Westpac chief economist Bill Evans is now forecasting that the RBA will begin lifting the cash rate from August. My view is that the RBA won’t start lifting rates until wage growth breaches 3%, which depends in part on the speed at which mass immigration is rebooted:

In this note we set out some changes to our interest rate forecasts.

In addition, we also assess the impact on economic growth of the omicron variant.

Omicron is forecast to have its major impact on the economy in January through a contraction in consumer spending.

Thereafter we expect a solid bounce back in the later stages of the March quarter and in the June and September quarters.

Westpac Economics is now forecasting growth for 2021 and 2022 of 3.2% and 5.5%, respectively. That is revised from the pre-omicron profile of 2.8% and 6.4%, with a net reduction of 0.5%.

We do not see that correction as having a significant impact on jobs growth or wages/inflation.

Changes to the outlook for interest rates

We have not changed our call for the first hike in the overnight cash rate by the RBA since June 2021 when we were early to challenge the “not till 2024” consensus.

Our “target” then was a first hike at the February Board meeting in 2023.

Developments since then have now prompted us to bring forward that tightening date to the meeting on August 2, 2022.

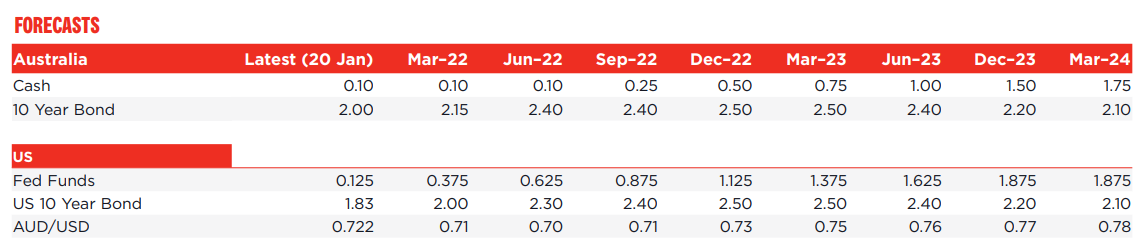

We now expect one hike of 15 basis points in August to be followed by a further hike of 25 basis points in October.

The full extent of the cycle and expected timing of subsequent moves is discussed below.

This revised timing for the first move is still well short of market pricing which is for the first hike to occur in June.

We understand that the Governor has firmly indicated that he does not expect to be raising rates until very late 2023 or 2024 and that this expectation is entirely consistent with the Bank’s current economic forecasts.

Those forecasts, which will be refreshed and possibly changed for the February 1 Board meeting, indicate that underlying inflation will print 2.25% by the end of 2022 and 2.5% by the end of 2023.

Wages growth is expected to reach 2.5% in 2022 lifting to 3% in 2023.

If these forecasts prove to be accurate then the “late 2023/2024” guidance will be appropriate.

But we have quite different forecasts for: inflation; wages growth and the unemployment rate.

We expect that underlying inflation (trimmed mean) will reach 2.4% in 2021 and lift to 2.6% in March 2022 and 2.9% in June 2022.

This will mean that by the time of the August meeting the Board will have observed three consecutive quarters in which annual underlying inflation has achieved or exceeded its target (around the mid-point of the 2-3% range).

Wages growth will be slower to reach the RBA’s “target” of 3% but whereas achieving the inflation target is a hard condition for any policy change, acceptance that wage growth has consistently lifted towards a speed we have not seen since 2014 should be sufficient to satisfy the Bank that the necessary conditions for a rate increase have been achieved.

We expect quarterly growth in the Wage Price Index to increase from 0.6% in the September quarter to 0.7% in the December quarter, to be followed by 0.8% in the March quarter.

The very low 0.4% result in the June quarter of 2021 means the actual Wage Price Index will still show annual growth of 2.75% for the year to March (the most recent dt available for the August meeting) but the increasing momentum will be clear once the six- month annualised pace reaches the 3% target.

If the Board sees the 3% wages growth as a hard target it may opt to delay the hike until the September Board meeting when the low 0.4% will drop out of the annual rate allowing it to reach the annual pace of 3%.

When assessing the outlook for wages, the Board will also rely on its own liaison work and high frequency measures of wage pressures. Even though the most recent reports from the Bank on its liaison points to a 2.5% pace for wages growth, we expect the picture to change quickly by the middle of 2022.

An example of the emerging evidence in the higher frequency data is the weekly payrolls report which shows a 9% lift in the total wage bill over the year to 19 December 2021 – with payrolls rising 3.2% over the same period this means average wage rose by 5.6%yr. This measure is impacted by bonuses paid, hours worked and changes in the composition of the work force, all of which are excluded from the Wage Price Index measure, but the sharp increase in this annual growth measure in recent months certainly bears consideration.

We accept that there is high inertia in the enterprise agreements (around 38% weighting in the Wage Price Index) and minimum wages/awards (around 21%) but expect that there will be a number of aspects of the WPI that will indicate stronger pressures than the headline print – the individual agreement component (around 37%) should be seeing gains running at around 0.9% a quarter and should be seen as a reliable lead indicator for enterprise agreements (note that the individual agreement component lifted by 1.1% in the September quarter partly boosted by seasonality and some ‘catch up’ from the very weak June quarter).

We expect that the National Wage case in April, a month before the likely date of the federal election, will also result in the government supporting a more generous settlement than has been the case in the recent past, potentially boosting award and the minimum wages by around 3%.

We are more optimistic about the unemployment rate than the Bank’s latest forecasts. Currently the Bank expects the unemployment rate to reach 4.25% by end 2022 and 4.5% by the month of June 2022 – our same forecasts are 3.8% and 4.1% respectively.

The Board would probably view around 4% as full employment – an objective the Bank does not expect to achieve until end 2023 but which we expect by June 2022.

The path of the tightening cycle Back in June last year we targeted a terminal RBA cash rate of 1.25%.

That related to the peak debt servicing ratio for the household sector we observed in previous cycles in 2009-10 and in 2018 (the latter stemming from macro-prudential measures rather than official rate tightening). But that forecast last June was in the context of a more benign inflation profile than we now expect. We now think the RBA will need to venture into mildly contractionary policy settings to address any inflation/wages risks.

While the concept of the household debt servicing ratio as a constraint to rates is attractive it is by no means an exact measure – the income distribution of those holding the debt; the exact mix between fixed and floating rate terms and between interest only and amortising loans complicates estimates.

There is also the likelihood that, over the long run, interest rates in Australia and the US are unlikely to settle too far out of alignment.

For these reasons we have lifted the terminal rate to 1.75% from the 1.25% we estimated back in June. The exact profile for rate rises would be 40 basis points in 2022; 100 basis points in 2023; with one final move of 25 basis points in early 2024.

The last example of an RBA tightening cycle was in 2009 /10 and saw six 25 basis point moves over the course of seven meetings between November 2009 and May 2010.

That was at a time when the RBA assessed neutral as being well above the 3% starting point and argued that it was important to move quickly away from the emergency settings associated with the GFC.

While the motive to move away from emergency settings will be the same, it is likely that there is more uncertainty around the exact level of neutral and the moves will be somewhat more cautious than we saw in 2009/10.

That said, central banks are also cautious about getting too far ‘behind the curve’ since that only increases the risks that policy will have to move further into contractionary territory than would be the case if policy had been tightened in a timely fashion.

For example, there is one view amongst some analysts that despite achieving its objectives, the RBA would remain on hold for an extended period, unnecessarily getting behind the curve and probably having to eventually move much more quickly risking an overshoot.

International issues

The FOMC has signalled that it is likely to begin tightening at its March meeting – ahead of our previous call that the tightening would begin in June – due to the rapid improvement in conditions in the labour market and a more sustained rise in inflation than had been assessed earlier in 2021.

The intention of the FOMC now appears to be to move more quickly to rein in an inflation rate that is now running a touch above 7%.

That would imply four rather than three hikes by the FOMC in 2022 – effectively adding the March move to our already expected three moves from June.

The key for global markets is whether inflation in the US can be brought back to the 2-2.5% range during 2023 to allow the FOMC to settle rates at around neutral rather than be obliged to push heavily into contractionary territory.

That remains our call and is consistent with a 1.875% terminal rate in this cycle (up from 1.625%) After four moves in 2022 the three additional 0.25% moves are likely to occur in 2023, providing the RBA with the comforting signal that the federal funds rate can settle around, or slightly above, the neutral level.

The risk for markets globally is that inflation does not settle back in 2023 into the 2-2.5% range forcing the FOMC to push into contractionary policy settings and precluding the FOMC from easing policy rates in the event of a major market meltdown.

The AUD and Bond rates

Our key near term AUD forecast is for a low point in the AUD of USD0.70 by mid-2022.

While we have a more urgent tightening cycle from the RBA we have also lifted the pace of rate hikes by the FOMC.

From the end 2022 we are expecting a further five RBA hikes through 2023 and 2024 compared to only three from the FOMC. That will support our call for a rising AUD through the second half of 2022 and 2023.

Note that relative to our earlier forecasts, the negative margin between the terminal cash rates for RBA and FOMC has narrowed from 40 basis points to 12.5 basis points, providing further support for our rising AUD view from mid- 2022.

We maintain our call that due to the sensitivity of the Australian economy to excessive levels of household debt the terminal rate can settle slightly below the FOMC rate.

All last year our forecasts for the long bond rates in both Australia and the US (key targets of 2.3% by end 2022) were heavily ‘out of the money’ as markets priced in a benign outlook for bond rates.

That has recently changed significantly with the AUD bond rate around 2%.( up from 1.5% in late 2021).

The higher terminal rates for RBA and FOMC now support slightly higher bond rate peaks, reaching 2.5% rather than the previous 2.3% by end 2022.

These relatively benign rates are consistent with our current expectations that inflation can settle around central banks’ targets allowing terminal rates to hold near neutral.

Omicron and economic growth

The omicron wave is denting economic activity in the opening quarter of 2022, centred largely on the consumer. The dramatic surge in cases locally looks to be driving a pull- back in consumer spending with widespread reports of disruptions to production and distribution networks as employees required to isolate are unable to work. We expect this to result in a hit to hours worked and a run-down of inventories, which is a drag on growth. A temporary soft spot in business confidence is also likely to see some delays to business investment, largely around equipment spending.

Westpac Economics is now forecasting growth for 2021 and 2022 of 3.2% and 5.5%, respectively. That is revised from the pre-omicron profile of 2.8% and 6.4%, with a net reduction of 0.5%.

It is worth noting that in the lead-up to the omicron outbreak, the economy was rebounding during the December quarter 2021 more quickly than previously anticipated. Retail sales were particularly strong in the month of November, surging 7.3% and building on a strong 4.9% gain in October. This has led to an upgrade to our Q4 GDP growth forecast, from 2.2% to 2.6%, led by a 1ppt upward revision to consumer spending.

More recent data from our Westpac Card Tracker, based on weekly credit and debit card activity to January 15, points to a material weakening in spending since late December.

Indeed, the tracker data suggests total consumer spending is likely to be down close to 3% for the January month. While some improvement on the COVID front is likely to see activity improve, particularly as we move into February, this is now expected to leave total consumer spending flat for the March quarter. This is compared to what would otherwise have been a continuation of the strong gains seen in the December quarter. The resilience of consumer sentiment in January is one promising sign that the consumer may revive quickly once the COVID situation stabilises.

With consumer spending stalled in the March quarter, and inventories subtracting an expected 0.3ppts in the period, overall GDP is also expected to be flat in the opening quarter of 2022. At this stage, we anticipate that disruptions to construction activity for the quarter will be minimal – with the sector largely on summer holiday early in January, and with some normalisation in movement and activity envisaged over the remainder of the quarter.

The quarterly GDP profile for 2022 is now expected to be: 0.0%; 2.6%; 2.0% and 0.8%.

For the 2022, consumer spending is expected to expand by 7.6%, lowered from 9.4% previously. This comes from both the upward revision to 2021 and the omicron disruptions in 2022.

Business investment gains have been pared back somewhat in 2022, but to a still strong pace, at a revised 7.8%, lowered from 8.5% pre omicron. This factors in equipment spending growth of 10.5%, trimmed from 12% previously. The hit to business confidence from omicron is likely to be short lived, as was the case with delta, with firms quickly refocusing on strong underlying demand and tight capacity, as well as generous tax concessions.

As noted above, inventories are run-down in the March quarter, due to labour shortages disrupting production and distribution. A stabilisation of inventories is anticipated in the June quarter, followed by some rebuilding of stock levels in the September quarter.

On the trade side, import growth for 2022 is pared back to reflect the downward revisions to demand, lowered by 1.3ppts to a still brisk 12.6%. Note that as much of the disruption to consumer spending is around domestic services, which limits the hit to imports. Export growth has also been trimmed, at the margin, by around 0.5% to 8.3%, to reflect those supply disruptions in the March quarter, with a partial catch-up over the following quarters.

The risks

One important risk to this rate and growth view is a further rise in COVID infections and hospitalisations near term or further out as the effectiveness of boosters and post-infection immunity wears off – the latter likely to be around mid-2022 when winter will be upon us and the virus tends to spread more freely (although evidence from the severe northern winters is not entirely relevant for Australia’s mild winters).

Importantly, the RBA along with other central banks, has come to look through COVID disruptions.

The line the RBA used around the delta lockdowns was that it would “delay but not derail” the recovery. That may mean that our timing for the first move turns out to be too early but the cycle would not be abandoned.

Further complicating this issue is that while another wave will impact activity as we are now seeing in January its implication for the nominal economy is less clear and we know that the RBA’s concern in recent cycles has been the weakness in the nominal economy.

Despite the sudden shift to lock downs last year, the RBA continued its tapering program, although it did delay consideration of a further taper by three months.

Increasing wage pressures and tightening labour markets are important preconditions for these forecasts. The opening of international borders will ease some of the labour shortages but is unlikely to be a smooth process.

Inflation and wage pressures result from an imbalance between demand and supply. The opening of borders will lift demand as well as increasing supply while the demand offset from Australians travelling abroad is likely to be minimal as Australian travellers remain cautious about overseas health risks, including the quality of overseas health systems.

Conclusion

Our forecast revisions reflect a much faster lift in inflation and wages growth than envisaged last June. While we have shaved our growth rate in 2022 due to the omicron-related contraction in consumer spending in January we do not see that as being significant for our wages/inflation/ employment profile.

The FOMC has now acknowledged that the conditions for a tightening of policy have arrived and, while less urgent, we think the RBA will do the same by August.

The approach we have used in this process is to recognize when our forecasts are different to the RBA; assume our forecasts will be correct; and predict how the central bank will react to a new reality.