It is clear that the stock market stress I have been warning about for three months is mounting. Some on Wall St get it while others want to fight it right to the cliff’s edge. Permabull Goldman is the latter:

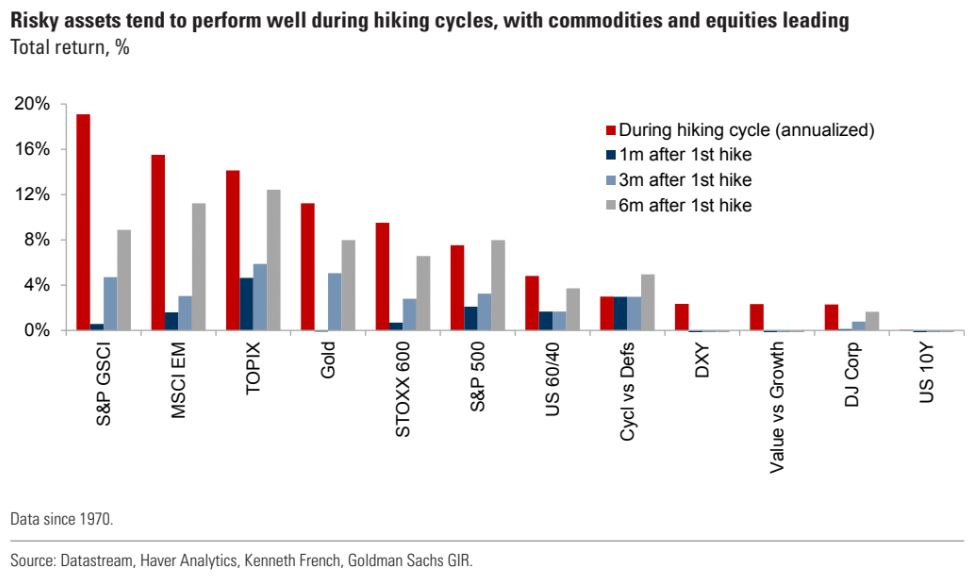

Although a sharp jump in rates driven by concerns over a more hawkish Fed has led to a sizable drawdown in long duration assets in recent days, we remain pro-risk in our asset allocation this year, and recommend overweights in equities and commodities, given continued strong global growth and low real yields. Indeed, we find that risky assets actually tend to perform well during Fed hiking cycles, with commodities and equities leading, as our chart of the week shows. We note, however, that since the 1990s, markets have tended to be less risk-on in the initial phase surrounding liftoff, with much of the positive performance coming in the subsequent 12-24 months as markets eventually took the gradual rise in rates in stride. In particular, US equities usually exhibit above-average returns when 5-year ahead fed funds expectations rise, with cyclical and Value stocks performing the best. That said, while Growth stocks have suffered during the recent rates moves, we recommend investors balance their exposure between Growth and Value given our expectation for only a gradual further rise in rates from a low level and slowing economic growth in 2022.

Fine. But quant models of past cycles do not guarantee a repeat in this one. There are some unique features to the COVID cycle. Most pointedly, owing to atypically extreme stimulus, equities and commodities are very overvalued earlier in the cycle and inflation is stronger.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.