Westpac with the note:

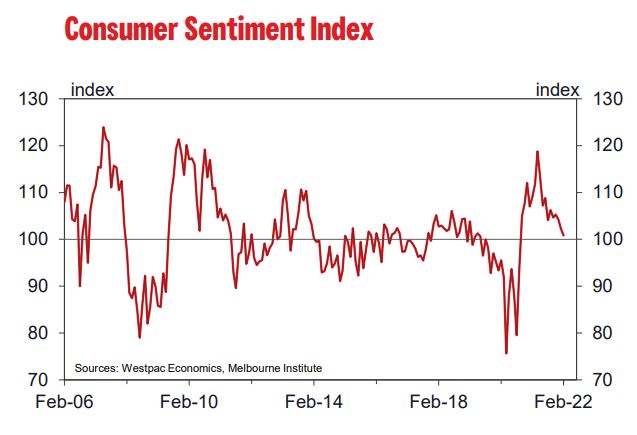

The Westpac-Melbourne Institute Index of Consumer Sentiment fell by 1.3% to 100.8 in February from 102.2 in January.

Given that the health disruptions from the Omicron variant have eased and the labour market has strengthened it is surprising that we did not see some improvement in the Index in February.

Virus developments do look to have seen an improved assessment of the economy, as measured by the components of the Index that relate to the economic outlook, and confidence in the jobs market (see below). The ‘economy, next 12 months’ sub-index increased by 2.4% and the ‘economy, next 5 years’ sub-index was up by 1.5%.

However, this was more than offset by increased pressure on family finances. Both components of the Index that measure respondents’ assessments of their finances deteriorated. The ‘finances vs a year ago’ sub-index slumped by 9.2% (more than reversing the surprise 7.5% lift in January) while the ‘finances, next 12 months’ sub-index fell by 1.5% to be down by 4.3% since December.

The most likely explanations for these elevated pressures on finances relate to: Omicron-related disruptions to activity and earnings at the start of the year; the rising cost of living; and the prospect of rising interest rates.

Petrol prices have lifted by 8% over the last month and 15% over the last two months. Recent CPI updates also show a broader lift in prices since mid-2021 that looks to have continued into early 2022, exacerbated by the collision of virus-related supply chain disruptions with surging demand.

Housing and building-related costs have seen particularly strong rises as well.

The sub-group detail shows a notably sharper weakening in ‘finances vs a year ago’ indexes for those in younger age groups, renters, retirees, and those on very low incomes. All of these sub-groups tend to be more sensitive to increases in the cost of living, particularly for ‘staples’ such as food and transport.

Meanwhile, there is a firming expectation amongst consumers that interest rates are set to rise. The proportion of respondents expecting an increase in mortgage rates over the next 12 months lifted from 55% in January to 66% in February with over one in four consumers now expecting rates to rise by more than a percentage point. This is the most pessimistic consumers have been about the interest rate outlook since August 2011, although on that occasion, rate hikes actually failed to materialise. Note that we now ask this question every month but prior to 2022 it was run twice a year, in February and August. Those surveyed after the RBA decision and the Governor’s speech mid-week were even more disposed to expect rate rises.

Consumers were clearly encouraged by the stunning fall in the official unemployment rate, from 4.6% in November to 4.2% in December. The Westpac Melbourne Institute Unemployment Expectations Index fell 8.7% to 102.8 (recall that lower reads mean more consumers expect the unemployment rate to fall over the next 12 months). This is the second lowest, i.e. best, read since February 2011, only outdone by last November’s exceptional reading of 95.3.

Housing-related sentiment had a mixed month, with price expectations lifting but buyer sentiment slipping to remain near fourteen-year lows.

After falling steadily to be down 9.2% over the previous four months, the Westpac Melbourne Institute Index of House Price Expectations recovered by 8.7% in February. The gain was across all the major states with Victoria recording a particularly strong 19% gain, NSW up 4.4%; Queensland up 7.1%; and Western Australia up 3.6%. All state indexes remain at relatively high levels meaning that a strong majority of Australians still expect prices to rise over the next year.

The results emphasise the sheer resilience of Australia’s housing market. Despite consumers being unnerved by higher cost of living and rising interest rates, their confidence in house prices remains solid.

However, the mix of price and interest rate rises is clearly less appealing from a buyer’s perspective. The ‘time to buy a dwelling’ index, which is heavily influenced by actual and prospective affordability, fell 2.4% to be 36% below its peak in November 2020. All major states recorded falls, reflecting the common expectation that rising prices and interest rate increases will see a further deterioration in affordability. Westpac does not expect the first rate hike by the RBA until August and it will be very interesting to observe how resilient this surprising recovery in confidence will be in the lead up to the first move.

The Reserve Bank Board next meets on March 1. With the Board having decided in February to cease its bond purchase program and the other support measures of Yield Curve Control and the Term Funding Facility having already been curtailed, policy will revert to interest rates.

At one point markets had been toying with the idea of a rate hike as early as March. They have now backed off but still expect a 25bp increase by June.

On January 20, following the January Consumer Sentiment report, Westpac brought forward its timing for the first rate increase to August. We expect that the Bank’s conditions for assessing that inflation is sustainably in the target range will be achieved by the time of the August meeting. Nevertheless, each meeting will be watched closely as the beginning of the tightening cycle nears.