By Gareth Aird, head of Australian economics at CBA:

Key Points

- We expect the RBA to announce the cessation of the bond buying program (QE) at the upcoming February Board meeting. The cash rate target will be left unchanged at 0.1%.

- The RBA Governor is likely to preview the RBA’s updated economic forecasts in his post-meeting Statement which will be more fully fleshed out in his speech on Wednesday 2 February to the National Press Club.

- The RBA will publish their full suite of updated economic forecasts in the February 2022 Statement on Monetary Policy (SMP) on Friday.

- We expect the RBA to significantly upwardly revise their profile for underlying inflation and more modestly downwardly revise their profile for the unemployment rate (this should also result in a small upward revision to their forecast profile for wages).

- The RBA’s newly painted central scenario for the economy is likely to be consistent with a first hike in the cash rate in mid 2023.

- But as has been the case over the past year, we expect the RBA’s updated inflation and wages forecasts to remain conservative relative to our forecasts, which are consistent with a rate hike in August 2022 (the risk lies with an earlier hike in June or July).

Overview

Market participants will have a lot to digest over the coming week. The RBA ends a six week communication hiatus in abrupt fashion with three major events. The old adage when it rains it pours springs to mind!

The Board holds the first meeting of 2022 on Tuesday 1 February. Governor Lowe will deliver a speech the following day to the National Press Club (this has now become an annual event on the RBA calendar). And the week ends with the RBA’s February 2022 Statement on Monetary Policy (SMP) that will contain updated economic forecasts.

The Governor’s speech, which will be followed by an extended Q&A session, is likely to be the standout of the three RBA events.

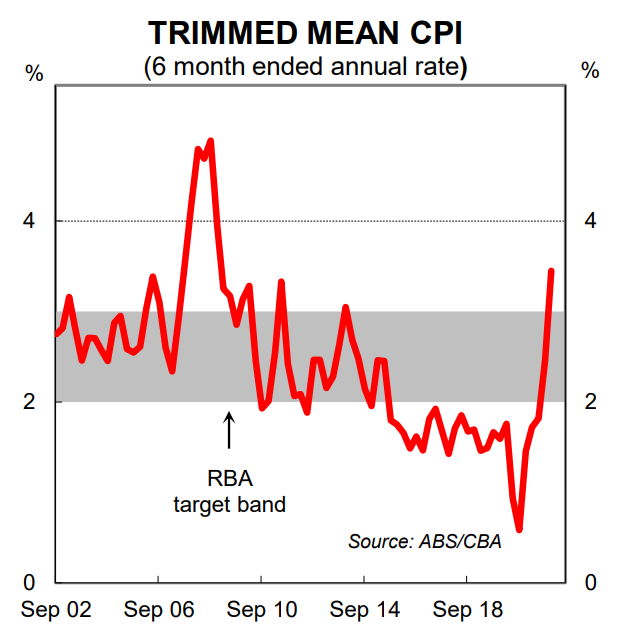

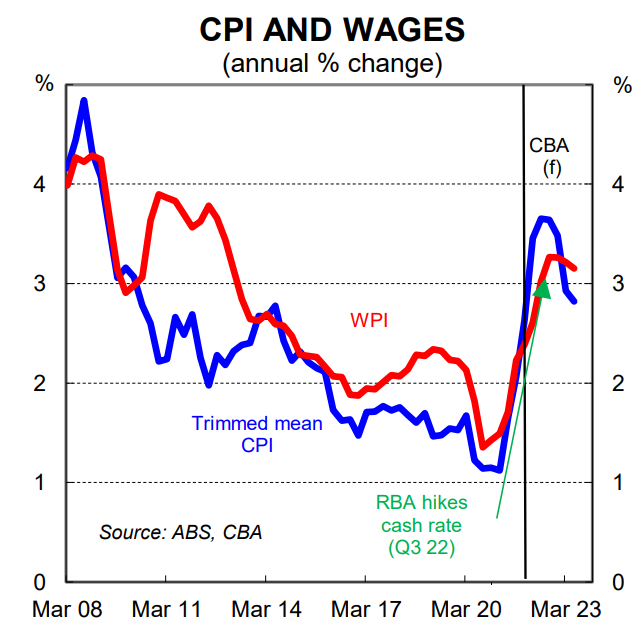

RBA inflation forecasts have missed the mark

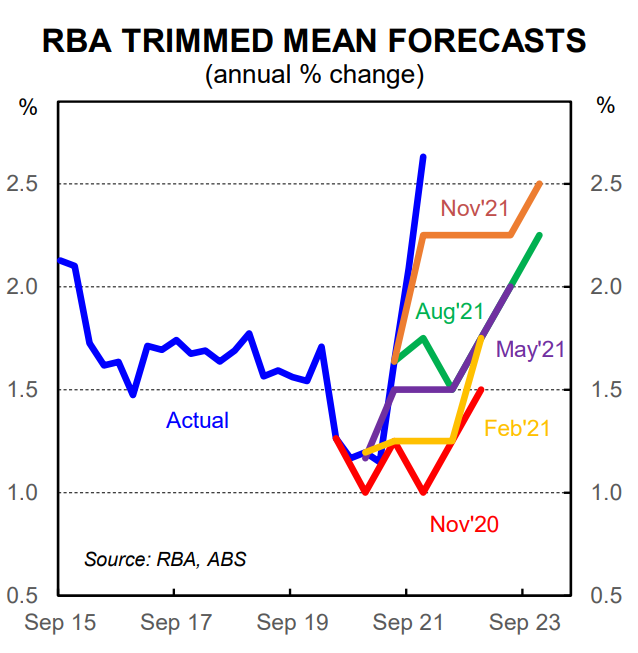

It is fair to say that the RBA forecasts for underlying inflation have missed the mark by a significant margin over the past year (see below chart). By extension, this means that their central scenario for the inflation outlook is not playing out as they expected.

Of course no economist has a crystal ball. And forecasting through a pandemic has been an incredibly tough assignment for anyone tasked with trying to predict the future. But the RBA have been quite dogmatic in their message that inflation pressures would only emerge modestly and “gradually”. Indeed they went out of their way to argue why the inflation dynamics would be different in Australia compared to many other comparable countries where inflation has risen significantly.

Regular readers will know that over the past year we assessed the inflation outlook through a different lens to the RBA. More specifically, we put less weight than usual on our models that forecast inflation based on spare capacity in the economy. Instead we put more weight on how the massive fiscal stimulus financed by money creation would generate demand pull inflation. This meant we expected to see inflation rise before wages growth. So far our thesis has playing out.

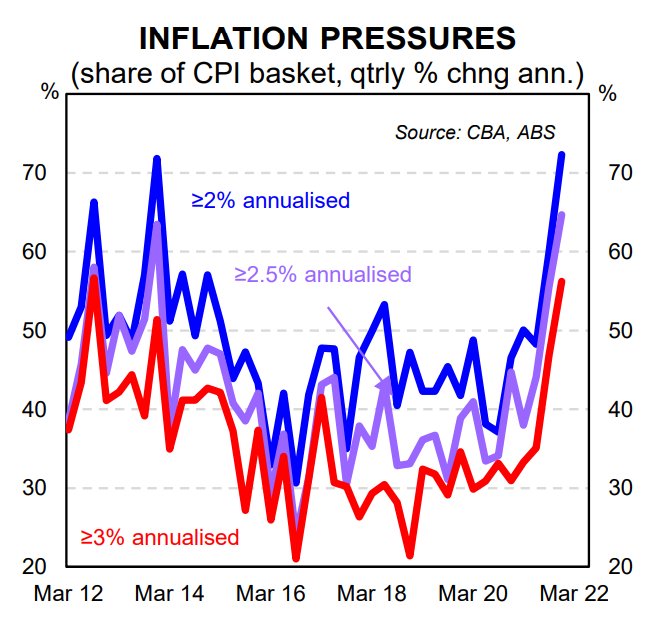

The latest data on consumer prices in Australia indicates that inflationary pressures have emerged quickly and sharply over the past six months (very much in contrast to the RBA’s “gradually” narrative).

The big inflation print this week did not surprise us (recall the Q4 21 trimmed mean rose by 1.0%/qtr; our forecast was 0.9%/qtr; the consensus amongst the forecasters was 0.7%/qtr; and the RBA’s forecast was ~0.6%/qtr).

Business surveys indicate the inflationary pulse is continuing to gather steam, so further strong reports are forthcoming. However, the drivers of firm inflation are likely to shift. More specifically, the impact of fiscal stimulus and money printing on inflation will wane. But that will be replaced by inflation that is driven by a very tight labour market and higher wages growth – exactly the type of inflation the RBA wants to engineer.

What does the RBA forecast and say next week?

Our working assumption is that the RBA will recognise that the inflation outlook has changed. This means we expect them to make a solid upward revision to their forecast for underlying inflation in 2022. We think they will forecast underlying inflation to be around 3.0%/yr over 2022 (i.e. the top of their target band).

Optically that appears high. But it’s a relatively conservative forecast given the six month annualised pace of core inflation is 3.5% and some low numbers will drop out of the annual calculation over the next two prints (the Q1 21 trimmed mean rose by 0.4% and the Q2 21 trimmed mean increased by 0.5%). Quarterly growth rates from here of 0.7% will see core inflation print around 3.0%/yr in 2022. We think that any forecast below 3.0%/yr for underlying inflation in 2022 isn’t particularly credible. For point of comparison, we expect core inflation to be above 3.5%/yr by mid-22).

That all said, we anticipate that the RBA will make only a very modest upward adjustment to their forecast profile for wages growth. This will simply reflect a lower starting point for the unemployment rate which printed at 4.2% in December. We think the most likely outcome is that the RBA upwardly revise their wages forecast from 2.5%/yr at end-2022 to 2.75%/yr and from 2.75%/yr mid-2023 to 3.0%/yr).

Forecasts of this configuration will mean the RBA can continue to emphasise their current reaction function to the market. This also means they can broadly keep their message unchanged from last year around what it will take for them to raise the cash rate despite making a solid upgrade to their forecast profile for underlying inflation.

More specifically, they can simply reiterate what they said at the end of last year: “the Board will not increase the cash rate until actual inflation is sustainably within the 2-3% range. This will require the labour market to be tight enough to generate wages growth that is materially higher than it is currently. This is likely to take some time and the Board is prepared to be patient.”

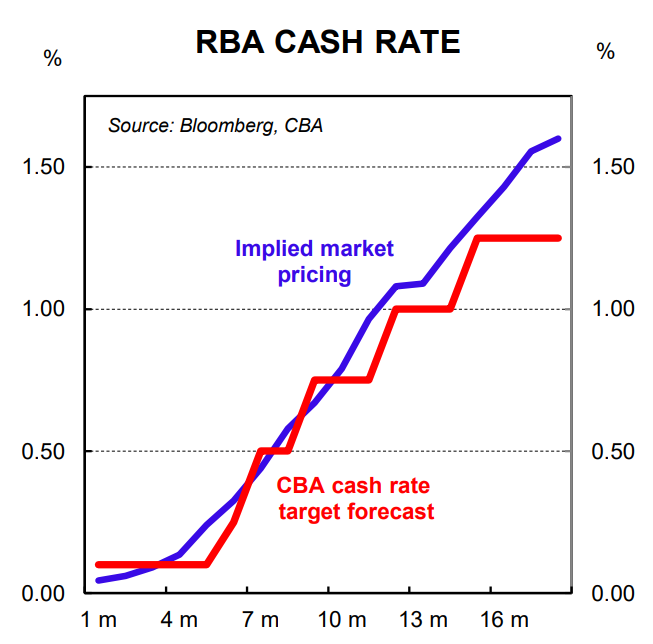

If the RBA takes this approach then the Governor will likely signal next week in his speech that the most probable outcome based on their new forecasts is a rate rise in mid-2023 with the slim chance of a rise in 2022. This is not a ‘policy pivot’.

The CBA view

We think that ultimately the RBA’s new updated forecasts will still miss the mark and we expect two strong wages prints coupled with core inflation above 3.5% by mid-2022 to be the catalyst for a first hike in the cash rate in August 2022. Put simply, the RBA’s objectives will be achieved by then and the appropriate policy response will be to commence normalising the cash rate.

On the bond buying program, we expect the RBA to announce the cessation of purchases at the Board meeting next week, as per our call in late December.