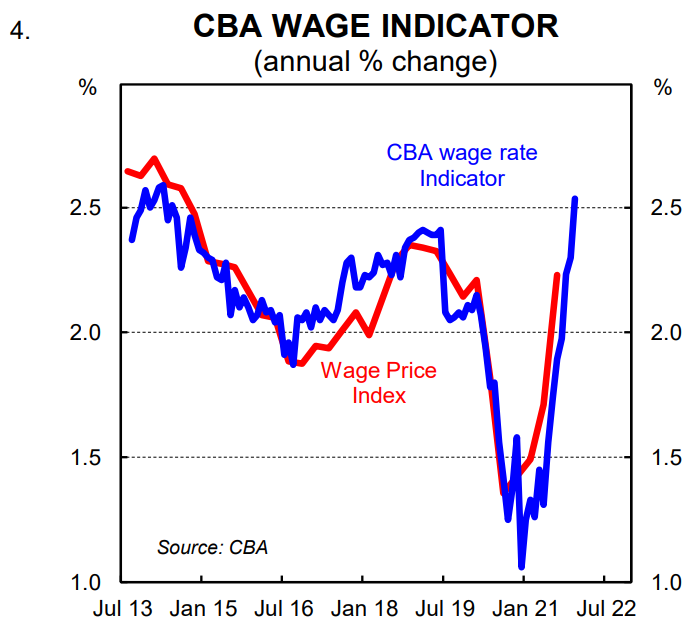

CBA internal data

We use quite a sophisticated methodology based on our internal data on wages and salaries paid into CBA bank accounts to model the WPI. More specifically, we apply a strict criteria to the accounts we include in our sample each month to account for people moving jobs, receiving a bonus or modifying hours worked in any material sense. We also take into account changes in tax rates or levies.

The upshot is that our real time wage price model, which is based exclusively on wages and salary payments into CBA bank accounts, very accurately tracks the WPI (chart 4).

Our most recent data is to December 2021. It suggests that wages inflation accelerated by ~0.8% over Q4 21 to take the annual rate to 2.5%. Such an outcome would be quite a bit stronger than the RBA’s forecast from the November Statement on Monetary Policy (SMP) for the WPI to be 2¼%/yr at end-2021 (note we receive the February 2022 SMP on Friday) It is worth noting that the RBA has had to make upward revisions to their wages forecasts over the pandemic to account for actual outcomes being stronger than they expected. For example in the May 2021 SMP the RBA forecast the WPI to be just 1¾% at end-2021.

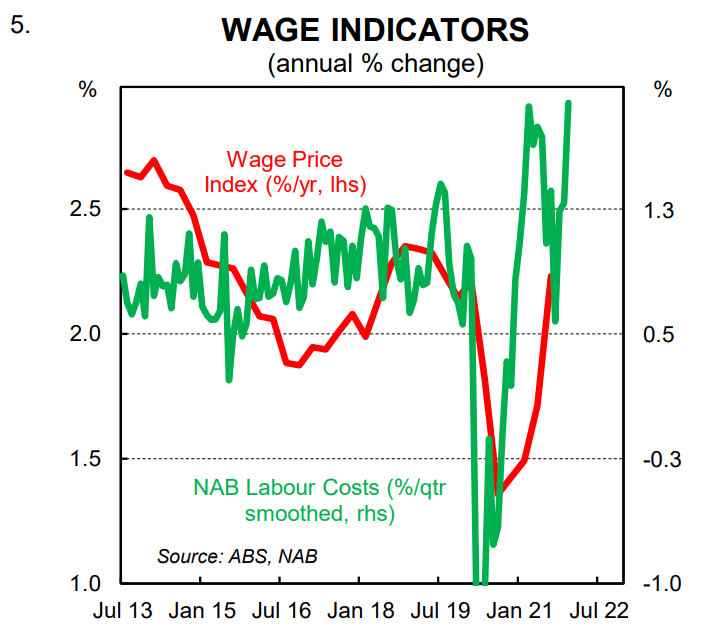

NAB Business Survey

Labour costs are measured in the NAB monthly business survey. The measure reflects changes in a businesses’ overall wage bill (i.e. it includes both employment growth and wage growth). It is therefore note a pure measure of wages inflation. But it does have a reasonably good correlation with the WPI (chart 5). The strong increase in labour costs provides further evidence, we believe, that wages growth is accelerating even when we account for the strong lift in employment more recently.

Markit PMIs

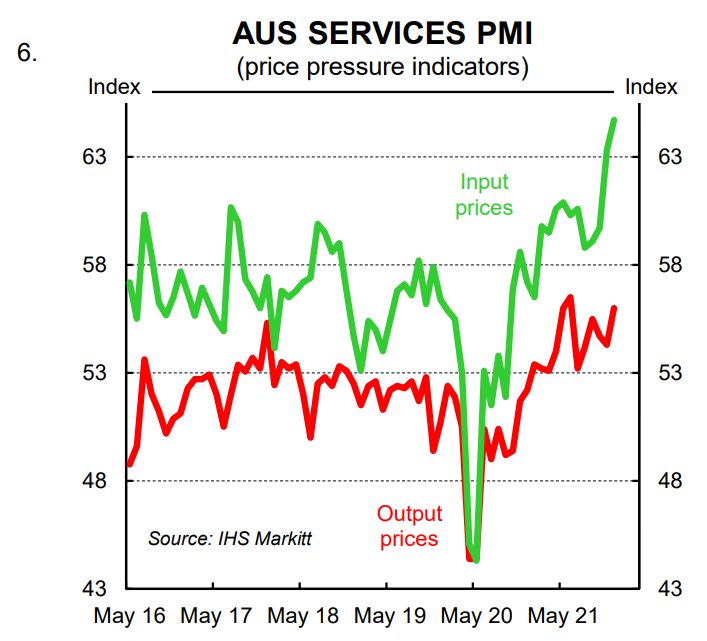

The Markit PMIs don’t have a long history in Australia (the series only dates back to 2016). But they are part of a global suite of PMIs that have a much longer history and have proven to be very useful indicators when tracking the pulse of private economic activity, which includes prices momentum.

The PMIs do not directly observe wages or labour costs. But they measure input costs. In the services sector, wages are the key input cost for a business. Input costs in the Flash Services PMI climbed to a record high in January 2022 (chart 6). This surge points to an increase in the cost of labour.

Conclusion and RBA call

There is a growing body of evidence that indicates wages growth has accelerated. The latest official read on wages (the Q3 21 WPI) is very dated. Indeed the WPI is picking up wages inflation at the mid-point of the quarter. So in the case of the Q3 21 WPI it is effectively a read on wages inflation at August 2021; that is almost six months ago!

A lot has changed since then and the labour market has tightened materially. Our forecast profile for wages growth and inflation means our call for the RBA to commence normalising the cash rate in August 2022 (give or take a month) remains very much on course.

We have pencilled in a first increase of 15bp in August 2022, which would take the cash rate to 0.25%. We expect that to be followed by an increase of 25bp in September 2022. We have three further 25bp hikes in Q4 22, Q1 23 and Q2 23 that take the cash rate to 1.25% (our estimate of neutral).

Overall we expect it to be a shallow and gradual tightening cycle given the elevated level of household indebtedness. It is possible the RBA needs to take the policy rate from a neutral setting to a contractionary one in 2023 if the RBA needs to put downward pressure on wages and consumer inflation (this would result in a terminal rate above 1.25%). That is a risk, however, and not our central scenario.