The RBA released its monthly chart pack this morning with some end of year figures and as always its a fun flirtatious flick-through!

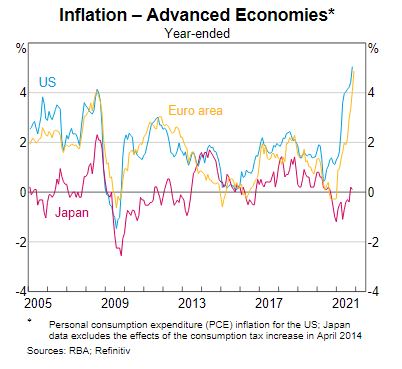

Let’s look at inflation first, which is either transitory or out of control depending on your point of view, but that’s a steep curve higher for Yankee-land and Euro-Disney:

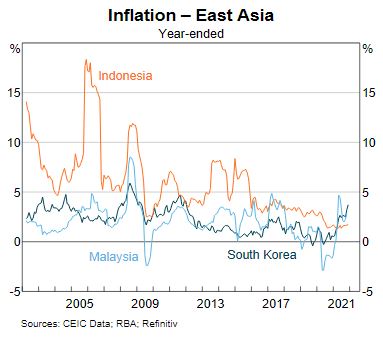

The US and Europe are seeing big moves higher in inflationary pressures while the East Asian countries are also seeing a pickup in inflation as supply constraints push prices ever higher.

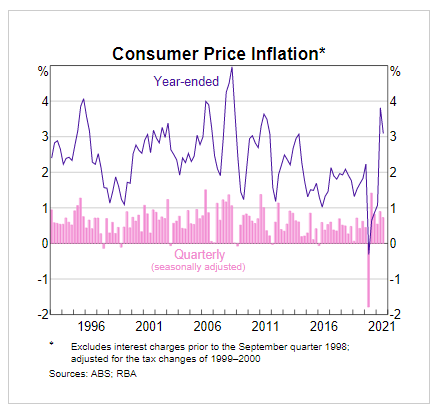

Meanwhile the local (very flawed and very laggy) measure of inflation remains somewhat benign despite the COVID spike, with the RBA still sitting on its hands. This seems to be changing as the latest PMI survey showed as supply constraints and input costs rise:

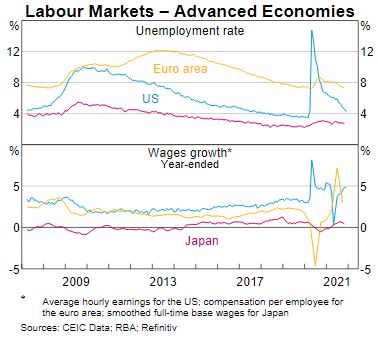

Unemployment rates are dropping, the Great Resignation is having a big impact in the US, although European wages growth is starting to stall:

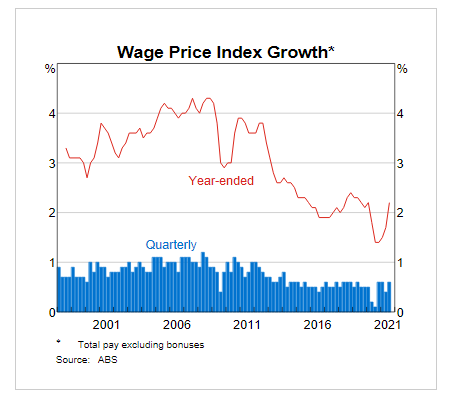

Australian workers continue to miss out on any meaningful wage growth:

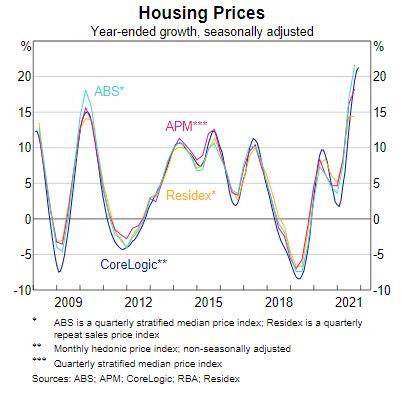

On to houses where its still going gangbusters – more than 20% annualised growth – which has to come down sooner or later? Surely?

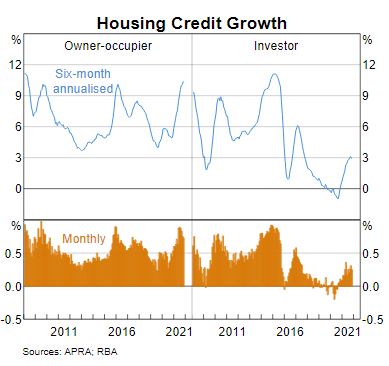

All being led by owner/speculators, not the investor/speculator crowd, although the latter has seen a tick up in credit growth:

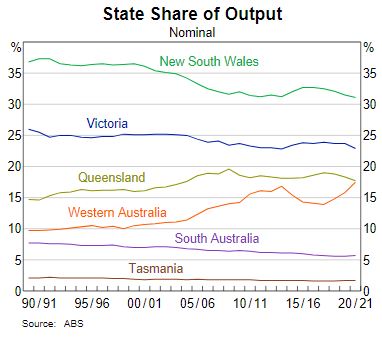

Different chart for a change, the state share of output showing WA taking up the reins as the COVID states grind to a halt:

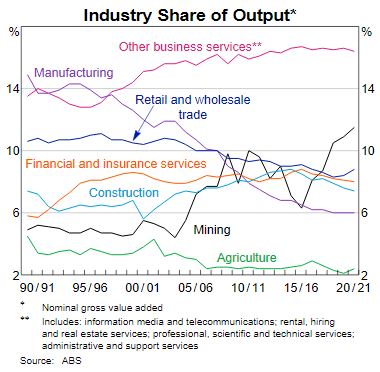

And of course its all mining as the manufacturing sector stagnates:

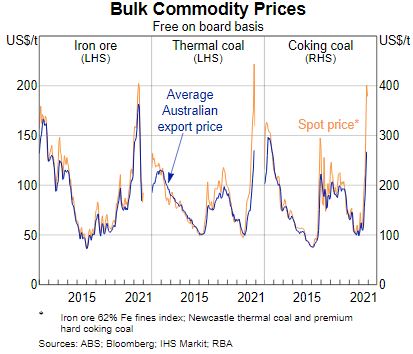

Helped along by very high bulk commodity prices, particularly coal:

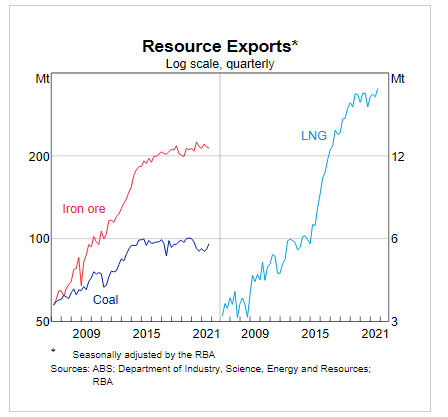

Even though volumes haven’t increased for coal (and will eventually go down to zero in the years ahead), LNG continues to soar out of control in ridiculous fashion, when it should all be sequestered locally to keep energy prices low domestically:

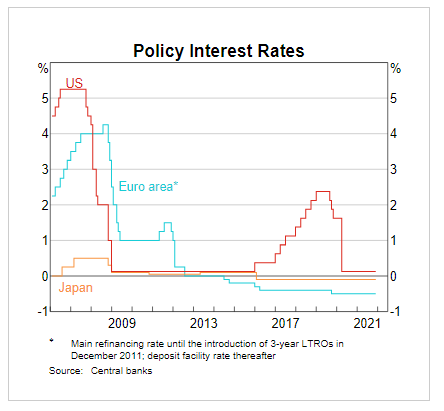

Moving to interest rates, its steady as she goes for the major economies, with only the UK (not shown, since it ain’t part of the Euro area no more) lifting recently:

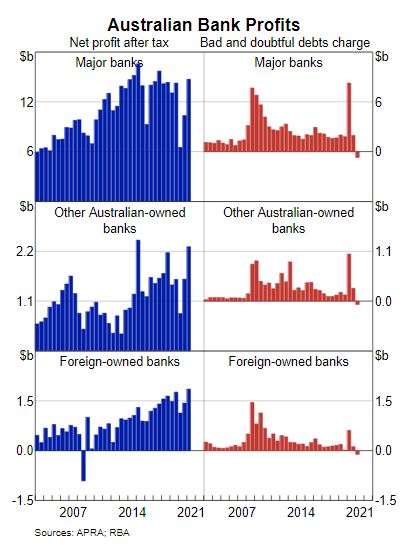

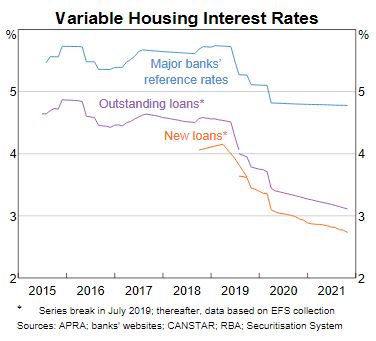

With local interest rates set by the banks still hovering around the 3% level despite the RBA sitting at near zero – nice padding!

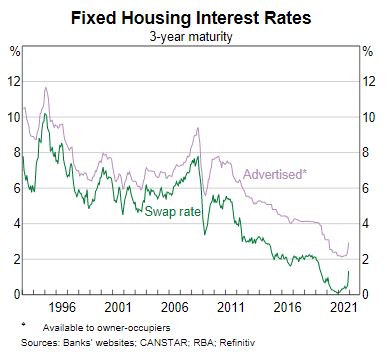

Meanwhile, the fix is in as the banks realise that shorter term interest rates will rise soon as fixed housing loans head sharply higher:

Must protect those profits hey!