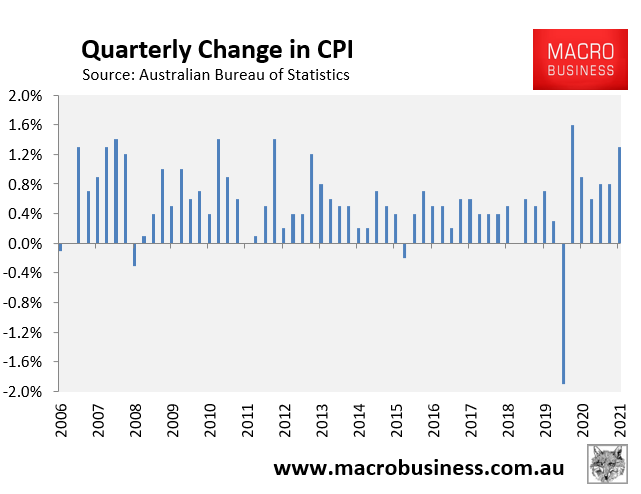

As already reported, Australia’s Consumer Price Index (CPI) came in hot at 1.3% in the December quarter – smashing market expectations of a 1.0% rise:

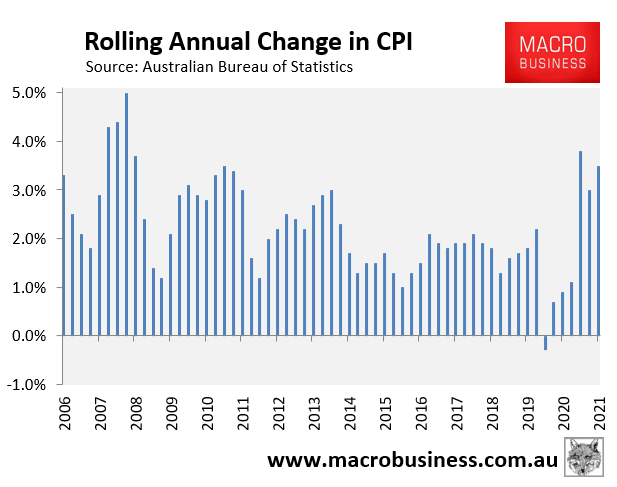

Annual CPI rose to 3.5%, smashing expectations of a 3.0% rise:

Advertisement

Looking at the major components, you can see that the rise in quarterly inflation was driven by Transport (petrol prices) followed by Clothing & footwear and housing (new dwellings):